Bengaluru-based Astrobase Space Technologies unveiled EVEREST, India’s first privately built 800 kN Full-Flow Staged Combustion (FFSC) LOX-Methane engine on 7 August 2026. India is now the fourth country after Russia, the US and China with FFSC technology.

What is an FFSC Engine?

About: An advanced liquid rocket engine architecture offering high thrust and efficiency.

Full-flow: Fuel and oxidiser pass through separate pre-burners, driving turbopumps before entering the main chamber.

Advantage: Almost all propellant contributes to thrust, improving efficiency and reusability.

What is LOX-Methane?

LOX: Liquid Oxygen as oxidiser.

Methane: Fuel that burns relatively cleanly, reducing engine deposits and aiding faster refurbishment and turnaround.

What is IN-SPACe?

Indian National Space Promotion and Authorisation Centre, an autonomous agency under the Department of Space.

Acts as a single-window agency to promote and authorise private space activities.

Astrobase received support through its Technology Adoption Fund.

Why is EVEREST Significant?

Technology: Makes India the 4th FFSC-capable nation.

Reusability: Suitable for reusable launch vehicles with precise throttle control.

Capacity: Could enable reusable systems carrying up to 30 tonnes to LEO.

Manufacturing: Uses advanced manufacturing, including large-scale 3D printing.

Timeline: Development began in 2024; integrated hot-fire tests are planned at Anantapur, with first flight targeted for December 2028.

Global Comparison

Russia: Pioneer in FFSC technology.

USA: SpaceX’s Raptor is the only operational FFSC engine.

China: LandSpace has developed a commercial high-thrust FFSC engine.

India: EVEREST marks its entry into FFSC technology.

Private Space Sector in India

2020 reforms: Opened space activities to private players through IN-SPACe.

Indian Space Policy 2023: Enables greater private participation across the space value chain.

NSIL: Commercial arm of the Department of Space.

Firms such as Skyroot Aerospace and Agnikul Cosmos are developing indigenous launch technologies.

“[2026] Consider the following statements about involvement of private entities in India’s space programme:

1. IN-SPACe is an autonomous agency formed to facilitate participation of private entities.

2. Agnikul Cosmos launched the world’s first flight using 3D-printed rocket engine.

3. Skyroot Aerospace has developed liquid fuel for GSLV.

India’s ethanol blending has reached 20%, ahead of the 2030 target. It has displaced 310 lakh tonnes of imported crude, saved over ₹1.90 lakh crore in foreign exchange and transferred over ₹1.6 lakh crore to farmers.

What is the Ethanol Blended Petrol (EBP) Programme?

EBP: Ethanol Blended Petrol Programme blends ethanol, mainly produced from sugarcane and grains, with petrol.

E20: 20% ethanol blending has been achieved ahead of schedule.

Benefits: Reduces crude imports, supports farmers and lowers emissions.

What are Strategic Petroleum Reserves (SPR)?

SPR: Strategic Petroleum Reserves are underground crude oil storage facilities used as an insurance against supply disruptions.

They provide a temporary buffer and must eventually be replenished.

What has Ethanol Blending Achieved?

20% blending achieved.

310 lakh tonnes of crude imports displaced.

₹1.90 lakh crore+ foreign exchange saved.

₹1.6 lakh crore+ transferred to farmers.

930 lakh tonnes+ CO₂ emissions avoided.

Why Both Public and Private Players?

ONGC: Oil and Natural Gas Corporation, a major state-owned upstream producer.

OIL: Oil India Limited, another major state-owned upstream producer.

Public sector: Provides strategic control and supports national energy security.

Private sector: Brings capital, technology and efficiency into exploration, production and storage.

Balanced approach: India needs both strategic public capacity and competitive private participation.

How Do Reserves and Domestic Production Complement Each Other?

SPR: Protects against sudden supply shocks.

Domestic production: Reduces imports over the life of an oil field.

Overseas stocks: Long-term suppliers could maintain crude stocks earmarked for India.

Exploration: Opening more offshore areas can expand domestic resources.

Energy Security in India

Energy security means reliable and affordable energy supply with resilience against disruptions.

Four pillars:

Domestic production

Strategic reserves

Import diversification

Alternative fuels

India’s high crude import dependence exposes it to global price shocks and disruptions in chokepoints such as the Strait of Hormuz and Bab el-Mandeb.

SATAT: Sustainable Alternative Towards Affordable Transportation, promoting compressed biogas.

SPR Programme: Strategic Petroleum Reserves Programme for crude oil security.

[2025] Consider the following statements:

Statement I: Of the two major ethanol producers in the world, i.e., Brazil and the United States of America, the former produces more ethanol than the latter.

Statement II: Unlike in the United States of America, where corn is the principal feedstock for ethanol production, sugarcane is the principal feedstock for ethanol production in Brazil.

Which one of the following is correct in respect of the above statements?

(a) Both Statement I and Statement II are correct and Statement II is the correct explanation for Statement I

(b) Both Statement I and Statement II are correct and Statement II is not the correct explanation for Statement I

