Finance Commission – Issues related to devolution of resources

Should State Governments borrow more? | Explained

From UPSC perspective, the following things are important :

Prelims level: Finance Commission; State Government; FRBM Act;

Mains level: Fiscal Federalism and its challenges

Why in the News?

Recently, the SC rejected Kerala’s plea for immediate relief in its case urging the Union government to ease borrowing constraints, allowing the state to secure extra funds in the ongoing fiscal year.

State governments receive funds from three sources:

- Own revenues (tax and non-tax)

- Transfers from the Union government as shares of taxes and as grants

- Market borrowings

Fiscal Demands for Extra Funds:

- Increased Expenditure: In 2020-21, the Kerala government sharply increased its spending to 18% of its GSDP, to provide economic relief in the wake of the COVID-19 pandemic, aided by the relaxation in borrowing norms then

- Central Gov transfers to Kerala declined: As ratios of GSDP, the Union government’s transfers to Kerala declined to 2.8% in 2023-24, significantly lower than previous years, even as the State’s revenues remained at around 8.0%.

- This meant that, in 2023-24, the State government could meet its modest budget expenditure, equivalent to 14.2% of GSDP, only by raising the borrowing to 3.4% of the GSDP

Socio-Economic for Extra Funds:

- Aging Population: Kerala, like many other states, faces the challenge of an aging population, which puts pressure on pension funds and healthcare systems, necessitating long-term financial planning and investment.

- Pension Liabilities: The substantial outgo for pensions poses a financial burden on the state’s budget, requiring strategies for sustainable pension management to ensure fiscal stability.

- Youth Outmigration: Kerala experiences significant outmigration of its youth, leading to a loss of productive workforce and potential tax revenues, highlighting the need for policies to retain skilled workers and stimulate economic growth

About Net Borrowing Ceiling (NBC):

|

Basis of the Net Borrowing Ceiling:

- Fiscal Responsibility Legislation: Both the central and state governments in India adhere to the FRBM Act, which establishes fiscal deficit goals to uphold fiscal discipline. Under the FRBM, states are required to maintain a fiscal deficit limit of 3% of the Gross State Domestic Product (GSDP).

- Central Government Guidelines: The central government, through the Department of Expenditure in the Ministry of Finance, sets the annual borrowing limits for each state based on a formula that considers the state’s GSDP, existing debt levels, fiscal discipline, and other relevant factors. These limits can be revised in response to special circumstances, such as natural disasters or significant economic downturns.

- Finance Commission Recommendations: The Finance Commission, which is constituted every five years, recommends how the central taxes are to be divided between the centre and the states and suggests measures to maintain fiscal stability. It also provides recommendations regarding the borrowing limits of states.

Conclusion: States need to put in place an effective forecasting and monitoring mechanism for cash inflows and outflows so that a need-based approach is followed for market borrowings and the interest cost of cash surpluses is minimized.

Mains PYQ

Q What were the reasons for the introduction of Fiscal Responsibility and Budget Management (FRBM) Act, 2013? Discuss critically its salient features and their effectiveness. (UPSC IAS/2013)

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Explained: Financial Devolution among States

From UPSC perspective, the following things are important :

Prelims level: Article 270, Article 280 (3)

Mains level: Not Much

Introduction

- Several Opposition-ruled states, particularly from southern India, have voiced concerns over the present scheme of financial devolution, citing disparities in the allocation of tax revenue compared to their contributions.

- Understanding the concept of the divisible pool of taxes and the role of the Finance Commission (FC) is crucial in addressing these issues.

Divisible Pool of Taxes: Overview

- Constitutional Provision: Article 270 of the Constitution outlines the distribution of net tax proceeds between the Centre and the States.

- Share of taxes: Taxes shared include corporation tax, personal income tax, Central GST, and the Centre’s share of Integrated Goods and Services Tax (IGST), among others.

- Finance Commission’s Role: Article 280(3) (a) mandates FC, constituted every five years, recommends the division of taxes and grants-in-aid to States based on specific criteria.

- XVI FC: It consists of a chairman and members appointed by the President, with the 16th Finance Commission recently constituted under the chairmanship of Arvind Panagariya for the period 2026-31.

Basis for Allocation: Horizontal and Vertical Devolution

- Vertical Devolution: States receive a share of 41% from the divisible pool, as per the 15th FC’s recommendation.

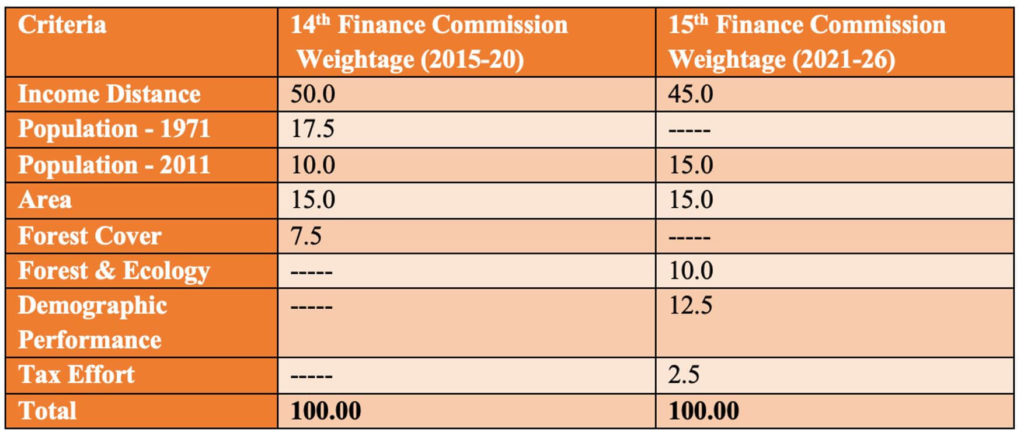

- Key criteria for horizontal devolution: For horizontal devolution, FC suggested 12.5% weightage to demographic performance, 45% to income, 15% each to population and area, 10% to forest and ecology and 2.5% to tax and fiscal efforts.

- Income Distance: Reflects a state’s income relative to the state with the highest per capita income (Haryana), aiming to maintain equity among states.

- Population: Based on the 2011 Census, replacing the earlier 1971 Census for determining weightage.

- Forest and Ecology: Considers each state’s share of dense forest in the total forest cover.

- Demographic Performance: Rewards states for efforts in controlling population growth.

- Tax Effort: Rewards states with higher tax collection efficiency.

Challenges and Issues

- Exclusion of Cess and Surcharge: Around 23% of the Centre’s gross tax receipts come from cess and surcharge, which are not part of the divisible pool, leading to disparities in revenue sharing.

- Variation in State Contributions: Some states receive less than a rupee for every rupee they contribute to Central taxes, indicating disparities in revenue distribution.

- Reduced Share for Southern States: Southern states have witnessed a decline in their share of the divisible pool over successive FCs, affecting their fiscal autonomy.

Proposed Reforms

- Expansion of Divisible Pool: Including a portion of cess and surcharge in the divisible pool could enhance revenue sharing among states.

- Enhanced Weightage for Efficiency: Increasing the weightage for efficiency criteria in horizontal devolution, such as GST contribution, can promote equitable distribution.

- Greater State Participation in FC: Establishing a formal mechanism for state participation in the FC’s constitution and functioning, akin to the GST council, can ensure a more inclusive decision-making process.

Conclusion

- Addressing issues of financial devolution requires a collaborative approach between the Centre and the States, focusing on equitable distribution and fiscal federalism.

- Reforms in revenue-sharing mechanisms, along with enhanced state participation in decision-making bodies like the FC, are essential for promoting balanced development and resource allocation across the country.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Call for imposing Financial Emergency in Kerala

From UPSC perspective, the following things are important :

Prelims level: Financial Emergency under Article 360

Mains level: Not Much

In the news

- The Supreme Court proceeded with hearing a suit filed by the State of Kerala against the Centre for alleged arbitrary interference in its financial matters, following unsuccessful negotiations between the two parties.

