India’s food processing sector is projected to grow from $307 billion (2023) to $700 billion by 2030, driven by rising demand, technological change, and strong policy support.

Scope of the Food Processing Industry in India

Large agricultural base

Second-largest producer of fruits and vegetables.

Wide product spectrum – Includes dairy, fruits & vegetables, meat, fisheries, beverages, ready-to-eat (RTE), and organic foods.

Lifestyle Shift – 65% of Indians under 35, rising incomes, urbanization & busy lifestyles have boosted demand for ready-to-eat & processed foods.

Rapid growth in Organised retail and “shopping mall culture”- better supply chain management. Eg- D-mart

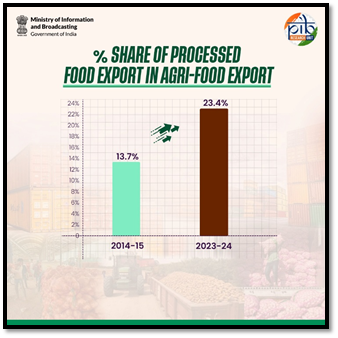

Export potential – India exports processed foods to 200+ countries

Nearly 70% of food processing units operate in the unorganised MSME sector – generate rural employment and entrepreneurship.

Challenges of the Food Processing Sector in India

Low Level of Processing – Only ~10% of total agricultural produce is processed (vs 60-70% in developed countries).

Post-harvest losses of 15-20% due to shortage of cold-storage, and transport infrastructure.

Fragmented Supply Chain – 86% of farmers are small/marginal – limits aggregation

High Logistics Cost of 13-14% of GDP (vs 8-9% in developed countries).

Delay in project implementation – Eg- only 25 out of 42 approved Mega Food Parks operational

Regulatory & Compliance Issues – Complex FSSAI norms and licensing delays discourage small processors.

Low Exports – 16% of India’s agri-exports are processed products, compared to 25% in the US and 49% in China.

Micro and small units struggle to access formal credit, collateral, and working capital.

Skill gap – Only 3% of the food processing workforce is formally trained

Quality & Safety Gaps – Inconsistent adherence to food safety standards, and limited testing infrastructure. Eg- Rejection of Indian exports by EU.

Negligible R&D (<0.5% of sectoral GVA) – stall innovation in packaging and product design

Measures taken by government

The food processing sector has been recognized as a ‘sunrise sector‘ and a key priority industry under the ‘Make in India’ initiative.

PM-Kisan SAMPADA (2016) – Central Sector Scheme to build a modern processing ecosystem from farm-gate to retail.

Mega Food Parks Scheme – Provides land, utilities, common facilities, effluent plants, R&D labs.

PM Formalisation of Micro Food Processing Enterprises (PM-FME) – Provides 40% credit-linked subsidy, branding support, and training for 2 lakh micro units under the One District One Product (ODOP) approach.

Production Linked Incentive Scheme (PLISFPI) to boost domestic manufacturing.

Operation Greens (TOP to TOTAL) – Price stabilization fund for tomato, onion, potato, now expanded to all perishable crops

100% FDI in food processing and 100% FDI under Government route for retail of food produced in India.

e-NAM Integration – Linking mandis for better price discovery, quality grading, and seamless movement of produce.

Food processing included under PSL to improve access to affordable credit.

National Makhana Board to globally position Indian superfoods like makhana.

Infrastructure Status (HLIS) – Food parks are included in Harmonized List of Infrastructure – enables concessional loans.

Collaboration with Invest India for FDI facilitation, market access, regulatory assistance.

As India moves forward under the Make in India vision, the food processing industry will continue to be a key driver of economic growth, ensuring food security, quality, and global competitiveness.