(c) Statement I is correct but Statement II is incorrect

(d) Statement I is incorrect but Statement II is correct

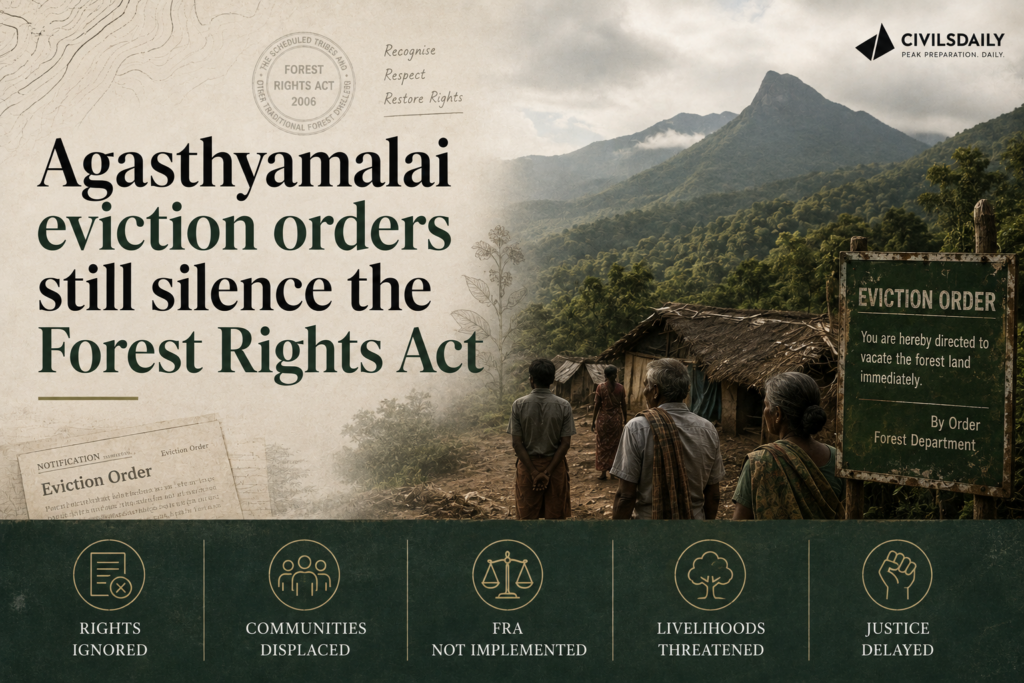

The Forest Department has issued eviction notices to thousands of households in the Agasthyamalai Biosphere Reserve (ABR) following a Supreme Court order for time-bound removal of forest encroachments. The issue highlights the tension between forest conservation and rights under the Forest Rights Act, 2006.

What is the Forest Rights Act, 2006?

Full name: Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006.

Recognises forest rights of Scheduled Tribes (STs) and other traditional forest dwellers.

Cut-off: Eligible occupation must pre-date 13 December 2005.

Claims are initiated and verified by Gram Sabhas and examined by higher-level committees.

Key safeguard: Eviction cannot take place until recognition and verification are completed.

What is the Agasthyamalai Biosphere Reserve?

ABR: Agasthyamalai Biosphere Reserve.

Covers about 3,500 sq km across Tamil Nadu and Kerala.

Includes Kalakkad-Mundanthurai, Srivilliputhur-Megamalai and Periyar Tiger Reserves, along with wildlife sanctuaries.

What is the Central Empowered Committee?

CEC: Central Empowered Committee.

Constituted under Supreme Court directions to monitor forest and environmental compliance.

It surveyed the Agasthyamalai landscape and reported violations involving non-forestry activities.

Who are Other Traditional Forest Dwellers?

OTFDs: Other Traditional Forest Dwellers.

Non-tribal communities primarily dependent on forests for livelihood.

They must demonstrate three generations or 75 years of dependence before 13 December 2005.

What did the Supreme Court order?

Time-bound eviction plan, with rehabilitation where applicable.

Legal action against wilful violators, including 118 government servants found to be encroachers.

Ecological restoration after eviction.

No new forest diversion or non-forest activity in ABR until encroachments are removed.

Possible deployment of paramilitary forces for enforcement.

Key Issue: Conservation vs Forest Rights

Conservation: Evictions aim to restore critical tiger habitat and remove non-forest activities.

Rights concern: Eviction before completion of FRA recognition and verification can violate statutory safeguards.

Data problem: Lack of reliable data on occupation outside FRA’s scope makes it difficult to distinguish genuine rights-holders from actual encroachers.

WLPA, 1972: Wild Life (Protection) Act, 1972, governs protected areas.

PESA, 1996: Panchayats (Extension to Scheduled Areas) Act, 1996, strengthens Gram Sabha powers in Scheduled Areas.

SC/ST PoA Act, 1989: Scheduled Castes and Scheduled Tribes (Prevention of Atrocities) Act, 1989.

Back2Basics: Forest Rights Act

Nodal Ministry: Ministry of Tribal Affairs.

Beneficiaries: Forest-dwelling STs and eligible OTFDs.

Three rights: Individual forest rights, community rights and Community Forest Resource (CFR) rights.

Gram Sabha: Starting point for claims.

Key safeguard: No eviction before completion of recognition and verification.

“[2021] At the national level, which ministry is the nodal agency to ensure effective implementation of the Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006?

(a) Ministry of Environment, Forest and Climate Change

India’s Asiatic lion population increased from 523 in 2015 to 891 in 2025, the highest recorded count. Project Lion, launched in 2020, aims to strengthen conservation of the species and its Gir landscape.

What is Project Lion?

Launched: 2020 for long-term conservation of the Asiatic lion.

Focus: Habitat improvement, disease surveillance, scientific monitoring and community participation.

Tools: Radio-collaring, camera traps and genetic/gene-pool conservation.

Need: The entire wild population is concentrated in one landscape, creating a major single-population risk.

Latest Population Status

2015: 523 lions

2025: 891 lions

Key concern: Many lions now occur outside protected areas, increasing human-wildlife conflict.

Habitat: Gir is approaching its carrying capacity, strengthening the case for a second home.

Back2Basics: Asiatic Lion

Scientific name:Panthera leo persica

IUCN: Endangered

CITES: Appendix I

Wild Life (Protection) Act, 1972: Schedule I

Only wild population: India

Natural range: Gir landscape, Gujarat

Proposed second home:Barda Wildlife Sanctuary, Porbandar.