- Earlier, Kerala Governor sought for the Presidential imposition of a financial emergency in the State under Article 360(1) of the Constitution due to dwindling situation of finances in the State.

What is Financial Emergency?

- Enshrined in Article 360: It is a vital provision aimed at addressing severe financial crises threatening India’s economic stability.

- Declaration and Authority: It can be declared by the President upon satisfaction that the financial stability or credit of India or any part of its territory is under threat.

- CoM Advice: The declaration is made based on the advice of the Council of Ministers, reflecting the collective responsibility of the executive branch.

Legislative Approval

- While the President can proclaim a Financial Emergency, its extension beyond two months needs approval from both Houses of Parliament.

- Once approved, it remains in effect until revoked by the President, allowing for flexible management of financial crises.

Effects and Implications

- The Centre’s executive authority expands significantly during a Financial Emergency, enabling it to issue directives to states on financial matters.

- Centralization of fiscal policies occurs, with the President empowered to reserve money bills passed by state legislatures for consideration.

- Austerity measures, including salary and allowance reductions for public officials, can be implemented to address economic challenges.

Judicial Review and Criticism

- 38th Amendment Act (1975) made the President’s decision final and immune from judicial review.

- However, the 44th Amendment Act (1978) allowed for judicial scrutiny.

- This amendment ensured checks and balances within the constitutional framework, preventing unchecked executive authority.

Historical Context and Usage

- Financial Emergencies have been sparingly invoked in India’s history, despite facing significant financial crises such as in 1991.

- The cautious utilization of this provision underscores the importance of aligning its implementation with democratic principles and federalism.

Conclusion

- The Supreme Court’s intervention in the Kerala-Centre financial dispute underscores the importance of cooperative federalism in addressing intergovernmental conflicts.

- The forthcoming hearings aim to reconcile differences and ensure the equitable distribution of resources, fostering harmonious relations between the Centre and states.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

The severe erosion of fiscal federalism

From UPSC perspective, the following things are important :

Prelims level: Fiscal deficit

Mains level: Net Borrowing Ceiling (NBC)

Central Idea:

The article discusses Kerala’s protest against the imposition of a Net Borrowing Ceiling (NBC) by the Central Government, which restricts the state’s ability to borrow funds. It argues that this imposition undermines fiscal federalism and challenges the constitutional authority of the state legislature over financial matters.

Key Highlights:

- Kerala Chief Minister Pinarayi Vijayan leads a protest against the Central Government’s imposition of a financial embargo on Kerala.

- The NBC limits states’ borrowings, including those from state-owned enterprises like the Kerala Infrastructure Investment Fund Board (KIIFB), leading to a severe financial crisis in Kerala.

- The article questions the constitutionality of including state-owned enterprises’ debt in the state’s total debt, arguing that it encroaches on the state legislature’s authority over financial matters.

- Kerala’s Fiscal Responsibility Act, 2003, aims to reduce fiscal deficit, demonstrating the state’s commitment to fiscal discipline.

- The article criticizes the move towards “annihilative federalism,” where the central government’s actions detrimentally affect states’ ability to meet welfare obligations.

Key Challenges:

- Balancing fiscal discipline with the need for states to fund development projects and welfare schemes.

- Addressing the erosion of fiscal federalism and the encroachment of central authority over state finances.

- Resolving the conflict between the powers of the central government and state legislatures regarding financial matters.

- Mitigating the impact of borrowing restrictions on states’ ability to fulfill their financial obligations.

Key Terms:

- Net Borrowing Ceiling (NBC): Limit imposed on states’ borrowings from all sources.

- Kerala Infrastructure Investment Fund Board (KIIFB): State-owned body responsible for funding infrastructure projects.

- Fiscal Responsibility Act: Legislation aimed at reducing fiscal deficit and promoting financial discipline.

- Fiscal Federalism: Distribution of financial powers and responsibilities between the central government and states.

- Annihilative Federalism: Central government actions that undermine states’ financial autonomy and welfare obligations.

Key Quotes:

- “The wide array of constitutional issues…point at the severe erosion of fiscal federalism in the country.”

- “The borrowing restrictions are an example of ‘annihilative federalism’ at play.”

Key Examples and References:

- Kerala’s protest led by Chief Minister Pinarayi Vijayan against the financial embargo imposed by the Central Government.

- The inclusion of KIIFB’s debt in Kerala’s total debt, leading to funding constraints for welfare schemes.

- Comparison of Kerala’s fiscal deficit reduction efforts with the central government’s fiscal deficit estimates.

Key Facts and Data:

- Kerala’s fiscal deficit reported to have reduced to 2.44% of the GSDP.

- Central government’s fiscal deficit estimated to be 5.8% for 2023-2024.

Critical Analysis:

The article underscores the tension between central authority and state autonomy in financial matters, highlighting the constitutional ambiguity surrounding the imposition of borrowing restrictions. It argues for a balanced approach that acknowledges states’ fiscal responsibilities while ensuring fiscal discipline.

Way Forward:

- Reevaluate the imposition of borrowing restrictions to ensure they do not unduly impede states’ ability to meet financial obligations.

- Enhance dialogue and cooperation between the central government and states to address fiscal challenges while respecting constitutional principles.

- Clarify the division of financial powers between the central government and state legislatures to mitigate conflicts and promote fiscal federalism.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Arvind Panagariya appointed as Sixteenth Finance Commission chief

From UPSC perspective, the following things are important :

Prelims level: Finance Commission

Mains level: Read the attached story

Central Idea

- The Centre has appointed Arvind Panagariya, a renowned trade economist and former Niti Aayog vice chairman, as the chairman of the Sixteenth Finance Commission.

Who is Arvind Panagariya?

- Panagariya is a professor at Columbia University.

- He served as the first vice chairman of the Niti Aayog from 2015 to 2017, succeeding the Planning Commission.

About Finance Commission

- Establishment: The Finance Commission (FC) of India was established by the President in 1951 under Article 280 of the Indian Constitution.

- Purpose: Its primary role is to define and regulate the financial relations between the central government and the individual state governments.

- Legislative Framework: The Finance Commission (Miscellaneous Provisions) Act, 1951, further outlines the qualifications, appointment, disqualification, term, eligibility, and powers of the Finance Commission.

- Composition: Appointed every five years, the FC comprises a chairman and four other members.

- Evolution: Since the First FC, changes in India’s macroeconomic landscape have significantly influenced the Commission’s recommendations.

Constitutional Provisions

- Article 268: Facilitates the levy of duties by the Centre, with collection and retention by the States.

- Article 280: Outlines the FC’s composition, qualifications for members, and its terms of reference. It mandates the FC to recommend the distribution of net tax proceeds between the Union and States and the allocation among States. It also addresses the financial relations between the Union and States and the devolution of unplanned revenue resources.

Key Functions of the Finance Commission

- Tax Devolution: Recommends how net tax proceeds should be distributed between the Center and States.

- Grants-in-Aid: Determines the principles governing these grants to States.

- Augmenting State Funds: Advises on measures to enhance the States’ Consolidated Funds to support local bodies and panchayats, based on State Finance Commissions’ recommendations.

- Other Financial Functions: Addresses any other financial matters referred by the President.

Members of the Finance Commission

- Structure and Standards: The Finance Commission (Miscellaneous Provisions) Act, 1951, provides a structured format and global standards for the FC.

- Qualifications and Powers: Specifies rules for members’ qualifications, disqualification, appointment, term, eligibility, and powers.

- Composition: The Chairman is chosen for their experience in public affairs. The other members are selected based on their judicial experience, knowledge of government finances, administrative and financial expertise, or special economic knowledge.

Challenges for the 16th Finance Commission

- Overlap with GST Council: The coexistence with the GST Council, a permanent constitutional body, presents a new challenge.

