| PYQ Relevance: Prelims: The Government of India has established NITI Aayog to replace the [UPSC CSE 2015] a) Human Rights Commission b) Finance Commission c) Law Commission d) Planning Commission Mains: 1. How have the recommendations of the 14th Finance Commission of India enabled the States to improve their fiscal position? [UPSC CSE 2021] 2. How is the Finance Commission of India constituted? What do you know about the terms of reference of the recently constituted Finance Commission? Discuss. [UPSC CSE 2018] 3. Though the federal principle is dominant in our Constitution and that principle is one of its basic features, it is equally true that federalism under the Indian Constitution leans in favor of a strong Centre, a feature that militates against the concept of strong federalism. [UPSC CSE 2014] |

Note4Students:

Mains: Finance Commission; Centre-State relations;

Prelims: Recommendations by Finance Commission;

Mentor comments: The issue of declining shares of some States in central transfers, is particularly affecting southern States like Karnataka and Tamil Nadu, stems from factors like the income distance criterion and changes in population data used for calculations. The income distance criterion, which rewards states further from the highest income state, has led to losses for southern States. To address this issue, we need to reduce the weight of the income distance criterion and limiting cesses and surcharges of the Centre’s gross tax revenues. Overall, today’s debate is over central transfers who need to have a balanced approach that considers various criteria like income distance and population while ensuring equitable distribution among all states.

Let’s learn.

—

Why in the News?

The Southern States have been facing a decline in their share out of the resources transferred from the Centre to the States. Considering this situation, there are many issues that the Sixteenth Finance Commission will have to deal with.

Background:

- The revenue sharing through the Finance Commission between Centre and the Southern States has fallen over the last two decades.

- The share of states in combined revenue receipts rose but has since fallen, highlighting the need for fair distribution mechanisms.

- Additionally, the shift in population data from 1971 to 2011 has impacted tax devolution, with some southern states feeling disadvantaged.