Why is a Second Home Needed?

Single-site risk: Disease or disaster in Gir could threaten the entire species.

Habitat saturation: Increasing population is pushing lions beyond protected areas.

Human-wildlife conflict: Greater interaction with people and livestock.

Disease risk: Outbreaks such as Canine Distemper Virus (CDV) can threaten large carnivores.

Habitat fragmentation: Mining, roads and railways can disrupt dispersal corridors.

Statutory Framework

WLPA, 1972: Wild Life (Protection) Act, 1972, provides legal protection to wildlife.

For the first time in 50 years, a Director General of Police set foot on the Telangana side of Karregutta, a hill once used to house Central Committee members of the banned Communist Party of India (Maoist). The visit marks the decline of Left Wing Extremism under Operation Kagar, with around 700 surrenders in Telangana and the top leadership largely killed, arrested, or surrendered.

What is Operation Kagar?

Definition:Operation Kagar is a coordinated anti-Maoist offensive launched by security forces in pursuit of the central government’s deadline for a Naxal-free India.

Scope: It combines intensified security operations with surrender-and-rehabilitation measures across the Maoist-affected belt.

Who are the CPI (Maoist)?

Definition: The Communist Party of India (Maoist), or CPI (Maoist), is a banned Left Wing Extremist organisation that seeks to overthrow the state through armed struggle.

Leadership: Its former General Secretary Muppala Lakshmana Rao, alias Ganapati, was the longest-serving general secretary of the outfit.

What happened at Karregutta?

The DGP’s visit: The Telangana Director General of Police entered the Telangana side of Karregutta accompanied by a large contingent of police and revenue personnel.

The message: The delegation’s size was meant to signal that it is now safe to visit the area, where earlier only specialised forces such as Greyhounds and COBRA units operated briefly during operations.

Tricolour hoisted: The contingent hoisted the national flag at the spot.

Tourism plan: The DGP announced the kaccha road into the forest would be tarred and the area developed into a tourist spot.

Surrender support: Surrendered Maoists are given a lump-sum grant, including the bounty announced on their heads, to start a new life.

What is the current status of the Maoist decline?

Surrenders: Around 700 Maoists surrendered in Telangana alone during the operation.

Leadership losses: By March 31, several Central Committee members of the CPI (Maoist) were killed, arrested, or had surrendered.

Top commander killed: Former General Secretary Nambala Keshava Rao, alias Basavaraju, was killed in a police encounter in May 2025.

Factional split: After Basavaraju’s death the party split into two factions, one led by Mallojula Venugopal Rao, alias Sonu, and another by Thippiri Tirupathi, alias Devuji, who later surrendered.

Few absconding: Only two to three top Maoists remain absconding, chief among them Ganapati.

Conclusion

A DGP entering Karregutta after five decades, followed by the hoisting of the Tricolour, signals the sharp decline of the Maoist movement in Telangana under Operation Kagar. With around 700 surrenders, the top leadership neutralised, and only a handful absconding, the insurgency’s organisational base has collapsed. The next milestone is the government’s deadline for a Naxal-free India and the rehabilitation of surrendered cadres into mainstream society.

Back2Basics:

Left Wing Extremism in India (Foundational Context)

About: Left Wing Extremism (LWE), also called Naxalism, is an armed insurgency by Maoist groups aiming to capture state power through violence.

Geography: It has historically concentrated in a forested tribal belt across Chhattisgarh, Jharkhand, Odisha, Telangana, and neighbouring States.

Nodal ministry: The Ministry of Home Affairs coordinates the national response through security and development measures.

Communist Party of India (Maoist)

Formation: Formed in 2004 through the merger of the People’s War Group and the Maoist Communist Centre of India.

Status: Designated a terrorist organisation under the Unlawful Activities (Prevention) Act, 1967.

Objective: Seeks to overthrow the Indian state through protracted armed struggle.

Armed wing: Operates the People’s Liberation Guerrilla Army.

Government Initiatives against LWE

SAMADHAN doctrine: An overarching strategy covering smart leadership, aggressive strategy, motivation, actionable intelligence, and technology.

Security Related Expenditure Scheme: Reimburses States for security operations, training, and rehabilitation of surrendered cadres.

Aspirational Districts Programme: Targets development in the most backward districts, many of them LWE-affected.

Road connectivity projects: The Road Requirement Plan and RCPLWE scheme build roads to open up affected areas.

Surrender and Rehabilitation Policy: Provides grants, vocational training, and support to those who lay down arms.

Key Facts about LWE

Shrinking footprint: The number of LWE-affected districts has fallen sharply over the past decade.

Declining violence: Incidents and casualties have dropped substantially with intensified operations.

Elite forces: Greyhounds of Telangana and Andhra Pradesh and the CoBRA units of the CRPF are specialised anti-Maoist forces.

Challenges in Countering LWE

Development deficit: Persistent gaps in roads, health, and education sustain grievances in affected areas.

Difficult terrain: Dense forests and hilly terrain aid guerrilla movement and hamper operations.

Tribal alienation: Displacement and land alienation feed recruitment among tribal populations.

Rehabilitation gaps: Surrendered cadres struggle to find a foothold in mainstream society.

Cross-border and inter-State movement: Cadres exploit State boundaries to evade coordinated action.

Way Forward

Sustained development: Extend roads, connectivity, and public services into cleared areas.

Robust rehabilitation: Ensure surrendered cadres receive grants, skills, and livelihoods.

Protect tribal rights: Implement the Forest Rights Act and Fifth Schedule protections effectively.

Consolidate security gains: Hold cleared areas and prevent the movement’s revival across State borders.