- Conflict of Interest: Decisions by the GST Council on tax rates could impact the FC’s revenue-sharing calculations.

- Feasibility of Recommendations: While the Centre often adopts the FC’s suggestions on tax devolution and fiscal targets, other recommendations may be overlooked.

Major Outstanding Recommendations

- Fiscal Council Creation: The 15th FC proposed a Fiscal Council for collective macro-fiscal management, but the government has shown reluctance.

- Non-Lapsable Fund for Internal Security: Though the Centre agreed ‘in principle’ to establish this fund, its implementation details are pending.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Cabinet clears terms of reference for 16th Finance Commission

From UPSC perspective, the following things are important :

Prelims level: Finance Commission

Mains level: Read the attached story

Central Idea

- The Union Cabinet approved the terms of reference (ToR) for the Sixteenth Finance Commission.

- The Commission will devise a formula for revenue sharing between the Centre and the States for the period starting April 1, 2026.

About Finance Commission

- Establishment: The Finance Commission (FC) of India was established by the President in 1951 under Article 280 of the Indian Constitution.

- Purpose: Its primary role is to define and regulate the financial relations between the central government and the individual state governments.

- Legislative Framework: The Finance Commission (Miscellaneous Provisions) Act, 1951, further outlines the qualifications, appointment, disqualification, term, eligibility, and powers of the Finance Commission.

- Composition: Appointed every five years, the FC comprises a chairman and four other members.

- Evolution: Since the First FC, changes in India’s macroeconomic landscape have significantly influenced the Commission’s recommendations.

Constitutional Provisions

- Article 268: Facilitates the levy of duties by the Centre, with collection and retention by the States.

- Article 280: Outlines the FC’s composition, qualifications for members, and its terms of reference. It mandates the FC to recommend the distribution of net tax proceeds between the Union and States and the allocation among States. It also addresses the financial relations between the Union and States and the devolution of unplanned revenue resources.

Key Functions of the Finance Commission

- Tax Devolution: Recommends how net tax proceeds should be distributed between the Center and States.

- Grants-in-Aid: Determines the principles governing these grants to States.

- Augmenting State Funds: Advises on measures to enhance the States’ Consolidated Funds to support local bodies and panchayats, based on State Finance Commissions’ recommendations.

- Other Financial Functions: Addresses any other financial matters referred by the President.

Members of the Finance Commission

- Structure and Standards: The Finance Commission (Miscellaneous Provisions) Act, 1951, provides a structured format and global standards for the FC.

- Qualifications and Powers: Specifies rules for members’ qualifications, disqualification, appointment, term, eligibility, and powers.

- Composition: The Chairman is chosen for their experience in public affairs. The other members are selected based on their judicial experience, knowledge of government finances, administrative and financial expertise, or special economic knowledge.

Challenges for the 16th Finance Commission

- Overlap with GST Council: The coexistence with the GST Council, a permanent constitutional body, presents a new challenge.

- Conflict of Interest: Decisions by the GST Council on tax rates could impact the FC’s revenue-sharing calculations.

- Feasibility of Recommendations: While the Centre often adopts the FC’s suggestions on tax devolution and fiscal targets, other recommendations may be overlooked.

Major Outstanding Recommendations

- Fiscal Council Creation: The 15th FC proposed a Fiscal Council for collective macro-fiscal management, but the government has shown reluctance.

- Non-Lapsable Fund for Internal Security: Though the Centre agreed ‘in principle’ to establish this fund, its implementation details are pending.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Why is Bihar demanding the Special Category Status?

From UPSC perspective, the following things are important :

Prelims level: Special Category Status

Mains level: Read the attached story

Central Idea

- Recently, Bihar govt passed a resolution seeking Special Category Status (SCS) for the state.

- This demand comes in light of the revelations from the “Bihar Caste-based Survey, 2022,” which unveiled that nearly one-third of Bihar’s population continues to grapple with poverty.

Special Category Status (SCS): An Overview

- Definition: SCS is a classification conferred by the Central government to support the development of states facing geographical or socio-economic disadvantages.

- Origins: SCS was instituted in 1969, based on the recommendations of the 5th Finance Commission (FC).

- Criteria: Five criteria are assessed before granting SCS, including factors like hilly terrain, low population density, and economic backwardness.

- Historical Allocation: Initially, three states—Jammu & Kashmir, Assam, and Nagaland—were granted SCS. Subsequently, eight more states, including Himachal Pradesh and Uttarakhand, received this status.

Benefits of having SCS

- Financial Assistance: SCS states used to receive grants based on the Gadgil-Mukherjee formula, accounting for approximately 30% of total central assistance.

- Devolution of Funds: Post the abolition of the Planning Commission and the recommendations of the 14th and 15th FCs, SCS assistance has been subsumed into increased devolution of funds for all states (now 41% in the 15th FC).

- Funding Ratio: SCS states enjoy a favourable 90:10 Centre-State funding split for centrally sponsored schemes, compared to 60:40 or 80:20 for general category states.

- Additional Incentives: SCS states receive concessions in customs and excise duties, income tax rates, and corporate tax rates to attract investments.

Why Bihar’s Demand for SCS?

- Resource Challenges: Bihar attributes its poverty and underdevelopment to limited natural resources, irregular water supply for irrigation, recurring floods in the north, and severe droughts in the south.

- Industrial Shift: The state’s bifurcation led to the relocation of industries to Jharkhand, creating unemployment and investment voids.

- Per-Capita GDP: Bihar’s per-capita GDP, at around ₹54,000, consistently ranks among the lowest in India.

- Welfare Funding: Chief Minister Nitish Kumar asserts that Bihar houses approximately 94 lakh poor families and that SCS recognition would generate about ₹2.5 lakh crore, crucial for funding welfare initiatives over the next five years.

SCS Demands from Other States

- Andhra Pradesh: Since its bifurcation in 2014, Andhra Pradesh has sought SCS due to revenue loss post-Hyderabad’s transfer to Telangana.

- Odisha: Odisha’s appeal for SCS underscores its vulnerability to natural disasters, such as cyclones, and a significant tribal population (around 22%).

- Central Government’s Response: Despite these demands, the Central government, citing the 14th Finance Commission’s report, which recommended against granting SCS to any state, has consistently rejected them.

Is Bihar’s Demand Justified?

- Criteria Fulfillment: Bihar meets most SCS criteria but lacks hilly terrain and geographically difficult areas, crucial for infrastructural development.

- Alternative Solutions: In 2013, the Raghuram Rajan Committee proposed a ‘multi-dimensional index’ methodology instead of SCS, which could be revisited to address Bihar’s socio-economic challenges effectively.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

What the 16th Finance Commission needs to do differently

From UPSC perspective, the following things are important :

Prelims level: 16th Finance Commission

Mains level: 16th Finance Commission and India's fiscal federalism

What’s the news?

- India’s fiscal landscape, transformed by GST, calls for a comprehensive reevaluation of fiscal federalism to address tax-sharing challenges and regional disparities.

Central idea

- The 122nd Constitutional Amendment of 2016 and the subsequent introduction of the GST regime in 2017 reshaped India’s fiscal landscape, replacing production-based taxation with a consumption-oriented approach. This shift highlights the importance of reevaluating fiscal federalism as the 16th Finance Commission forms, addressing tax-sharing principles and regional balance in taxation.

What is meant by fiscal federalism?

- Fiscal federalism refers to the division of financial responsibilities and resources between different levels of government within a federal or decentralized system.

- It encompasses the principles and mechanisms by which revenues are generated, collected, shared, and spent by various levels of government, typically at the national (central) and subnational (state or regional) levels.

- India operates as a federal republic with a multi-tiered system of governance, and fiscal federalism is an essential aspect of this arrangement.

Potential challenges faced by the 16th Finance Commission

- Revisiting Tax-sharing Principles: The 16th Finance Commission faces the challenge of reexamining and redesigning tax-sharing principles due to the shift from production-based to consumption-based taxation under the GST regime.

