As per Granville Austin, India is a “cooperative federalism” model, where Centre and States are bound in a “seamless web” to achieve socio-economic revolution. The recent changes highlight the spirit of ‘competitive-cooperative federalism’.

Recent Changes in Centre-State Relations

Legislative

Farm Acts, 2020 – Parliament legislated in agriculture (State subject) under Concurrent List.

GNCTD (Amendment) Act, 2021 – Enhanced LG’s powers in Delhi.

All India Services rules amendment – Greater Centre control over deputation/discipline.

Executive / Institutional

Governor-State tensions – Delayed assent to bills (TN, Kerala, WB).

Pandemic handling – Centralised lockdown and restrictions.

Revival of Inter-State Council

NITI Aayog – Replaced Planning Commission

Financial

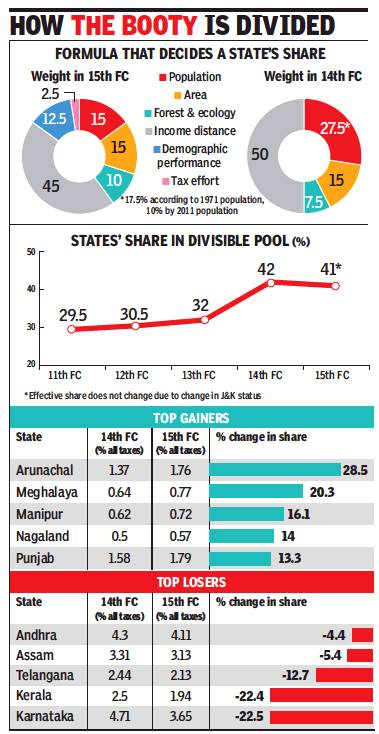

15th Finance Commission – New devolution formula using 2011 census and performance criteria.

GST Council – Extended GST compensation cess.

Rise in cess & surcharges – increased from 10.4% in 2011-12 to 20% in 2021-22.

Conditional borrowing – Linked to reforms under FRBM/Art. 293.

Issues in Centre-State Relations

Financial Issues

Cesses & surcharges not shared with States.

Special category status demand – Bihar, Andhra Pradesh.

Finance Commission TOR – (e.g., use of 2011 Census penalising southern States).

GST regime – Delayed compensation, reduced fiscal autonomy.

Administrative Issues

Governor’s appointment & dismissal (Art. 156) – Often politically motivated

Control over All India Services

Central agencies’ overreach – CBI, ED, NIA operating in States without consent.

Legislative Issues

Encroachment on State List – use of Epidemic Diseases Act, 1897 and Disaster Management Act, 2005 in public health (a State subject).

Measures to Build Trust & Strengthen Federalism

Sarkaria Commission (1983-88)

Inter-State Council (Art. 263) to be activated as a permanent forum for consultation.

Governor’s role – should be impartial; appointment in consultation with CM.

Centre’s use of Art. 356 – to be a measure of last resort.

All India Services – joint consultation in rules of recruitment, posting, and deputation.

Punchhi Commission (2007-10)

Clear guidelines for Governor’s office – fixed tenure, limited discretion, no arbitrary withholding of assent to bills.

Concurrent List – reduce overlap by greater consultation before Union laws are enacted.

National Commission to Review the Working of the Constitution (NCRWC, 2000)

Decentralisation – strengthen local bodies and fiscal devolution.

Inter-Governmental Forums – regular meetings between PM and CMs to resolve disputes.

Second Administrative Reforms Commission (2nd ARC, 2005-09)

Neutral federal institutions – e.g., CBI under Lokpal for credibility, not political misuse.

Fiscal federalism – ensure predictability in devolution; reduce tied grants in Centrally Sponsored Schemes.

Finance Commission Recommendations

Suggested GST Council as a true federal forum for resolving fiscal disputes.

“Federalism is not a monolith; it is a dialogue between self-rule and shared rule.” Thus, such Acts must be exercised with consultation and cooperation.