UPSC Relevance

[UPSC 2018] Left Wing Extremism (LWE) is showing a downward trend, but still affects many parts of the country. Briefly explain the Government of India’s approach to counter the challenges posed by LWE.

Linkage: The PYQ examines the Government’s approach to tackling Left Wing Extremism. Operation Kagar demonstrates the security and surrender components of this approach. The article also highlights the need for rehabilitation and development after security gains.

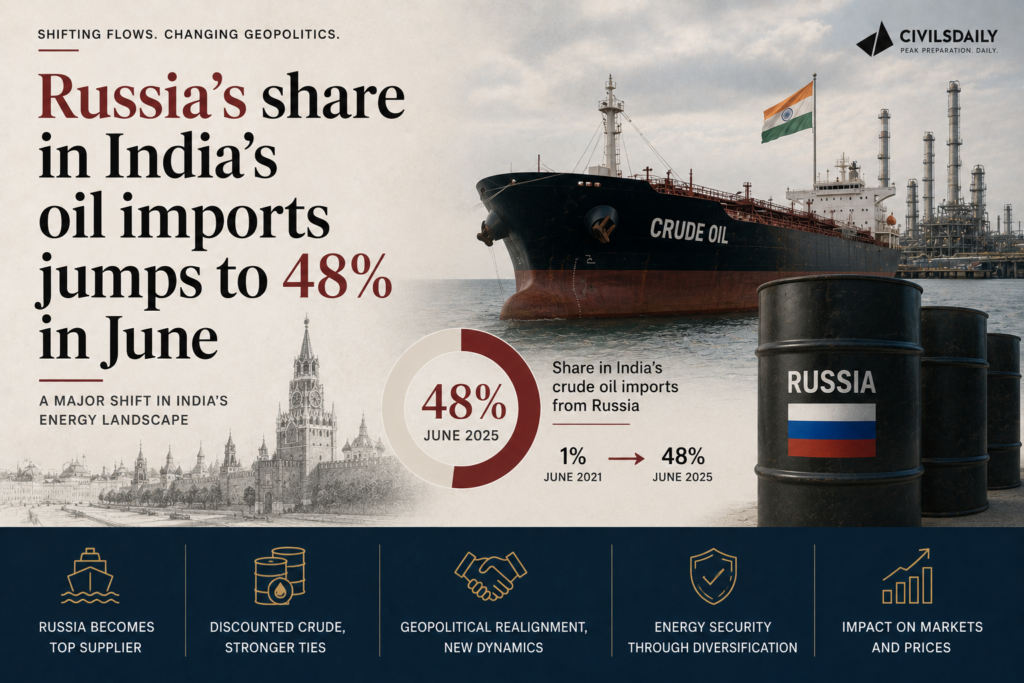

Russia’s share in India’s crude oil imports rose to an all-time high of 48 percent in June 2026, even as India cut its total crude imports. This comes as the US Senate has passed a bill to levy tariffs of up to 100 percent on the top buyers of Russian oil and gas, placing India’s energy security and its trade exposure to the United States in direct tension.

What is the Sanctioning Russia and Iran Act of 2026?

Definition: The Lindsey O. Graham Sanctioning Russia and Iran Act of 2026 is a US bill that authorises secondary tariffs of up to 100 percent on countries that continue to buy Russian oil and gas. It targets the largest purchasers of these products from Russia.

Status: The bill was passed by the US Senate and still requires passage by the US House of Representatives before it becomes law.

What are the tariff triggers under the bill?

Top-buyer test: Tariffs apply to a country that was among the five largest importers of Russian crude oil or natural gas in the 12 months preceding the Act’s enactment.

Continuation test: The tariff applies if that country continues to import Russian oil or gas beyond 30 days after enactment.

Sanctions-evasion clause: Tariffs can also be imposed on countries found to have helped Russia evade sanctions.

India’s exposure: India, alongside China, is one of the top two importers of Russian oil, so it qualifies under these criteria.

What do the June import figures show?

Fall in total imports: June crude oil imports of 18.2 million metric tonnes (MMT) were 16.5 percent lower than in May 2026 and 13 percent lower than in June the previous year.

Import bill still high: The June oil import bill was 22 percent lower than in May but still 40 percent higher than in June last year, due to elevated crude prices.

Russian purchases held up: India imported 8.7 MMT of Russian oil in June, only 1 percent lower than May and 25 percent higher than a year earlier.

Record Russian share: Russia’s share reached 48 percent by quantity and 48.6 percent by value, rising every month since March.

UAE at a high: The United Arab Emirates (UAE) supplied 17.5 percent of imports by volume and 18 percent by value, its highest share so far.

Concentration: Russia and the UAE together accounted for nearly two-thirds of India’s oil imports in June, the highest combined share from any two countries.

Shrinking discount: The premium Russia charged India rose from a discount as recently as February 2026 to a premium of $10.6 per tonne in June, down from $77.7 per tonne in April.

How has India pre-empted sanctions exposure?

Ship-to-ship transfers: The Ministry of Petroleum and Natural Gas said exposure was pre-empted through ship-to-ship transfer operations in international waters via the Red Sea route through Yanbu and Fujairah.

Avoiding a single choke point: The aim was to ensure that no single choke point or sanctions regime could halt India-bound cargo.

Refinery flexibility: Indian refineries spent a decade acquiring the flexibility to switch between crude grades and shipping routes when disruption struck.

Why does the record Russian share expose India?

Energy security dependence: India cannot quickly cut back on Russian oil while supplies through the Strait of Hormuz remain constrained by the West Asia conflict.

Trade and tariff risk: Continued high Russian purchases place India within the top-buyer criteria of the US bill, risking tariffs of up to 100 percent.

Ambiguity on evasion: It is unclear whether India’s ship-to-ship arrangements would be treated as helping Russia evade sanctions.