- Efficient Tax Collection: Variations in the cost of tax collection (ranging from 7 to 10 percent) have emerged as a challenge, given the joint collection of taxes by the Union and states under GST.

- Redesigning Horizontal Distribution: The Commission must address the challenge of redesigning criteria for distributing the divisible pool among states to ensure equitable distribution of tax revenues and grants.

- Reviewing the Compensation Scheme: The necessity, viability, and desirability of the GST compensation scheme must be reviewed by the Commission, considering the performance of GST revenues over the past six years.

- Institutional Relationships: Establishing formalized institutional relationships between the GST Council and the Finance Commission presents a challenge in the evolving federal financial structure.

The need for a comprehensive reevaluation of India’s fiscal federalism

- Shift to the GST Regime: The introduction of the Goods and Services Tax (GST) regime represents a monumental shift in India’s taxation system. This change from a production-based tax system to a consumption-based one necessitates a reevaluation of fiscal federalism to align with this new tax paradigm.

- Impact on Vertical and Horizontal Imbalances: The transition from a production-based to a consumption-based tax system has the potential to rectify historical vertical imbalances in tax revenue distribution. However, it also introduces new horizontal imbalances among states due to varying consumption patterns and economic development levels.

- Equitable Resource Allocation: To ensure a fair distribution of resources among states, it is imperative to revisit the criteria for resource allocation. The reevaluation should consider the principles of fiscal federalism and the specific needs of each state within the GST framework.

- Efficiency and Transparency: An updated fiscal federalism framework can lead to increased efficiency and transparency in revenue collection, sharing, and utilization. This can help streamline fiscal processes and reduce inefficiencies.

- Adaptation to Changing Economic Realities: India’s economic landscape is dynamic, with evolving challenges and opportunities. A comprehensive reevaluation allows fiscal policies to adapt to these changes, ensuring they remain relevant and effective.

- Fiscal Responsibility: To ensure fiscal sustainability, a reevaluation should assess the long-term fiscal health of both the central government and state governments. It can recommend measures to manage fiscal deficits and public debt responsibly.

Way forward

- Mandate of the 16th Finance Commission: The government should promptly constitute the 16th Finance Commission with a clear mandate to reexamine the tax-sharing principles and other related fiscal matters.

- Define Comprehensive Terms of Reference (ToR): The ToR for the 16th Finance Commission should be carefully formulated to guide the Commission in addressing the challenges posed by the GST regime and its impact on fiscal federalism.

- Pooling of Indirect Tax Sovereignty: Given the significant changes in the tax landscape, the Commission should comprehensively assess the pooling of indirect tax sovereignty between the Union and states under the GST system.

- Redesign Tax-sharing Principles: The Commission should undertake a thorough review and redesign of tax-sharing principles, especially with regard to the divisible pool, unsettled IGST, and settlement frequencies, in alignment with the GST structure.

- Distribution Criteria Reevaluation: Reevaluate the criteria for distributing the divisible pool among states, particularly for equalizing grants, to ensure that they align with the new consumption-based tax system and address regional imbalances effectively.

- Formalize Institutional Relationships: Formalize and strengthen the institutional relationship between the GST Council and the Finance Commission to facilitate seamless coordination, information exchange, and alignment of fiscal policies.

- Engage with Stakeholders: Engage in extensive consultations with relevant stakeholders, including state governments, economists, and experts, to gather diverse perspectives and insights.

Conclusion

- The 16th Finance Commission must reshape India’s fiscal federalism for the GST era by redefining the divisible pool, improving tax collection efficiency, revisiting distribution criteria, reviewing compensation, and formalizing institutional relationships. Flexible terms of reference are crucial for these essential reforms to align the fiscal system with the new tax paradigm and promote equitable growth.

Also read:

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Why normative recommendations of finance commissions remain on paper

From UPSC perspective, the following things are important :

Prelims level: Finance Commissions

Mains level: Finance Commissions and its role, recommendations and challenges in implementation

What is the news?

- This article critically examines the historical outcomes of the 13th FC and underscores the need for realistic expectations regarding the forthcoming 16th FC

Central idea

- The Finance Commissions (FC) in India play a crucial role in determining the fiscal framework for resource allocation between the Union and state governments. Established under Article 280 of the Constitution, the FCs provide recommendations on vertical devolution, horizontal distribution, and grants-in-aid. However, the effectiveness of these recommendations in achieving their intended objectives remains a matter of contention

Purpose and Scope of Finance Commissions

- Finance Commissions are constituted under Article 280 of the Constitution and their recommendations encompass three key areas: vertical devolution, horizontal distribution, and grant-in-aid.

- Vertical devolution focuses on Union to state transfers

- Horizontal distribution involves the allocation of resources between states based on a specific formula.

- Grant-in-aid, covered under Article 275, provides financial assistance to states deemed in need.

- It is important to note the distinction between grants and grant-in-aid, as the latter operates at arm’s length and offers more flexibility in terms of control.

Recommendations of the previous Finance Commission

13th Finance Commission Recommendations:

- Increase the number of court working hours using existing infrastructure.

- Enhance support to Lok Adalats.

- Provide additional funding to State Legal Services Authorities to enhance legal aid for the marginalized.

- Promote the use of Alternative Dispute Resolution (ADR) mechanisms.

- Enhance the capacity of judicial officers and public prosecutors through training programs.

- Support the creation of a judicial academy in every state for training purposes.

- Allocate funds for the setting up of specialized courts.

15th Finance Commission Recommendations:

- Gather quantifiable data on the level of various services available in different states.

- Collect corresponding unit cost data to estimate cost disabilities among states.

- Fill gaps in statistical data through the efforts of the Ministry of Statistics.

Challenges encountered in the implementation of Finance Commission recommendations

- Lack of Implementation of Homilies: The recommendations made by Finance Commissions, both at the Union and state levels, are often ignored as mere pious intentions. This indicates a lack of commitment and follow-through in translating the recommendations into concrete actions.

- Conditionalities and Expenditure Restrictions: The objections raised by some states in the article indicate challenges related to conditionalities attached to grants. Conditionalities may restrict the expenditure options of states, creating obstacles in implementing the recommended reforms.

- Inadequate Resource Allocation: The allocated funds for specific reforms may not be sufficient, leading to inadequate implementation. Financial constraints and competing budgetary priorities can limit the availability of resources needed to effectively execute the recommended measures.

- Lack of Coordination: The implementation of Finance Commission recommendations requires cooperation between the Union and state governments. Any lack of coordination or disagreements between these entities can hinder the execution of reforms

Way forward: Need for realistic expectations regarding the forthcoming 16th FC

- Acknowledging Implementation Challenges: Recognize the challenges and complexities involved in implementing Finance Commission recommendations, such as coordination issues, administrative capacity, and resistance to change. This understanding will help shape realistic expectations and strategies for addressing these challenges.

- Strengthening Implementation Mechanisms: Focus on improving the implementation mechanisms and processes. This includes enhancing coordination and cooperation between the Union and state governments, strengthening administrative capacity at all levels, and streamlining the implementation of conditionalities to facilitate smoother execution.

- Robust Monitoring and Evaluation: Establish effective monitoring and evaluation mechanisms to track the progress and outcomes of implemented reforms. Regular assessment will help identify implementation gaps and provide opportunities for course correction and improvement.

- Building Stakeholder Consensus: Foster stakeholder engagement and consensus-building to ensure the buy-in and ownership of recommended reforms. Engage relevant stakeholders, including government departments, civil society organizations, and local communities, to create a shared vision and collective commitment towards implementation.

- Learning from Past Experiences: Analyze past experiences and identify the reasons behind the limited implementation of previous recommendations. This will help inform future strategies, learning from the challenges faced and replicating successful implementation models.

