The Goods and Services Tax (GST), implemented on 1 July 2017, unified India’s fragmented indirect tax system into a single, destination-based tax, aimed at creating a ‘one nation, one tax’ System.

Indirect Taxes Subsumed under GST

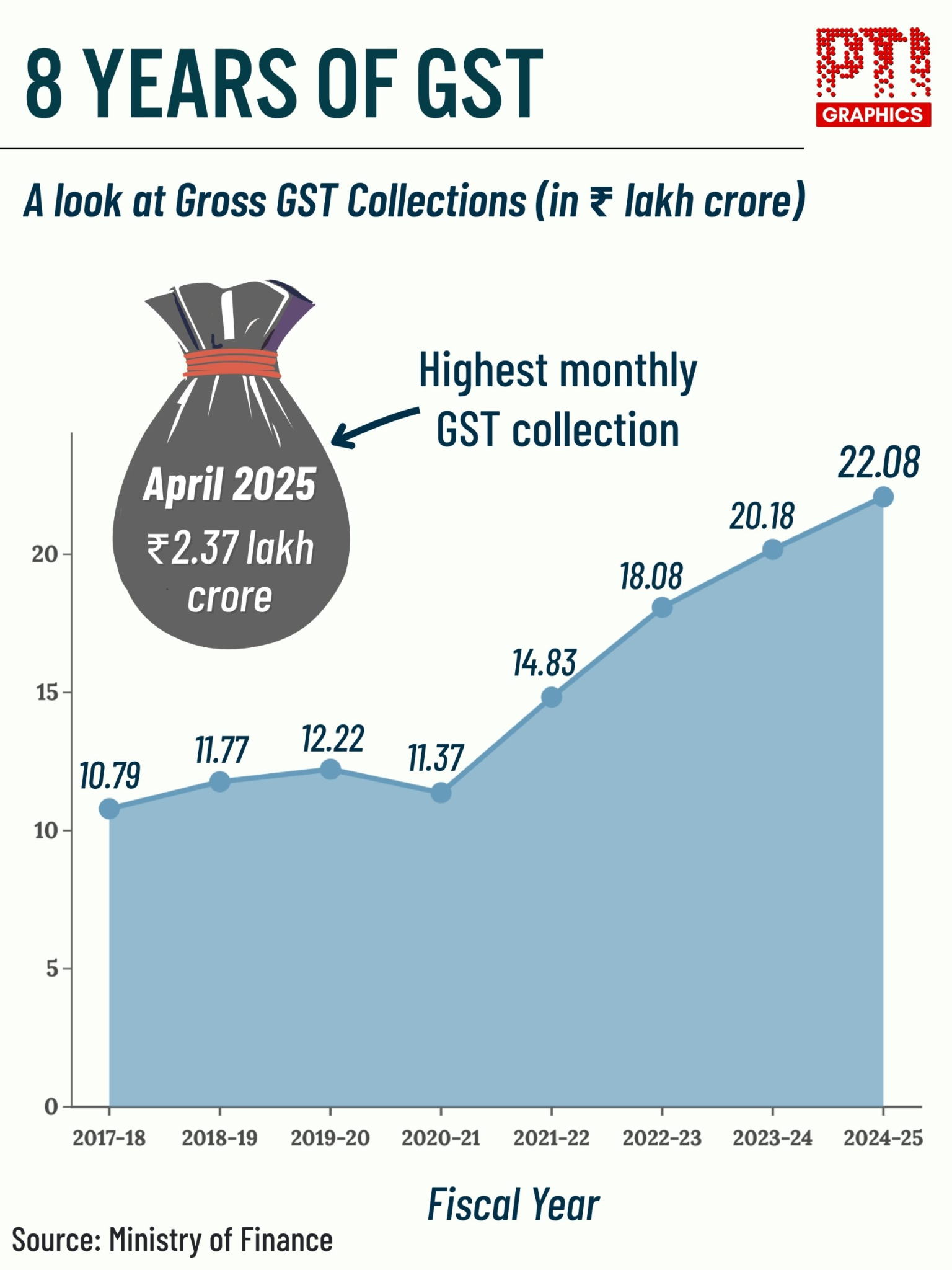

Revenue Implications of GST Since July 2017

Rising Revenue Collections – Eg – Average monthly collections rose from to .

Formalisation – E-invoicing, ITC matching and GSTN integration improved compliance, pushing MSMEs into the formal economy

Reduction in Cascading – Unified tax with seamless input credit reduced the tax-on-tax effect, improving supply-chain efficiency and indirectly boosting revenues.

Support for Manufacturing: Correcting inverted duty structures enhances domestic value addition, strengthens export competitiveness, and boosts revenue.

Ease of Compliance – lower rates under GST 2.0 combined with better compliance can increase GST collections in the medium term.

Challenges

Post GST 2.0 revenue shortfall of . Due to reduced rates and zero-rating of many goods.

PRS Report– the aggregate revenue under GST has declined from 6.5% of GDP in 2015-16 to 5.5% of GDP in 2023-24. (below the 7% GST-to-GDP ratio projected by the 15th FC)

Initial Revenue Volatility – States faced shortfalls despite compensation, indicating

High Compliance Burden – Multiple monthly, quarterly, and annual returns, e-invoicing, and ITC reconciliation increase administrative load, especially for SMEs.

State Revenue Concerns – Dependence on compensation cess and delays in payments strain state finances

Evasion and fraud through fraudulent activities like fake invoices persist.

Nearly half of the economy remains outside the GST framework. Eg- petroleum products, real estate, and electricity duties are excluded from GST.

For higher, predictable and efficient revenue generation, the need is to

Include petroleum and electricity under the GST

Anti-Evasion Measures: Eg- Utilizing advanced data analytics

Bring emerging sectors- crypto-assets, carbon credits under GST