Conclusion

India’s rising dependence on discounted Russian crude has hit a record 48 percent share, secured through diversified shipping routes even as total imports fell. This leaves India balancing its energy security against the risk of secondary tariffs under the US bill. The immediate milestone is the bill’s fate in the US House of Representatives, which will determine whether the tariff threat becomes law.

Back2Basics:

Strait of Hormuz

Designation: A narrow strait linking the Persian Gulf to the Gulf of Oman and the Arabian Sea.

Bordering states: Bordered by Iran to the north and Oman and the UAE to the south.

Significance: One of the world’s most critical oil transit choke points, carrying a large share of seaborne crude.

What is Energy Security? (Foundational Context)

About: Energy security is the uninterrupted availability of energy sources at an affordable price.

Rationale: It matters because India imports the bulk of its crude oil, leaving growth and prices exposed to external supply shocks.

Core dimensions: It rests on availability, affordability, accessibility, and diversification of both sources and supply routes.

Key Facts about India’s Oil Imports

Import dependence: India imports over 85 percent of its crude oil requirement.

Global standing: India is among the world’s largest crude oil importers and consumers.

Key choke point: The Strait of Hormuz, between the Persian Gulf and the Arabian Sea, carries a large share of India’s West Asian crude.

Challenges to India’s Energy Security

High import dependence: Reliance on imports for most crude exposes the economy to price and supply shocks.

Geopolitical concentration: A large combined share from Russia and the UAE concentrates supply risk in two sources.

Choke-point vulnerability: Disruption at the Strait of Hormuz can constrain West Asian supply.

Sanctions exposure: Purchases from sanctioned suppliers risk secondary tariffs and financial penalties.

Price volatility: War-driven crude price spikes inflate the import bill and widen the current account deficit.

Way Forward

Diversify sources: Expand purchases from a wider set of suppliers to reduce concentration.

Accelerate clean energy: Scale up renewables, biofuels, and electric mobility to cut import dependence over time.

Secure shipping routes: Maintain logistical flexibility across grades and routes to withstand choke-point disruption.

PYQ Relevance

[UPSC 2025] Energy security constitutes the dominant kingpin of India’s foreign policy, and is linked with India’s overarching influence in Middle Eastern countries. How would you integrate energy security with India’s foreign policy trajectories in the coming years?

Linkage: The PYQ examines the integration of India’s energy security with its foreign policy. India’s record 48% dependence on Russian crude highlights the geopolitical dimension of energy security. The article shows the need to diversify suppliers and routes while balancing ties with Russia, the US and West Asia.

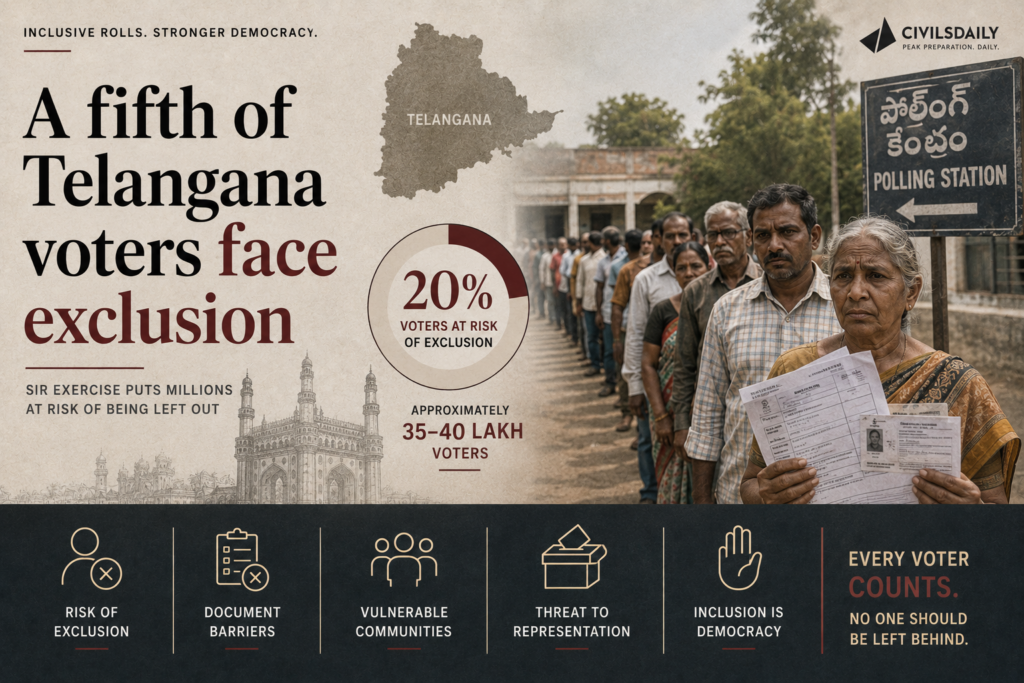

In Telangana, 73.47 lakh enumeration forms, nearly 22% of the electorate, were marked “Uncollectable” during the Special Intensive Revision (SIR) of electoral rolls. The large number raises concerns about balancing clean electoral rolls with the risk of excluding genuine voters.

What is Special Intensive Revision (SIR)?

SIR: Special Intensive Revision of electoral rolls.

Conducted by the Election Commission of India (ECI) through comprehensive, house-to-house enumeration.

Electors submit enumeration forms; non-returned forms may be marked “Uncollectable”.

Doubtful cases may receive notices from Electoral Registration Officers (EROs) for verification.

Current Status in Telangana

Enumeration ended: August 10, 2026.

Uncollectable: 73,47,075 forms, nearly 22% of the electorate.

Draft rolls: Scheduled for August 17.