- Advocacy and Public Awareness: Create awareness among the public about the importance of Finance Commission recommendations and their impact on governance and development. Foster advocacy efforts to generate public support and hold governments accountable for implementing the recommended reforms.

Conclusion

- Finance Commissions in India fulfill a critical role in determining fiscal transfers between the Union and state governments. However, the implementation of their recommendations often falls short of expectations due to various challenges and limitations. By critically analyzing the past experiences of Finance Commissions, it becomes evident that a more pragmatic approach is necessary to align expectations with the actual outcomes.

Also read:

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Finance Commission and the Challenges of Fiscal Federalism

From UPSC perspective, the following things are important :

Prelims level: Finance commission and its role, Concepts: Cess, surcharges, grants, freebies etc

Mains level: Fiscal Federalism, challenges and the role of Finance commission

Central Idea

- The government is set to appoint a Finance Commission in the coming months to address the crucial matter of distributing the Centre’s tax revenue among the States. This article examines the significance of the Finance Commission in India’s fiscal federalism, highlighting the changing dynamics post-reforms and the ensuing debates surrounding the horizontal distribution formula.

Evolution of the Finance Commission

- Constitutional Provision: The Finance Commission is a constitutional body established under Article 280 of the Indian Constitution. It was first constituted in 1951.

- Primary Objective: The primary objective of the Finance Commission is to recommend the distribution of financial resources between the Union (Centre) and the States.

- Five-Year Cycle: The Finance Commission is appointed every five years, or as specified by the President of India. The recommendations of the Commission cover a five-year period.

- Composition: The Commission consists of a Chairman and other members appointed by the President. The Chairman is usually a person with a background in economics, finance, or public administration.

- Terms of Reference: The President determines the terms of reference for each Finance Commission, which guide the Commission in its deliberations and recommendations.

Significance of the Finance Commission in India’s fiscal federalism

- Vertical and Horizontal Distribution: The Finance Commission determines the vertical share, which is the proportion of the Centre’s tax revenue that should be given to the States, ensuring a fair allocation of resources. It also formulates the horizontal sharing formula, which determines how this revenue should be distributed among the States.

- Addressing Fiscal Disparities: The Finance Commission plays a crucial role in addressing these disparities by providing financial transfers to less economically developed states. Through revenue deficit grants and other means, the Commission helps bridge the fiscal gap and supports states with limited revenue-raising capacity.

- Promoting Cooperative Federalism: The Finance Commission acts as an institutional mechanism that fosters cooperative federalism by facilitating intergovernmental fiscal transfers. It encourages collaboration and coordination between the Centre and the States, fostering a sense of shared responsibility in fiscal matters.

- Constitutional Mandate: The Finance Commission is constitutionally mandated under Article 280 of the Indian Constitution. Its existence and functioning are enshrined in the constitutional framework, ensuring its independence and impartiality in making recommendations.

- Five-Year Review Cycle: The regular appointment of the Finance Commission every five years ensures a periodic review of the fiscal arrangements between the Centre and the States. This allows for adjustments and revisions based on evolving economic and social realities, ensuring that fiscal transfers remain relevant and effective.

- Expertise and Recommendations: The Finance Commission comprises experts in the fields of economics, finance, and public administration. Its recommendations are based on in-depth analysis, consultations, and assessments of various factors, including population, fiscal capacity, and development needs. These recommendations provide valuable insights and guidance to the Centre and the States in fiscal decision-making.

- Resolving Fiscal Conflicts: The Finance Commission helps resolve conflicts and disputes between the Centre and the States regarding fiscal matters. By providing an independent and objective platform for negotiation and deliberation, it promotes a sense of fairness and transparency in fiscal resource allocation.

- Strengthening Fiscal Discipline: The Finance Commission plays a role in promoting fiscal discipline and accountability. By assessing the fiscal performance and needs of the States, it encourages responsible fiscal behavior and discourages imprudent spending practices

Facts for Prelims

| Aspect | Vertical Distribution | Horizontal Distribution |

| Definition | Allocation of the Centre’s tax revenue between the Centre and the States | Allocation of funds among the States |

| Determined by | Finance Commission | Finance Commission |

| Factors considered | Fiscal capacity, needs of the States, population figures, and relevant indicators | Population, area, fiscal capacity, demographic trends, development indicators, and relevant parameters |

| Objective | Provide a fair and equitable share of revenue to the States | Promote equitable development and address regional imbalances |

| Purpose | Ensure States have sufficient resources for expenditure requirements and promote balanced development | Provide greater financial support to States with lower fiscal capacity and greater development needs |

| Focus | Centre-State distribution of revenue | State-State distribution of funds |

| Outcome | Ensures fair allocation of revenue between the Centre and the States | Reduces disparities and fosters balanced growth among the States |

Changing dynamics post reforms

- Decreased Role of Plan Financing: In the pre-reform era, the Centre had the flexibility to compensate States through plan financing. However, post-reforms, there has been a decline in fresh investments in public sector undertakings (PSUs) and the abolition of the Planning Commission in 2014. As a result, the Finance Commission has become the primary mechanism for the vertical and horizontal distribution of resources, making its role more critical.

- Devolution of Tax Revenues: With the amendment of the Constitution in 2000, States were given a share in the Centre’s tax revenue pool. This devolution of tax revenues has increased the significance of the Finance Commission in determining the distribution of funds between the Centre and the States.

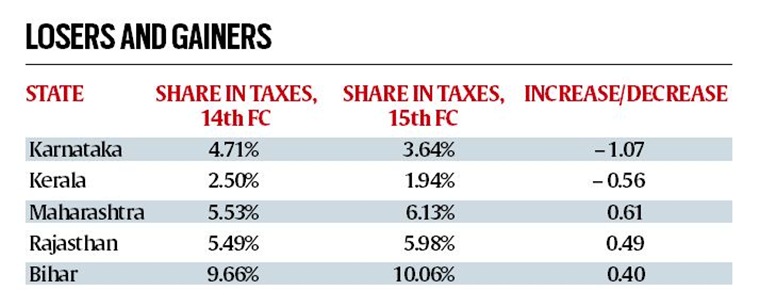

- Shift in Population Figures: The use of population figures in determining the distribution of resources has seen a shift from the earlier practice of using 1971 census data to considering 2011 census data. This shift has led to debates and controversies, particularly among States that have successfully controlled population growth rates, as it can affect their share of devolution.

- Deepening Faultlines: In recent years, faultlines between States have deepened along political, economic, and fiscal dimensions. The outcome of elections and regional disparities in terms of infrastructure, private investment, social indicators, and the rule of law have widened the north-south gap and brought regional imbalances into focus. Managing these faultlines while ensuring equitable distribution poses challenges for the Finance Commission.

- Concerns of Fiscal Incapacity vs. Fiscal Irresponsibility: The Finance Commission faces the challenge of determining the extent to which a State’s deficit is due to its fiscal incapacity or fiscal irresponsibility. Striking a balance between supporting deficit-ridden States without penalizing fiscally responsible ones is a complex task, as providing more to one State would mean giving less to others.

- Changing Economic Landscape: The post-reform period has witnessed shifts in India’s economic landscape, with some states experiencing higher growth rates and greater fiscal capacity compared to others. This dynamic requires the Finance Commission to consider the changing economic realities and ensure that the distribution formula reflects the current context

Addressing the concerns related to cesses and surcharges

- Clear Guidelines: The Finance Commission should lay down clear guidelines on when and under what circumstances cesses and surcharges can be levied. These guidelines should ensure that cesses and surcharges are not used as routine measures but rather as exceptional instruments to address specific needs or challenges.

- Cap on Amount Raised: The Finance Commission can suggest a formula or mechanism to cap the amount that can be raised through cesses and surcharges. This would prevent excessive reliance on these instruments and ensure that they do not become a substantial portion of the Centre’s total tax revenue.

- Transparency and Accountability: The government should enhance transparency and accountability in the utilization of funds generated through cesses and surcharges. It should provide regular reports on the utilization of these funds, demonstrating how they contribute to the intended purposes and benefit the states and the overall economy.

