The 101st Constitutional Amendment Act, 2016 introduced the Goods and Services Tax (GST) with effect from July 1, 2017. It was a landmark tax reform aimed at creating a “One Nation, One Tax, One Market” framework.

Significance of the 101st Amendment Act

Unified Taxation System – Subsumed 17 central & state taxes and 23 cesses, removing cascading effects.

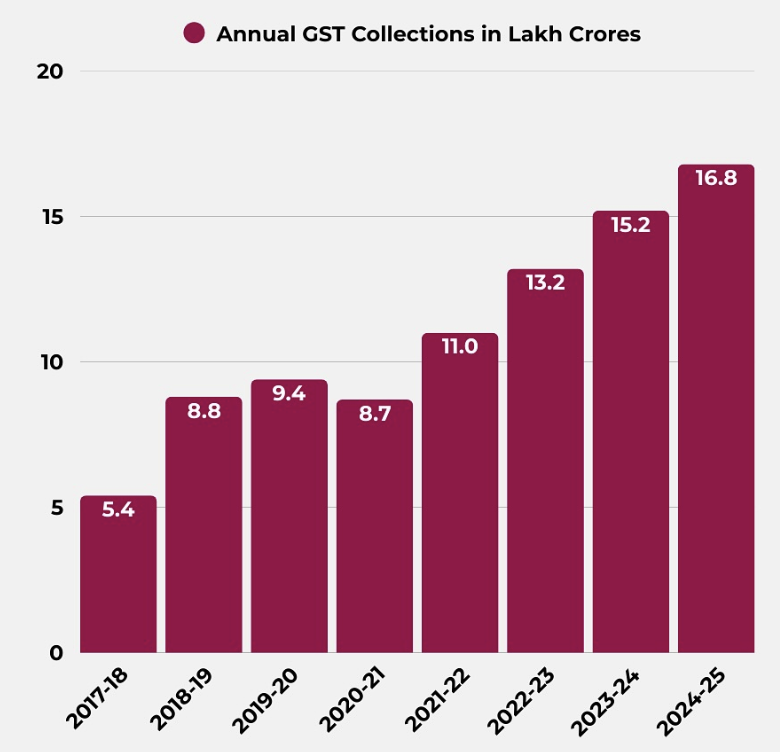

Expansion of Tax Base – Taxpayers increased from 66 lakh (2017) to over 1.5 crore (2024).

Revenue Growth – Tax base rose from over a decade (CAGR 14.4%); average monthly collections near .

Economic Efficiency – Eliminated cascading effects of taxation and reduced compliance costs.

Household Savings – Reduced overall tax burden, saving families ~4% on monthly expenses.

Ease of Doing Business – Unified national market and reduced transport time by 33%, improving efficiency.

Digital Governance – GSTN ensured transparency, compliance, and reduced evasion.

GST Reflecting the Accommodative Spirit of Federalism

Institutionalised Cooperative Federalism – The GST Council (Art. 279A) is a federal forum of Union and State Finance Ministers deciding by consensus (3/4th majority).

Pooled Sovereignty – Both Union and States share taxing powers under Article 246A, representing co-ownership of fiscal authority.

Balanced Federal Approach – Dual GST (CGST + SGST) integrates economies while maintaining State autonomy.

Fiscal Balance – Provided States 5-year compensation for revenue loss, cushioning transition.

Special Provisions – Petroleum, alcohol, electricity kept outside GST, respecting States’ revenue needs.

Challenges

Complex multi-tier rate structure increases compliance burden.

Frequent rate revisions affect business stability.

GST Council decided to do away with the compensation cess

Revenue shortfalls weaken State finances.

Centre’s Dominance – Weighted voting gives Centre 33%.

Way Forward

Revive National Anti-Profiteering Authority to ensure rate cuts are passed on to customers

Periodic technological upgrades in GSTN.

Strengthen dispute resolution mechanism within GST Council.

As the Supreme Court (Mohit Minerals, 2022) clarified, GST Council recommendations are not binding, reaffirming that India’s federalism is based on cooperation, not coercion.