Claims and objections will follow publication of the draft rolls.

Why is it Concerning?

Disenfranchisement risk: Genuine voters may be deleted along with ineligible entries.

Burden on voters: Migrants, poor households and hard-to-reach groups may struggle to submit forms.

Short timeline: Limited time to reconcile uncollectable forms before draft publication.

Legal concerns: The process has faced challenges regarding deletion procedures.

Safeguards After Draft Roll

Claims and objections: Voters can seek restoration of wrongly deleted names.

ERO verification: Doubtful cases can be examined before finalisation.

Appeals: Aggrieved voters can approach higher electoral authorities and courts.

Constitutional & Legal Framework

Article 324: Gives the Election Commission of India (ECI) superintendence, direction and control over elections and electoral rolls.

Article 325: Provides for one general electoral roll and prohibits exclusion on grounds of religion, race, caste or sex.

Article 326: Provides for adult suffrage.

Representation of the People Act, 1950 (RPA 1950): Governs preparation and revision of electoral rolls.

Registration of Electors Rules, 1960: Provides procedures for claims, objections and revision.

Back2Basics: Election Commission of India

Type: Constitutional body under Article 324.

Established: 1950.

Composition: Chief Election Commissioner and other Election Commissioners.

Mandate: Conducts elections to Parliament, State legislatures, and the offices of President and Vice-President.

Role in rolls: Conducts summary and intensive revisions to maintain accurate electoral rolls.

Challenges

Wrongful deletion of genuine voters.

Exclusion of migrants and seasonal workers.

Duplicate, dead and ineligible entries.

Compressed timelines for verification and objections.

Documentation burden on vulnerable voters.

Loss of public trust due to perceived lack of transparency.

[2017] For election to the Lok Sabha, a nomination paper can be filed by

(a) Anyone residing in India

(b) A resident of the constituency from which the election is to be contested

(c) Any citizen of India whose name appears in the electoral roll of a constituency

The Parliamentary Standing Committee on Social Justice and Empowerment flagged delays in constructing and operationalising Eklavya Model Residential Schools (EMRS). Only 428 of 728 sanctioned schools have been completed, while 118 continue from government or rented buildings.

What is EMRS?

EMRS: Eklavya Model Residential Schools.

Provides free residential education from Classes 6 to 12 to Scheduled Tribe (ST) students in tribal-majority and remote areas.

Nodal Ministry: Ministry of Tribal Affairs.

Managing body: National Education Society for Tribal Students (NESTS).

Aim: Improve educational access while preserving tribal cultural identity.

What did the Panel Find?

428/728 schools completed.

249 under construction.

51 at pre-construction stage.

118 schools operate from temporary government/rented buildings.

Delays have caused construction cost escalation.

Panel suggested an independent monitoring agency and an alternative implementation mechanism.

Scholarship Concerns

Scholarship funds are often released in the next academic year due to delays in State/Union Territory verification.

The Committee criticised the repeated explanation that States need more time for verification.

It also recommended reviewing the ₹8 lakh annual income ceiling for the free coaching scheme for Scheduled Castes (SCs) and Other Backward Classes (OBCs).

Government accepted 14 of 25 recommendations; the panel rejected responses on four issues.

Why is Implementation Weak?

Federal dependence: Central schemes depend on States for construction and verification.

Weak monitoring: Delays accumulate without independent oversight.

Cost escalation: Delays increase construction costs and budget requirements.

Portal mismatch: Scholarship portals and State verification timelines do not align well.

Constitutional Framework

Article 15(4): Enables special provisions for advancement of socially and educationally backward classes and STs.

Article 46: Directs the State to promote educational and economic interests of STs.

Article 275(1): Provides Central grants for tribal welfare and Scheduled Areas.

Article 342: Specifies Scheduled Tribes.

Fifth & Sixth Schedules: Provide special arrangements for administration of Scheduled and tribal areas.

Back2Basics: EMRS

Full form: Eklavya Model Residential Schools.

Nodal Ministry: Ministry of Tribal Affairs.

Implementing body: NESTS, National Education Society for Tribal Students.

Classes: 6 to 12.

Target: ST students in tribal-majority and remote areas.

Purpose: Quality residential education with cultural preservation.

Key Government Initiatives

Pre-Matric & Post-Matric Scholarships: Financial support for ST students.

National Fellowship and Scholarship for Higher Education of ST Students: Supports higher education.

PM-JANMAN: Pradhan Mantri Janjati Adivasi Nyaya Maha Abhiyan, focused on Particularly Vulnerable Tribal Groups (PVTGs).

Dharti Aaba Janjatiya Gram Utkarsh Abhiyan: Development of tribal villages.

Vanbandhu Kalyan Yojana: Umbrella framework for tribal development.