- Consultation with States: The Finance Commission should engage in extensive consultations with states while formulating guidelines regarding cesses and surcharges. States should have the opportunity to provide their input, share their concerns, and suggest ways to strike a balance between the Centre’s revenue requirements and the states’ financial autonomy.

- Alignment with Fiscal Responsibility: Any levies on cesses and surcharges should be in line with the principles of fiscal responsibility and budget management. The Finance Commission can ensure that these instruments are used judiciously and do not undermine the fiscal discipline goals set by the FRBM Act.

- Review and Evaluation: Regular review and evaluation of the impact of cesses and surcharges should be conducted to assess their effectiveness in achieving the intended objectives. The Finance Commission can play a crucial role in monitoring the usage of these instruments and recommending necessary adjustments based on the evaluation outcomes.

Implementing restraint on freebies

- Clear Definition: Establishing a clear definition of what constitutes a freebie is crucial to avoid ambiguity and misuse of resources. It should encompass measures that go beyond essential public services and infrastructure development and instead focus on non-essential giveaways or subsidies.

- Fiscal Responsibility and Budgetary Constraints: The Finance Commission can emphasize the importance of adhering to fiscal responsibility guidelines and staying within budgetary constraints. This ensures that resources are allocated judiciously and in a sustainable manner, avoiding the accumulation of unsustainable debt.

- Prioritization of Essential Services: Encouraging governments to prioritize essential public services, such as healthcare, education, and infrastructure, over non-essential freebies. This ensures that resources are allocated to areas that have a more significant and long-lasting impact on the overall well-being and development of the population.

- Evaluation of Impact: Regular evaluation of the impact of freebies on the economy, fiscal health, and the intended beneficiaries is essential. This evaluation can help identify any unintended consequences, potential wastage of resources, or negative effects on economic growth.

- Public Awareness and Discourse: Creating public awareness about the implications of excessive freebies and the importance of responsible fiscal management. Encouraging open discourse and dialogue among citizens, policymakers, and experts can foster a deeper understanding of the long-term consequences of unsustainable giveaways.

- Role of the Finance Commission: The Finance Commission can play a pivotal role in setting guidelines and recommendations for restraint on freebies. This includes providing advice on responsible fiscal management and ensuring that resource allocation aligns with long-term development goals.

Conclusion

- The Finance Commission plays a crucial role in India’s fiscal federalism. To address concerns regarding cesses, surcharges, and freebies, the Commission must provide clear guidelines, ensure transparency, and emphasize long-term fiscal sustainability. Stakeholder consultation, periodic evaluation, and public awareness are key to maintaining a balance between meeting welfare needs and promoting responsible fiscal management.

Also read:

| The curious case of Fiscal Federalism in India |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

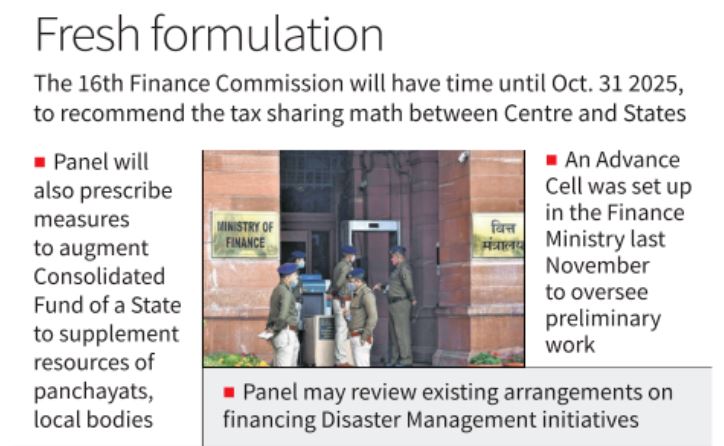

16th Finance Commission to be constituted in November

From UPSC perspective, the following things are important :

Prelims level: Finance Commission

Mains level: Read the attached story

The Union government is gearing up to constitute the Sixteenth Finance Commission in November this year to recommend the formula for sharing revenues between the Centre and the States for the five-year period beginning 2026-27.

What is the Finance Commission?

- The Finance Commission (FC) was established by the President of India in 1951 under Article 280 of the Indian Constitution.

- It was formed to define the financial relations between the central government of India and the individual state governments.

- The Finance Commission (Miscellaneous Provisions) Act, 1951 additionally defines the terms of qualification, appointment and disqualification, the term, eligibility and powers of the Finance Commission.

- As per the Constitution, the FC is appointed every five years and consists of a chairman and four other members.

- Since the institution of the First FC, stark changes in the macroeconomic situation of the Indian economy have led to major changes in the FC’s recommendations over the years.

Constitutional Provisions

Several provisions to bridge the fiscal gap between the Centre and the States were already enshrined in the Constitution of India, including Article 268, which facilitates levy of duties by the Centre but equips the States to collect and retain the same.

Article 280 of the Indian Constitution defines the scope of the commission:

- Who will constitute: The President will constitute a finance commission within two years from the commencement of the Constitution and thereafter at the end of every fifth year or earlier, as the deemed necessary by him/her, which shall include a chairman and four other members.

- Qualifications: Parliament may by law determine the requisite qualifications for appointment as members of the commission and the procedure of selection.

- Terms of references: The commission is constituted to make recommendations to the president about the distribution of the net proceeds of taxes between the Union and States and also the allocation of the same among the States themselves. It is also under the ambit of the finance commission to define the financial relations between the Union and the States. They also deal with the devolution of unplanned revenue resources.

Important functions

- Devolution of taxes: Distribution of net proceeds of taxes between Center and the States, to be divided as per their respective contributions to the taxes.

- Grants-in-aid: Determine factors governing Grants-in-Aid to the states and the magnitude of the same.

- Augment states fund: To make recommendations to the president as to the measures needed to augment the Fund of a State to supplement the resources of the panchayats and municipalities in the state on the basis of the recommendations made by the finance committee of the state.

- Any financial function: Any other matter related to it by the president in the interest of sound finance.

Members of the Finance Commission

- The Finance Commission (Miscellaneous Provisions) Act, 1951 was passed to give a structured format to the finance commission and to bring it to par with world standards.

- It laid down rules for the qualification and disqualification of members of the commission, and for their appointment, term, eligibility and powers.

- The Chairman of a finance commission is selected from people with experience of public affairs. The other four members are selected from people who:

- Are, or have been, or are qualified, as judges of a high court,

- Have knowledge of government finances or accounts, or

- Have had experience in administration and financial expertise; or

- Have special knowledge of economics

Key challenges ahead for 16th FC

- Overlap with GST Council: A key new challenge for the 16th FC would be the co-existence of another permanent constitutional body, the GST Council.

- Conflict of interest: The GST Council’s decisions on tax rate changes could alter the revenue calculations made by the Commission for sharing fiscal resources.

- Feasibility of recommendations: Centre usually takes the Commission’s recommendations on States’ share of tax devolution and the trajectory for fiscal targets into account, and ignores most other suggestions.

Major outstanding recommendations

- Creating a Fiscal Council: The 15th FC has suggested creating a Fiscal Council where Centre and States collectively work out India’s macro-fiscal management challenges, but the government has signalled there is no need for it, he pointed out.

- Creating a non-lapsable fund for internal security: The centre accepted to set up a non-lapsable fund for internal security and defense ‘in principle’, its implementation still has to be worked out.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Process to set up 16th Finance Commission set to kick off soon

From UPSC perspective, the following things are important :

Prelims level: Finance Commission

Mains level: Not Much

The Centre will soon kick off the process to set up the Sixteenth Finance Commission, with the Finance Ministry likely to notify the terms of reference.

What is the Finance Commission?

- The Finance Commission (FC) was established by the President of India in 1951 under Article 280 of the Indian Constitution.

