Under panchamrit Targets at COP26, India committed to achieving 50 percent of its installed electricity capacity from non-fossil (clean and renewable) sources by 2030.

Progress towards 50% energy needs from renewables – Justification

Non-fossil capacity reached around 50% of installed capacity in 2025, ahead of the 2030 deadline.

India stands 4th globally in Renewable Energy Installed Capacity, 4th in Wind Power capacity and 3rd in Solar Power capacity (as per IRENA RE Statistics 2025).

India focuses on five key priorities to achieve its 2030 target of 500 GW non-fossil capacity.

Better Contracts: Long-term power deals to attract investors.

Stronger Grids: Modern grids and battery storage for steady power supply.

Make in India: Boosting local production of solar panels and wind turbines.

Smart Land Use: Using land wisely with floating solar and solar on farms.

Easy Financing: Making funds available to support clean energy projects.

Government efforts

National Solar Mission – Expansion of solar capacity at utility and rooftop level.

PM-KUSUM – Solarisation of agricultural pumps and rural feeders.

National Wind-Solar Hybrid Policy – Maximises land and grid utilisation.

PM Surya Ghar Muft Bijli Yojana – Accelerates residential rooftop solar.

Institutional mechanisms

Green Grids Initiative under OSOWOG

BEE and PAT Scheme – Promote energy efficiency.

Economic incentives

PLI Scheme for Solar PV Modules and Batteries

Viability Gap Funding and Capital Subsidies

Green bonds for clean energy projects.

Global efforts and partnerships

Technology transfer and funding through ISA, IBSA, G20

Participation in Just Energy Transition Partnerships (JETP) and multilateral climate funds.

Challenges

Policy inconsistency (continued approval of coal plants) weakens investor confidence in renewables.

Financial Challenges

India needs nearly

High upfront capital costs and slow RoI discourage private investors.

Limited availability of low-cost green finance for small and medium developers.

Intermittency issue and limited energy storage solutions.

Grid integration problems due to weak transmission and distribution.

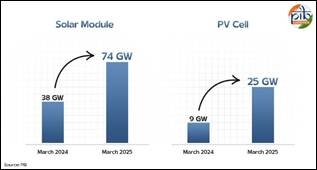

Import Dependence. Eg- China supplied ~56% of India’s solar cells in FY2024. 100% import-dependent for lithium, cobalt, nickel, graphite, copper.

Skilled manpower shortage in advanced RE technologies.

Land & Environmental Constraints – Eg- Sillahalla Hydro Project (Tamil Nadu) raised concerns over biodiversity loss and displacement.

E-Waste – No comprehensive solar recycling policy or sufficient recycling infrastructure

Delayed payments and PPA renegotiations/cancellations coupled with weak financial capacity of DISCOMS impact market stability

How shifting subsidies from fossil fuels to renewables will help

Level playing field – Removing fossil-fuel subsidies makes RE more competitive and attractive.

Lower cost of clean energy – Redirected subsidies can reduce tariffs of solar and wind

Crowding in private investment due to higher returns and lower risk

Savings can be used for battery storage, smart grids, green corridors and EV charging networks.

Reduced fossil fuel demand due to higher prices

Global leadership – Strengthens India’s position in climate negotiations and green diplomacy.

Way Forward

Optimize Land and Water Resources – Eg- Omkareshwar Floating Solar Park.

Develop Renewable Energy Clusters with single-window clearances and fiscal incentives.

Leverage Emerging Technologies – Eg- blockchain-based P2P renewable energy trading

Expand Renewable Infrastructure – Scale rooftop solar, microgrids and solar pumps for rural electrification and off-grid solutions.

Circular Waste-to-Energy Parks using anaerobic digestion, gasification and pyrolysis. Eg- Jamnagar

India’s energy transition can help realise SDG 7 (Affordable and Clean Energy), SDG 13 (Climate Action), and SDG 9 (Industry, Innovation, and Infrastructure).