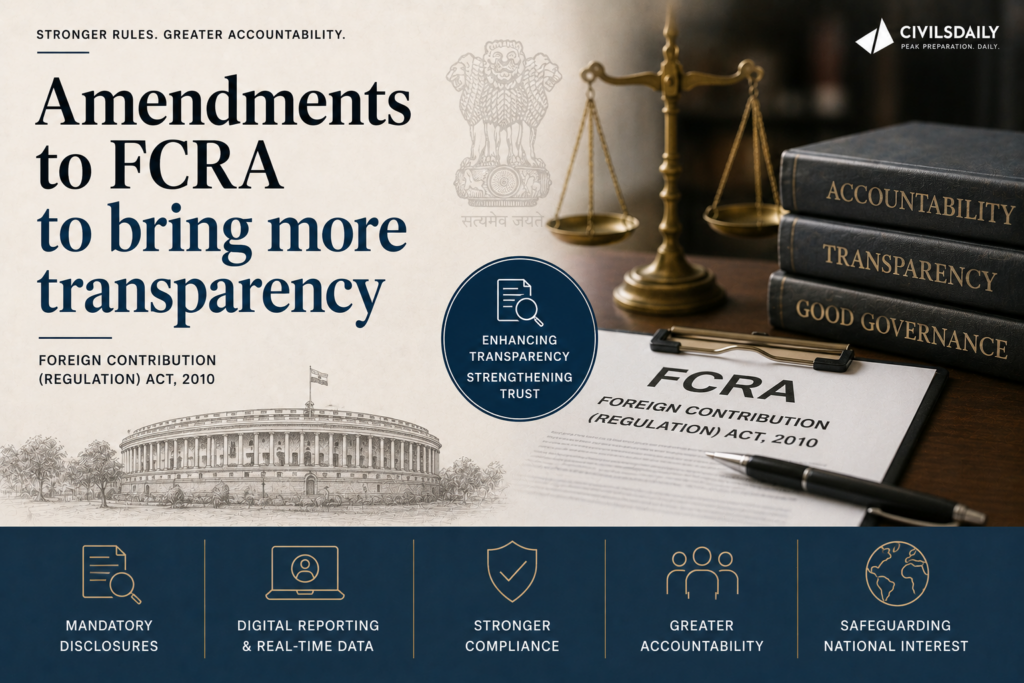

India’s ambassador to the United States publicly defended the amendments to the Foreign Contribution (Regulation) Act after a US Congressman claimed the changes would let the Indian government take control of churches and charities. The envoy argued the amendments bring more transparency and follow national security practice adopted by other democracies.

What is the Foreign Contribution (Regulation) Act?

Definition: The Foreign Contribution (Regulation) Act (FCRA) is the law that governs the acceptance and use of foreign donations by non-governmental organisations (NGOs), civil society bodies, educational institutions, and religious organisations. It requires such bodies to register and channel foreign funds through a laid-down process.

Objective: The stated purpose is to ensure foreign contributions do not compromise national interest or the integrity of public and political life.

What do the 2026 amendments change?

Vesting of assets already in law: When a registration is cancelled or surrendered, foreign contributions and the assets created from them already vest in a State Government authority under a provision in force since 2010.

A designated safeguard authority: The 2026 Bill adds a designated authority to safeguard those assets rather than leaving them unprotected.

A way back: If the organisation restores its registration, all assets and unused funds are returned in full.

Protection for places of worship: Where a cancelled association created property connected to a place of worship, that property passes to another FCRA-registered association of the same faith to ensure continuity of worship.

Faith-neutral application: The Act applies to all organisations regardless of religion, community, or ideology, and faith-based welfare, religious education, and maintenance of places of worship remain eligible for foreign funding.

Why does the government say FCRA regulation is justified?

Sovereign step: Regulating foreign financial flows in public and political spaces is presented as a sovereign act driven by national security concerns.

Internal matter: Legislative decisions concerning India are treated as internal affairs decided by Parliament.

Accepted global feature: The government frames such regulation as a standard feature of modern governance in many democracies.

How do other countries regulate foreign funding?

United States: The Foreign Agents Registration Act (FARA) has operated since 1938, requiring agents of foreign principals to register and disclose their activities.

United States: The Foreign Account Tax Compliance Act (FATCA) has operated since 2010, mandating reporting of foreign-held financial accounts.

Australia: Legislated foreign-influence transparency rules in 2018.

Canada: Enacted its foreign-funding framework in 2024.

United Kingdom: Its foreign-influence registration scheme came into force in July 2025.

European Union: Is currently legislating a comparable framework.

What is the scale of FCRA-regulated funding?

NGO base: India has over three million NGOs, of which only 14,450 hold FCRA registration.

Legislative timeline: India first enacted FCRA in 1976, followed by a new Act in 2010, with further amendments in 2016, 2018, and 2020.

Use of funds: Registered associations routinely receive foreign funds for health, education, disaster relief, research, and humanitarian work.

Conclusion

The government’s position is that the 2026 FCRA Bill adds safeguards for the assets of cancelled associations, a route to restore them, and specific protection for places of worship, framed as a transparency and national-security measure rather than a takeover of religious bodies. The next step is passage of the 2026 Bill and the accompanying Rules, which the government describes as the continuation of a phased strengthening of the law since 1976.

Regulation of Foreign Funding of NGOs in India (Foundational Context)

About: Foreign funding of civil society is regulated so that donations from abroad do not influence India’s internal politics or security.

Administering authority: FCRA is administered by the Ministry of Home Affairs, which grants, renews, and cancels registrations.

Design feature: Registered bodies must receive all foreign contributions in a single designated bank account for monitoring.

Laws and Rules Governing Foreign Contributions

Foreign Contribution (Regulation) Act, 1976: The original law regulating the acceptance of foreign donations by associations.

Foreign Contribution (Regulation) Act, 2010: Replaced the 1976 Act, tightened registration, and required renewal every five years; introduced vesting of assets of cancelled associations in a State authority.

2020 Amendment: Barred sub-granting of foreign funds, capped administrative expenses at 20 percent, and mandated an SBI New Delhi FCRA account.

2026 Bill and Rules: Add a designated authority to safeguard assets of cancelled registrations and protect property linked to places of worship.

Back2Basics: FCRA regulatory framework

Governing Act: Foreign Contribution (Regulation) Act, 2010, as amended.

Administering ministry: Ministry of Home Affairs.

Jurisdiction: Applies to associations, individuals, and companies receiving foreign contributions, excluding certain government bodies.

Key requirement: Mandatory registration or prior permission, five-yearly renewal, and receipt of funds in a designated account.

Challenges to the FCRA Regime

Compliance burden: Frequent amendments and strict banking rules raise the administrative cost for small NGOs.

