Why in the news?

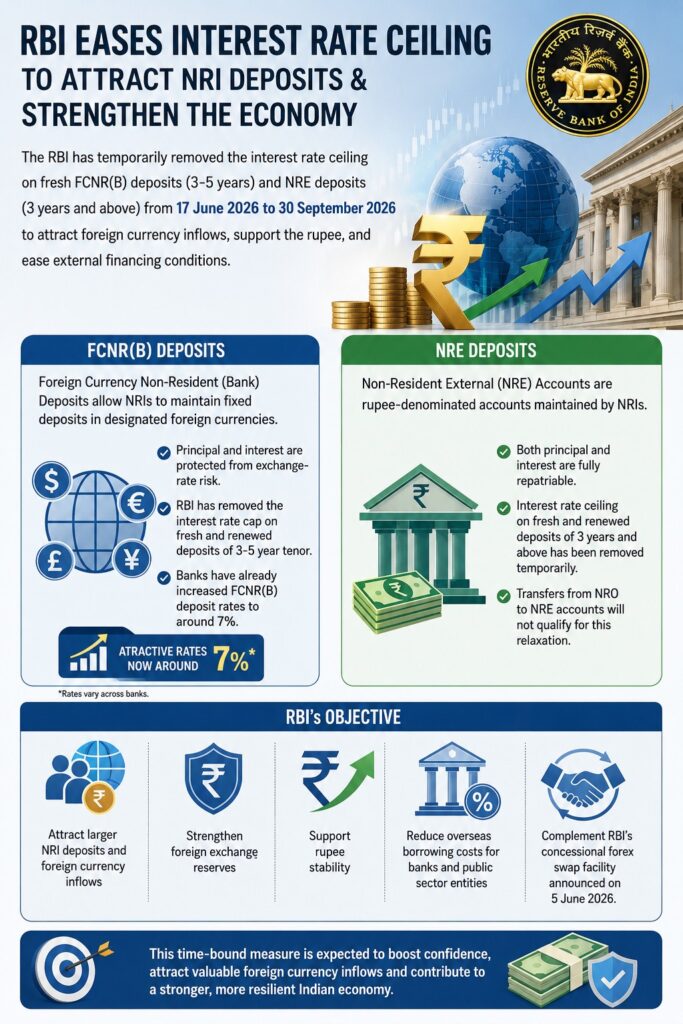

The RBI has temporarily removed the interest rate ceiling on fresh FCNR(B) deposits (3-5 years) and NRE deposits (3 years and above) from 17 June 2026 to 30 September 2026 to attract foreign currency inflows, support the rupee, and ease external financing conditions.

FCNR(B) Deposits

- Foreign Currency Non-Resident (Bank) Deposits allow NRIs to maintain fixed deposits in designated foreign currencies.

- Principal and interest are protected from exchange-rate risk.

- RBI has removed the interest rate cap on fresh and renewed deposits of 3-5 year tenor.

- Banks have already increased FCNR(B) deposit rates to around 7%.

NRE Deposits

- Non-Resident External (NRE) Accounts are rupee-denominated accounts maintained by NRIs.

- Both principal and interest are fully repatriable.

- Interest rate ceiling on fresh and renewed deposits of 3 years and above has been removed temporarily.

- Transfers from NRO to NRE accounts will not qualify for this relaxation.

RBI’s Objective

- Attract larger NRI deposits and foreign currency inflows.

- Strengthen foreign exchange reserves.

- Support rupee stability.

- Reduce overseas borrowing costs for banks and public sector entities.

- Complement RBI’s concessional forex swap facility announced on 5 June 2026.

Expected Impact

- Analysts estimate $30-50 billion of inflows by Q3 FY27.

- Similar FCNR(B) scheme in 2013 attracted nearly $25 billion.

- Increased foreign currency liquidity may ease external sector pressures.

[2021] Consider the following:

1. Foreign currency convertible bonds

2. Foreign institutional investment with certain conditions

3. Global depository receipts

4. Non-resident external deposits

Which of the above can be included in Foreign Direct Investments?

[A] 1, 2 and 3

[B] 3 only

[C] 2 and 4

[D] 1 and 4