- It was formed to define the financial relations between the central government of India and the individual state governments.

- The Finance Commission (Miscellaneous Provisions) Act, 1951 additionally defines the terms of qualification, appointment and disqualification, the term, eligibility and powers of the Finance Commission.

- As per the Constitution, the FC is appointed every five years and consists of a chairman and four other members.

- Since the institution of the First FC, stark changes in the macroeconomic situation of the Indian economy have led to major changes in the FC’s recommendations over the years.

Constitutional Provisions

Several provisions to bridge the fiscal gap between the Centre and the States were already enshrined in the Constitution of India, including Article 268, which facilitates levy of duties by the Centre but equips the States to collect and retain the same.

Article 280 of the Indian Constitution defines the scope of the commission:

- Who will constitute: The President will constitute a finance commission within two years from the commencement of the Constitution and thereafter at the end of every fifth year or earlier, as the deemed necessary by him/her, which shall include a chairman and four other members.

- Qualifications: Parliament may by law determine the requisite qualifications for appointment as members of the commission and the procedure of selection.

- Terms of references: The commission is constituted to make recommendations to the president about the distribution of the net proceeds of taxes between the Union and States and also the allocation of the same among the States themselves. It is also under the ambit of the finance commission to define the financial relations between the Union and the States. They also deal with the devolution of unplanned revenue resources.

Important functions

- Devolution of taxes: Distribution of net proceeds of taxes between Center and the States, to be divided as per their respective contributions to the taxes.

- Grants-in-aid: Determine factors governing Grants-in-Aid to the states and the magnitude of the same.

- Augment states fund: To make recommendations to the president as to the measures needed to augment the Fund of a State to supplement the resources of the panchayats and municipalities in the state on the basis of the recommendations made by the finance committee of the state.

- Any financial function: Any other matter related to it by the president in the interest of sound finance.

Members of the Finance Commission

- The Finance Commission (Miscellaneous Provisions) Act, 1951 was passed to give a structured format to the finance commission and to bring it to par with world standards.

- It laid down rules for the qualification and disqualification of members of the commission, and for their appointment, term, eligibility and powers.

- The Chairman of a finance commission is selected from people with experience of public affairs. The other four members are selected from people who:

- Are, or have been, or are qualified, as judges of a high court,

- Have knowledge of government finances or accounts, or

- Have had experience in administration and financial expertise; or

- Have special knowledge of economics

Key challenges for 16th FC

- Overlap with GST council: A key new challenge for the 16th FC would be the co-existence of another permanent constitutional body, the GST Council.

- Conflict of interest: The GST Council’s decisions on tax rate changes could alter the revenue calculations made by the Commission for sharing fiscal resources.

- Feasibility of recommendations: Centre usually takes the Commission’s recommendations on States’ share of tax devolution and the trajectory for fiscal targets into account, and ignores most other suggestions.

Major outstanding recommendations

- Creating a Fiscal Council: The 15th FC has suggested creating a Fiscal Council where Centre and States collectively work out India’s macro-fiscal management challenges, but the government has signalled there is no need for it, he pointed out.

- Creating a non-lapsable fund for internal security: The centre accepted to set up a non-lapsable fund for internal security and defense ‘in principle’, its implementation still has to be worked out.

Crack Prelims 2023! Talk to our Rankers

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

The curious case of Fiscal Federalism in India

From UPSC perspective, the following things are important :

Prelims level: Finance commission, NITI Aayog

Mains level: Issues with cooperative Federalism

Context

- NITI Aayog has not taken any major steps since its constitution to promote cooperative federalism. Contrary to its public statements on promoting cooperative federalism, the Government of India has been accused of doing exactly the opposite. The following instances clearly demonstrate as to how the central government’s policies have undermined the spirit of federalism and eroded the autonomy of the States.

Why the states are angry over hypocrisy of the Centre?

- Centre raises off budget borrowings states are restricted: The borrowings by corporations against State guarantees are mostly used for capital investment. The Centre has also been raising off Budget borrowings but mainly for meeting revenue expenditure.

- CAG report on extra budgetary resources: The Comptroller and Auditor General of India (C&AG) Report on the Compliance of FRBM Act for 2017-18 and 2018-19 pointed out as many as eight instances of meeting revenue expenditure through Extra Budgetary Resources (EBR).

- Unjustified limitations on states: Revenue expenditure met through EBR by the Centre amounted to ₹81,282 crore in 2017-18 and ₹1,58,107 crore in 2018-19. Such borrowings were not reflected in the Budget of the central government. In view of this, treating off Budget borrowings of State corporations as States’ borrowings retrospectively is totally unjustified.

Unhappiness about the grants by the finance commission’s recommendations?

- Special grants are not given to states: The Fifteenth Finance Commission, in its first report, had recommended a special grant to three States amounting to ₹6,764 crore to ensure that the tax devolution in 2020-21 in absolute terms should not be less than the amount of devolution received by these States in 2019-20. This recommendation was not accepted by the Union Government.

- Nutritional grants are accepted: the recommendation relating to grants for nutrition amounting to ₹7,735 crore was not accepted.

- Grants to states are refused by the Centre: A similar approach has been followed by the Union Government with regard to grants to States recommended by the Finance Commission for the period 2021-26.

- Sector and state specific grants: The sector specific grants and State specific grants recommended by the Commission amounting to ₹1,29,987 crore and ₹49,599 crore, respectively, have not been accepted. This clearly demonstrates that the Union Government has undermined the stature of the institution of the Finance Commission and cooperative federalism.

How borrowing of the states is controlled by the Centre?

- Changes in off budget borrowing norms: decision to treat off Budget borrowings from 2021-22 onwards serviced from the State budgets as States’ borrowings and adjusting them against borrowing limits under Fiscal Responsibility and Budget Management (FRBM) in 2022-23 and following years is against all norms.

- No recommendations by finance commission: This is the first time that the Government of India is proposing to treat off Budget borrowings as government borrowings retrospectively from 2021-22. The Government of India has indicated that such a decision is in accordance with the recommendation of the Finance Commission. In fact, there is no recommendation to this effect by the Fifteenth Finance Commission. The Finance Commission recommended that governments at all tiers may observe strict discipline by resisting any further additions to the stock of off Budget transactions.

- No amendment to FRBM act: It observed that in view of the uncertainty that prevails now, the timetable for defining and achieving debt sustainability may be examined by a high-powered intergovernmental group and that the FRBM Act may be amended as per the recommendations of this group to ensure that the legislations of the Union and the States are consistent. No such group has been appointed so far by the Centre.

Cess and Surcharge- A tool to raise revenue for Centre not available to the states

- Rising share of cess and surcharges: The government has been resorting to the levy of cesses and surcharges, as these are not shareable with the States under the Constitution. The share of cesses and surcharges in the gross tax revenue of the Centre increased from 13.5% in 2014-15 to 20% in the Budget estimates for 2022-23.

- States don’t get all share in divisible pool: Though the States’ share in the Central taxes is 41%, as recommended by the Fifteenth Finance Commission, they only get a 29.6% share because of higher cesses and surcharges.

- Undermining the purpose of cess: The C&AG in its Audit Report on Union Government Accounts for 2018-19 observed that of the ₹2,74,592 crore collected from 35 cesses in 2018-19, only ₹1,64,322 crore had been credited to the dedicated funds and the rest was retained in the Consolidated Fund of India. This is another instance of denying States of their due share as per the constitutional provisions.

- Increasing centrally sponsor scheme and burden on state: Committee after committee appointed by the Government of India has emphasised the need to curtail the number of Centrally Sponsored Schemes (CSS) and restrict them to a few areas of national importance. But, what the Government of India has done is to group them under certain broad umbrella heads (currently 28). In addition, in 2015, the Centre increased the States’ share in a number of CSS, thereby burdening States. Most of the CSS are operated in the subjects included in the State list. Thus, States have lost their autonomy.

