Why in the News

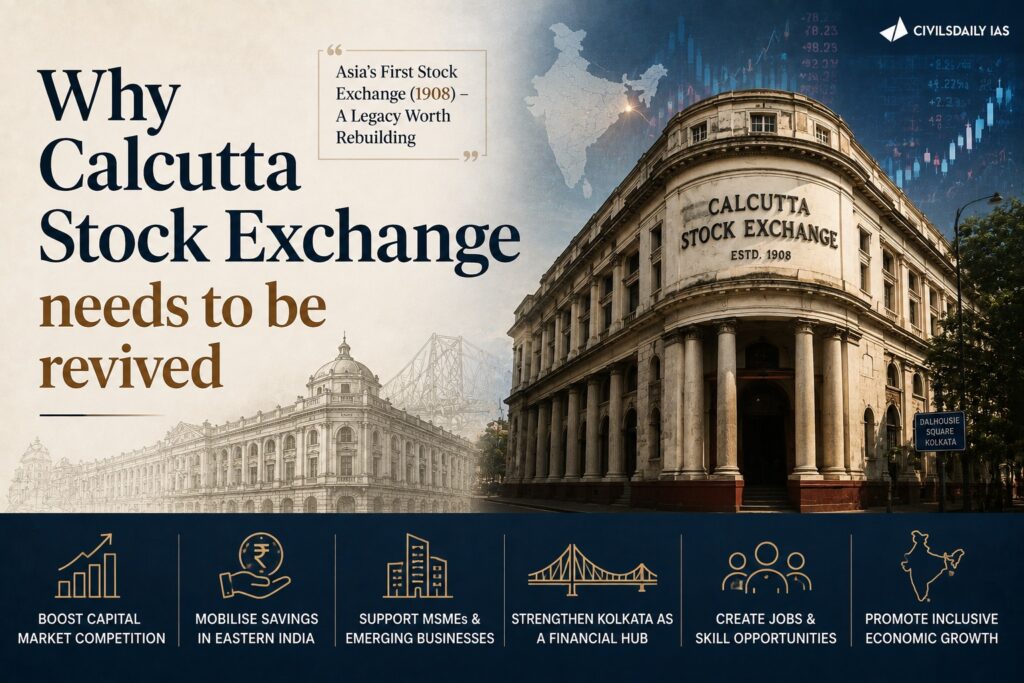

The West Bengal government’s 2026–27 budget backs the revival of the Calcutta Stock Exchange (CSE) as India’s third exchange dedicated to pre-commercial deep tech listings. The proposal exposes a gap in India’s capital markets: intellectual property driven companies in semiconductors, biotech and space with years to go before revenue have no domestic listing path, forcing them toward foreign exchanges or private capital alone.

What is the Calcutta Stock Exchange?

- Calcutta Stock Exchange (CSE): It was established in 1908, months after 8,000 Indian households financed Tata Steel by public subscription. CSE is India’s oldest stock exchange, now largely dormant, whose revival the West Bengal government’s 2026-27 budget backs.

- Pre-commercial listing: A pre-commercial listing allows a company to raise public capital before it has meaningful revenue, based on milestone data such as clinical trial results or chip tape-out yields rather than financial performance.

How has China built a market for pre-revenue deep tech listings?

- China, STAR Market, disclosure gated deep-tech board: Opened in Shanghai in 2019 amid tightening American sanctions, the STAR Market lists companies based on milestone disclosure rather than profitability, and has raised about $160 billion across 592 companies in seven years.

- China, STAR 50 index, performance signal: The STAR 50 index rose 64 percent in the first half of 2026, and Cambricon, a chip designer that listed unprofitable in 2020, became the board’s first trillion-renminbi company. This gives the evidence that the model can produce durable winners.

- China, sectoral breadth, widening aperture: The STAR Market’s listing scope has expanded into artificial intelligence, robotics and space technology, tracking China’s evolving strategic priorities rather than staying fixed to its original mandate.

What reforms would let the Calcutta Stock Exchange fill this gap?

- Milestone gated listing regime: Listings would be gated by disclosure and technical milestones, clinical data for biopharma, tape-out and yield data for semiconductors, flight heritage for aerospace, rather than financial performance thresholds.

- Accredited investor gate: A consolidated accredited investor definition would give family offices, global institutions and Alternative Investment Fund managers preferred initial access, with retail participation phased in as disclosure accumulates.

- Formalised unlisted shares dealer network: The existing informal grey market for unlisted shares, currently offline trading at one-way quotes, would be consolidated into a regulated dealer network under CSE.

- Interoperable settlement: Trades would settle through existing clearing corporations under interoperability, with mainboard migration to NSE or BSE available as a right once a listing has seasoned on CSE.

- Issuer-sponsored research: Research coverage would be seeded through issuer-sponsored analyst reports to build an information ecosystem where currently there is no listed deep-tech paper to analyse.

What are the challenges to reviving the Calcutta Stock Exchange?

- Fragmentation risk: A third exchange adds a distinct venue for investors and issuers to track, raising the risk of fragmented liquidity relative to NSE and BSE.

- CSE’s institutional history: The exchange has a complicated operating history and would need fresh institutional capital and governance separated from its existing broker ownership to be credible as a new venue.

- Market for lemons risk: Pre-commercial listings without profitability as a filter raise the risk of low quality issuers exploiting the milestone disclosure regime, countered in the proposal only through lock-ins, shorting and surveillance built in by design.

- Retail investor protection: Phasing retail investors in only as disclosure accumulates depends on regulators enforcing that sequencing strictly, since retail demand for deep-tech exposure could otherwise push premature access.

Conclusion

The case for reviving the Calcutta Stock Exchange rests on India lacking any domestic listing path for companies whose value lies in intellectual property years away from revenue. Whether the exchange can be rebuilt with the governance and investor protection safeguards the proposal outlines, rather than repeating its earlier institutional troubles, will determine if it becomes a genuine third venue alongside NSE and BSE.

Back2Basics

| Feature / Details | BSE (Bombay Stock Exchange) | NSE (National Stock Exchange) |

| Establishment | 1875 (oldest in Asia) | 1992 (started with a modern, digital system) |

| Main Index | SENSEX (Top 30 Companies) | NIFTY 50 (Top 50 Companies) |

| Listed companies | Approximately 5,900+ (more companies) | Approximately 2,900+ (fewer companies) |

| Trading Volume | Low (popular for small & mid-cap shares) | Very high (leader in cash & derivatives market) |

| Global ranking | One of the largest exchanges in the world | World’s No. 1 in derivatives contracts trading |

PYQ Relevance

[UPSC 2023] Consider the following markets: 1. Government Bond Market 2. Call Money Market 3. Treasury Bill Market 4. Stock Market.

How many of the above are included in capital markets? (a) Only one (b) Only two (c) Only three (d) All four.

Answer: (b)