Fiscal federalism refers to the financial relations between centre and states, covering the division of taxation powers, expenditure responsibilities, and transfer mechanisms. Article 268 – 293 deal with Fiscal Federalism in India.

Evolving Pattern of Centre-State Financial Relations in Planned Development

1950-1990- Centralised Planning Era

The Planning Commission controlled transfers through discretionary plan grants.

The Finance Commission played a limited role in fiscal transfers.

The Centre shaped State priorities through proliferation of CSS.

1991-2014- Reform & Decentralisation Phase

Economic liberalisation gave States more fiscal autonomy in revenue and expenditure.

Introduction of VAT (2005) boosted State revenues through a buoyant tax base.

CSS were rationalised but tied funds still constrained State flexibility.

2015 onwards- New Federalism Phase

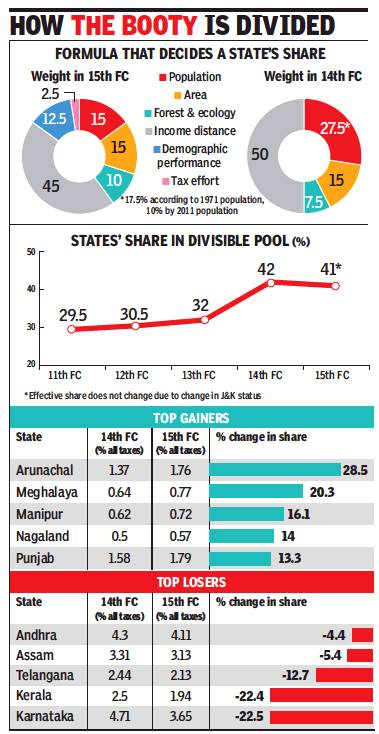

The 14th Finance Commission raised devolution to 42%, enhancing fiscal space for States.

NITI Aayog replaced the Planning Commission and adopted a consultative approach.

GST (2017) introduced pooled sovereignty and created a shared tax regime.

The 15th Finance Commission continued 41% devolution but increased performance-linked grants.

Impact of Recent Reforms on Fiscal Federalism

Positive Impacts

Institutionalised Cooperative Federalism – GST Council as joint decision-making forum.

Economic Efficiency – GST reduced cascading taxes, transport time cut by 33%, tax base expanded from 66 lakh (2017) to 1.5 crore+ (2024), collections near .

Strengthened Development Role – States’ developmental expenditure rose from 8.8% of GDP (2004-05) to 12.5% (2021-22).

Negative Impacts

The Centre retains major taxation powers (income tax, CGST, natural resources), while States restricted to SGST.

Cesses & surcharges grew, shrinking States’ effective share from 35% (2015-20) to ~31% (2020-24).

Delayed GST compensation, especially during COVID, undermined States’ trust.

Borrowing capped at 3% of GSDP, with enhanced limits tied to reform conditions (e.g., power sector).

The 15th FC’s 45% income distance weight penalised better-performing States (TN, Kerala, Karnataka).

Grants-in-aid declined from to , reducing States’ fiscal flexibility.

CSS burden increased as States finance a larger share but have little role in design.

Way Forward

Equity in devolution – Use HDI as a parameter in horizontal tax distribution.

Off-budget borrowings – Scrutinise and report to ensure transparency and accountability.

Horizontal imbalance – Guarantee minimum share for rich States and set a ceiling for poorer States.

Increase Devolution to 50% under 16th FC.

Include Cess/Surcharge in divisible pool

Restructure CSS – Consolidate into fewer umbrella schemes

For India’s fiscal federalism to be effective, it must rest on the principles of autonomy, adequacy, and elasticity.