India has cut import duty on crude palm oil (CPO) and refined, bleached and deodorized (RBD) palm oil, and also moved RBD oil from the “free” to the “restricted” list of imports.

A move against outspoken Malaysia

- Curbing palm oil imports has been construed as retaliation against Malaysia’s PM Mahathir Mohamad, who has criticised India’s internal policy decisions such as the revocation of the special status for J&K and CAA.

- Malaysia has also been sheltering since 2017 the Islamic preacher Zakir Naik who is wanted by India on charges of money laundering, hate speech, and links to terror.

Has India banned import of Malaysian palm oil because of political reasons?

- Not really. The import of RBD palm oil has been restricted, not banned — and this is from all countries, not just Malaysia. Also, CPO can still be imported freely.

- Under the trade classification system that India follows, except for goods that can be imported only by state trading enterprises all goods whose import is not restricted or prohibited are traded freely.

- Normally, a special licence is required to import a restricted good. The government has neither specified what the restrictions entail nor issued any licences.

- However, it has been reported that vessels carrying RBD palm oil are stuck at several ports because buyers have been asked to shun the product.

How much palm oil does India import?

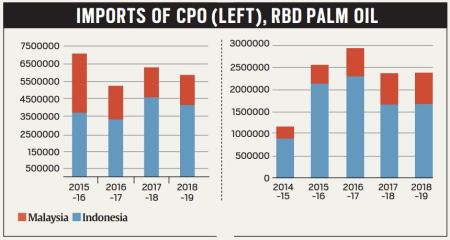

- India imported 64.15 lakh metric tonnes (MT) of CPO and 23.9 lakh MT of RBD in 2018-19, the bulk of which was from Indonesia.

- India imported $10 billion worth of vegetable oil in 2019-20, making it the country’s fifth most valuable import after mineral oil ($141 bn), gold ($32 bn), coal ($26 bn), and telecom instruments such as cell phones ($17 bn).

Why does India need so much palm oil?

- It is the cheapest edible oil available naturally.

- Its inert taste makes it suitable for use in foods ranging from baked goods to fried snacks.

- It stays relatively stable at high temperatures, and is therefore suitable for reuse and deep frying. It is the main ingredient in vanaspati (hydrogenated vegetable oil).

- However, palm oil is not used in Indian homes.

- That, and the fact that CPO continues to be imported, makes it unlikely that the decision to restrict refined palm oil imports will impact food inflation immediately.

Who will be impacted by the decision?

- Indonesia and Malaysia together produce 85% of the world’s palm oil, and India is among the biggest buyers.

- Both Indonesia and Malaysia produce refined palm oil; however, Malaysia’s refining capacity equals its production capacity — this is why Malaysia is keen on exporting refined oil.

- Indonesia, on the other hand, can supply CPO, which would allow India to utilise its full refining capacity.

Why import Crude Palm Oil?

- The CPO that India imports contains fatty acids, gums and wax-like substances. Refining neutralises the acids and filters out the other substances.

- The filtrate is bleached so that the oil does not change colour after repeated use. Substances that may cause the oil to smell are removed physically or chemically.

- This entire process increases the value of a barrel of crude oil by about 4%.

- Additionally, there are costs to transporting the crude, which makes it more cost-effective to import the refined oil.

- But the refining industry has been demanding that the import duty on refined oil be increased, which would make importing crude oil cheaper than importing refined oil.

- The decision to restrict imports of refined oil will benefit refiners, which include big-ticket names like the Adani Wilmar group.

Will restricting imports of RBD palm oil help farmers?

- Restricting refined oil imports will not help farmers directly, as they are not involved in the process of refining.

- However, the restrictions have caused refined palm oil prices to increase. If prices continue to hold, farmers will get a better realization for their crop.

- But the timeframe over which the changes in import policy will have an effect on domestic crop realization is fairly long, given that palm trees take over four years to provide a yield.

- Also, if the demand is met entirely by importing and refining CPO, farmers will be left out of the picture.

How will Malaysia be affected?

- Malaysia has said that it cannot retaliate against India because it is “too small”.

- With imports to its largest market restricted (India bought over 23% of all CPO produced by Malaysia in 2019), Malaysian palm oil futures fell by almost 10% in January, although it has recovered since then.

- India and Malaysia signed a free trade agreement — Malaysia-India Comprehensive Economic Cooperation Agreement — in February 2011.

- In 2018, Malaysia exported 25.8% of its palm oil to India.

- If India does not issue licenses for importing refined oil, Malaysia will have to find new buyers for its product.