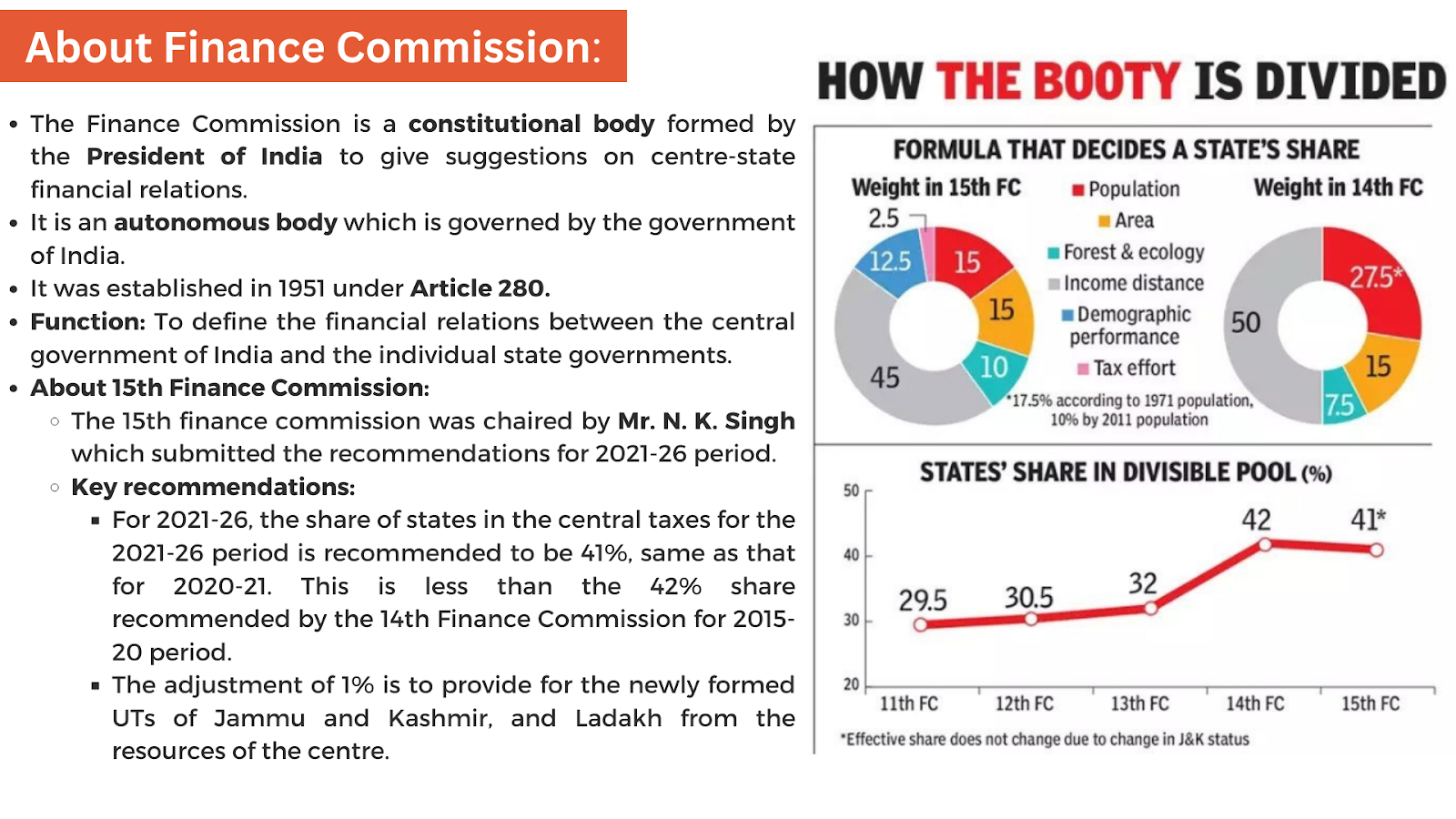

| What is the income distance criterion and how does it affect state shares? The income distance criterion in the context of Finance Commission allocations is a measure of the distance between a state’s income and the state with the highest income, calculated based on the average per capita Gross State Domestic Product (GSDP). States with lower per capita income receive a higher share to ensure equity among states. Significance of this criteria: It remains crucial for ensuring fair distribution among states. It also plays a significant role in determining the distribution of union taxes to each state, with states further from the highest income state receiving a higher share. |

What are the 3 major challenging observations in Centre-State Tax Devolution?

1) Issue of share with states in Tax Devolution:

- Firstly, we need to look at which States have been gaining and which are losing their share over time; the criteria of horizontal distribution which has led to some States steadily losing their share; and what can be done to reverse this trend.

- In Table 1, the shares of groups of States and those for selected States are shown, for the 12th FC to the 15th FC (final report).

- Southern States have been on a steady fall in their share, from 19.785% to 15.800%. The northern and eastern States have also lost. The ‘gainer States’ were the hilly, central, and western States including Maharashtra.

- The low-income States such as Bihar and Uttar Pradesh show, in terms of their overall share, a loss of 0.970% points and 1.325% points.

- The main reason for the loss to the southern States due to the distance criterion amounted to 8.055% points, although the overall loss was much less at 3.985% points, implying that there was a gain under other criteria.

2) Issue over the Income Distance:

- Inconsistency: Table 2 provides a list of the different criteria used by Finance Commissions, from the Twelfth to the Fifteenth.

- Decreasing weight: The distance criterion has been accorded the highest weight amongst these criteria. Its weight was reduced from 50% to 47.5% by the 13th FC and further reduced to 45% by the 15th Fifteenth FC.

- Hampering equalization: The above two observations challenge the Socio-economic justice principles which has always been regarded as a key principle in governing distribution.

3) Issue over the Population:

- Data Updation issue: Until the Fourteenth Finance Commission, the data for the population in 1971 was used. For the Fifteenth Finance Commission, data for the population in 2011 was used.

- Mismatched data: In order not to penalize States 15th FC showed better performance in reducing fertility rates, and the demographic change criterion was eventually introduced.

- The joint impact of these two changes has been marginal for all groups of States. For Tamil Nadu, the joint impact was marginally positive.

| Recommendation for Sixteenth Finance Commission: Balanced allocation approach: Need to consider reducing the weight of the income distance criterion by 5% to 10% points. On Cesses and Surcharges: Need to evaluate and potentially impose an upper limit on cesses and surcharges to safeguard the divisible pool size and states’ revenue shares. |

What steps need to be taken? (Way Forward)

- Maintain Income Distance Criterion: The income distance criterion is essential for equitable distribution among states and should not be abandoned. We need to consider reducing its weightage while enhancing other criteria to balance allocations.

- Manage Divisible Pool Size: We need to limit cesses and surcharges to 10% of the Centre’s gross tax revenues to prevent reducing the size of the divisible pool. The increase in states’ share from 32% to 42% by the Fourteenth Finance Commission should not be offset by additional levies.

- Review Revenue Sharing Trends: Need to analyze the impact of changing criteria on state shares over time to ensure fair and balanced distribution. Further, we also need to address concerns raised by states experiencing declining shares due to existing allocation mechanisms.

https://prsindia.org/theprsblog/central-transfers-to-states-role-of-the-finance-commission