- NITI Aayoge recommendations are not accepted: The Sub-Committee of Chief Ministers appointed by NITI Aayog has recommended a reduction in the number of schemes and the introduction of optional schemes. These recommendations have not been acted upon.

Conclusion

- Finance commission is balancing wheel of fiscal federalism. Share of states in central taxes may have increased but cess and surcharges have also increased. Off budget borrowing on states can lifted provided should reduce the unnecessary freebies in the state budget.

Mains Question

Q. Fiscal federalism is tilted in favour of Centre. Elaborate. How Cess and surcharges are discriminatory against the state governments?

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Finance Commission’s Approach to Equitable Delivery of Goods and Services

From UPSC perspective, the following things are important :

Prelims level: NA

Mains level: Equitable delivery

Context

- 15th Finance commission on horizontal devolution agreed that the Census 2011 population data better represents the present need of States, to be fair to, as well as reward, the States which have done better on the demographic front, Finance commission has assigned a 12.5 per cent weight to the demographic performance criterion. Population, area, forest and ecology, demographic performance, tax efforts, income and distance are the criteria for horizontal distribution of funds.

Why equitable delivery is necessary in the country?

- To fulfil the need of basket of Goods: There is a basket of goods and services that should be delivered by the State. It is best not to call them public goods, since “public goods” have a specific meaning for economists and this basket has items that are typically collective private goods.

- To achieve Aantodaya approach (last person): Curlew Island is in the Andaman and Nicobar Islands. Until the 2011 Census, it had a population of two. Pulomilo Island, also in Andaman and Nicobar, had a population of 20 in 2011. At the time of elections, we read of astounding attempts made, so that voters in remote locations can vote. No one should be disenfranchised because of remoteness of location. By the same token, a resident, regardless of location, must be entitled to that basket.

- To achieve poverty alleviation: The quality of public services affects economic growth via its impact on poverty alleviation, human capital formation and corruption.

What are the Problems with Equitable delivery targets?

- High cost of delivery: States can have differential sources of revenue. Alternatively, the cost of delivering that basket may vary across geographical zones.

- Problems associated with migration: Over time, villages of course get depopulated. They are reclassified, get absorbed into larger agglomerations, or disappear because of migration.

How equitable delivery can be achieved?

- State need to take honest responsibility: The State cannot abdicate its responsibility of providing the basket.

- Economic compulsion: Migration is a voluntary decision, often driven by the pull (and push) of economic forces. That voluntary decision cannot be replaced by fiat.

- Dividing the pool between the governments: The Union Finance Commission has a vertical task, dividing the divisible pool between the Union government and states.

- Adjusting to the criteria set by FC: It also has a horizontal task, dividing State share between different states. Accordingly, from the 1st to the 15th, Finance commission have adopted different formulae, with an attempt to also create incentives, by attaching weights to fiscal efficiency and even demographic performance.

- This leaves variables like population, geographical area, income distance, infrastructure distance and forest cover:

- expenditure equalisation based on needs/costs of public services;

- Revenue equalisation measured by the ability of the state to raise revenue from one or more sources; and

- Macro indicators covering broader economic or non-economic indicators that approximate fiscal capacity, where data constraints make it difficult to apply the other approaches.

- Addressing Geographic area and population: Needs/costs are sought to be measured through geographical area and population. All Finance Commissions have used area as another criterion in the devolution formula on the ground of need — the larger the area, greater is the expenditure requirement for providing comparable services.

Conclusion

- Equitable access to public goods and services in low income and inequal (economic inequality) country like India is cumbersome task. Finance commission is trying their best for equitable allocation of resources.

Mains Question

Q. How Equity is different from equality? What is the finance commission’s criteria for horizontal allocation of resources among the states ?

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

Skewed divisible pool

From UPSC perspective, the following things are important :

Prelims level: Finance commission

Mains level: Fiscal federalism

Context

Context

- The centralisation of fiscal powers in India has been blamed for the poor fiscal health of the states.

Why in news?

- Chief Ministers expressed their concern about dwindling State revenues in a NITI Aayog meeting chaired by the Prime Minister.

- They sought a higher share in the divisible pool of taxes and an extension of GST compensation, both of which have long remained a bone of contention between the Union government and the States.

Need for financial devolution

- To strengthen democracy at grass root level with more revenue resources for better service delivery.

- To increase accountability to people so performance can be realized as direct contact with people.

What is divisible pool of taxes?

- The divisible pool is that portion of gross tax revenue which is distributed between the Centre and the States. The divisible pool consists of all taxes, except surcharges and cess levied for specific purpose, net of collection charges.

What is fiscal federalism?

- Fiscal federalism refers to how federal, state, and local governments share funding and administrative responsibilities within our federal system. The funding for these programs comes from taxes and fees.

Poor state of state finances

- Stagnant revenue: Since States cannot raise tax revenue because of curtailed indirect tax rights — subsumed in GST, except for petroleum products, electricity and alcohol — the revenue has been stagnant at 6% of GDP in the past decade.

- Distorted expenditure: While States lost their capacity to generate revenue by surrendering their rights in the wake of the Goods and Services Tax (GST) regime, their expenditure pattern too was distorted by the Union’s intrusion, particularly through its centrally sponsored schemes.

- Decline in share: The ability of States to finance current expenditures from their own revenues has declined from 69% in 1955-56 to less than 38% in 2019-20.

- Stress on finance: States’ financial health had taken a turn for the worse with the implementation of the Ujwal DISCOM Assurance Yojana, farm loan waivers, as also the slowdown in growth in 2019- 20.

Key fact to remember

Finance Commission keeps tax devolution for states at 41% in FY22

How fiscal centralisation impacts on states?

- Cut in the corporate tax: The recent drastic cut in corporate tax, with its adverse impact on the divisible pool, and ending GST compensation to States have had huge consequences.

- States paying high interest rates: States are forced to pay differential interest — about 10% against 7% — by the Union for market borrowings.

- Centrally sponsored schemes curbing autonomy: There are 131 centrally sponsored schemes, with a few dozen of them accounting for 90% of the allocation, and States required to share a part of the cost.

Suggestions for strong fiscal federalism

- Creation of federal institution: We need to create another institution in the form of a GST state secretariat that can bring together senior officers from the Centre and states in an institutional forum registered under the Society Act.

- State Finance Commissions: should be accorded the same status as the Union Finance Commission and the 3Fs of democratic decentralization (funds, functions, and functionaries) should be implemented properly.

- Robust GST regime: Transparency, simplification and rationalisation of GST will help states to recover soon.

Way Forward

- Relook on various exemptions to rationalise the taxes/levies

- Augmentation of Tax Administration Structure

- Technology-based Tax Administration may also be further expanded to cover even utility charges like water, street lights, sanitation charges, etc.

Conclusion

- It is important now to rethink the design and structure of a genuine fiscal partnership, which should not merely be a race to garner more resources, but a creative attempt to move towards a vibrant Indian value chain that can catapult India’s growth rate closer to the quest for double-digit growth.

Mains question

Q. Why it is important now to rethink the design and structure of a genuine fiscal partnership? Discuss this in context of Skewed divisible pool and state of fiscal federalism in India.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Finance Commission – Issues related to devolution of resources

fiscal federalism in India

From UPSC perspective, the following things are important :

Prelims level: Finance Commission

Mains level: Paper 2- Issues with fiscal federalism in India

Context

The centralisation of fiscal powers in India has been blamed for the poor fiscal health of the states.

Centralisation of fiscal powers: A background

- Jawaharlal Nehru believed that socio-economic inequities could be addressed through the planning process.

- A degree of centralisation in fiscal power was required to address the concerns of socio-economic and regional disparities.

- As a result asymmetric federalism is inherent to the Indian Constitution.

- India was never truly federal — it was a ‘holding together federalism’ in contrast to the ‘coming together federalism,’ in which smaller independent entities come together to form a federation (as in the United States of America).