Registration cancellations: Large-scale cancellations have disrupted health, education, and relief work dependent on foreign grants.

Chilling effect: Uncertainty over renewals discourages legitimate civil society activity.

Ambiguity in definitions: Broad terms such as activities against national interest allow wide discretion.

International friction: Foreign governments and donors periodically object, creating diplomatic exposure.

Way Forward

Predictable timelines: Fix clear, time-bound decisions on registration, renewal, and restoration to reduce uncertainty.

Proportionate compliance: Scale reporting requirements to the size of the organisation.

Transparent grounds: Publish specific reasons for cancellation to allow effective appeal.

Stakeholder consultation: Consult civil society and faith-based bodies before framing subordinate Rules.

[2025, GS2, 10 marks] Civil Society Organizations are often perceived as being anti-State actors rather than non-State actors. Do you agree? Justify.”

The Centre has filed an affidavit in the Supreme Court opposing the introduction of a “creamy layer” income filter within reservations for Scheduled Castes (SCs) and Scheduled Tribes (STs). It has argued that the historical disadvantage faced by these communities is rooted in untouchability and social exclusion, not economic backwardness, and that any change to reservation policy is for Parliament to decide, not the courts.

What is the creamy layer concept?

Definition: The creamy layer is an income and status filter that excludes the socially and economically advanced members of a backward class from reservation benefits. Its purpose is to ensure quota benefits reach the genuinely disadvantaged within a group rather than its better-off sections.

Origin and current scope: It was introduced by the 1992 Indra Sawhney judgment as a test for Other Backward Classes (OBCs). It has never been applied to SCs and STs.

Who does reservation currently apply to in India?

Category-wise quota: Central reservation stands at 15 percent for SCs, 7.5 percent for STs, and 27 percent for OBCs on the non-creamy-layer principle.

Economically Weaker Sections: A 10 percent quota for Economically Weaker Sections (EWS) applies to those outside the SC, ST, and OBC categories.

The ceiling: The Indra Sawhney judgment fixed a 50 percent ceiling on total reservations, though the EWS quota and some State laws now exceed it.

Creamy layer coverage: The creamy layer income exclusion currently applies only to OBCs, not to SCs or STs.

Which constitutional provisions govern reservation?

Article 15(4): Allows the State to make special provisions for the advancement of socially and educationally backward classes, SCs, and STs.

Article 16(4): Permits reservation in public appointments for any backward class inadequately represented in State services.

Article 16(4A) and 16(4B): Enable reservation in promotions for SCs and STs and the carry-forward of unfilled reserved vacancies.

Articles 341 and 342: Empower the President to notify the initial lists of SCs and STs; once notified, inclusion or exclusion can be made only by an Act of Parliament.

Article 335: Requires that reservation claims be balanced with the maintenance of administrative efficiency.

Articles 338 and 338A: Establish the National Commission for Scheduled Castes and the National Commission for Scheduled Tribes.

103rd Constitutional Amendment, 2019: Inserted Articles 15(6) and 16(6) to provide the 10 percent EWS reservation.

What did the petition seek?

Income-based preferences: The Public Interest Litigation (PIL), filed by a politician and advocate, sought income-based preferences across all reserved categories, including OBCs and EWS.

Elite capture argument: It argued that affluent families within the SC and ST categories monopolise reservation benefits, depriving the most marginalised of access to education and public employment.

Reliance on the 2024 ruling: It relied on the 2024 Supreme Court judgment permitting sub-classification of SCs and STs, in which four of the seven Constitution Bench judges suggested extending the creamy layer principle to these groups.

What is sub-classification of Scheduled Castes?

Definition: Sub-classification allows a State to divide the single SC list into sub-groups and reserve a portion of the SC quota for the most backward castes within it. The 2024 judgment upheld this power, holding SCs are not a socially homogeneous class.

Why does the government distinguish SC/ST identification from OBC identification?

Basis of SC status: SCs face historical disadvantage stemming from the practice of untouchability, a form of social exclusion not tied to income.

Basis of ST status: STs are identified by their distinct cultures, geographical isolation, and backwardness.

Basis of OBC status: OBCs are identified primarily through a combination of social, educational, and economic disadvantages, which makes an economic filter relevant to them.

Objective of SC/ST quotas: The stated aim is social equality, overcoming historical discrimination, and inclusive participation in public life, since discrimination against these groups does not occur on the basis of economic conditions.

What legal precedents did the Centre cite?

Indra Sawhney (1992): Upheld the Mandal Commission report on OBC reservation and introduced the creamy layer test, expressly confining it to OBCs and holding it has no relevance for SCs and STs.

E V Chinnaiah (2005): Held that even if a situation ever required excluding a creamy layer from SCs, only Parliament could take the necessary legislative steps.

Separation of powers: The affidavit argued courts cannot direct the executive to adopt a particular policy merely because a fairer or wiser alternative exists, and the judiciary cannot substitute for the legislature in framing public policy.

Why is the demand for a creamy layer contested?

The case for it: Affluent SC and ST families capturing quota benefits leaves the poorest within these groups without access, which undercuts the stated goal of reaching the most marginalised.

The case against it: Caste-based discrimination and untouchability persist regardless of a family’s income, so an economic filter would exclude people who still face social stigma.

The judicial split: The 2024 Bench itself divided, with a minority favouring the extension of the creamy layer to SCs and STs, which keeps the question legally open.

What are the major debates surrounding reservation?

Social justice versus economic upliftment: Whether reservation is a remedy for historical social injustice or a tool for economic advancement, which decides if income can ever be a valid filter.

The 50 percent ceiling: The Indra Sawhney cap is under pressure from State laws and the EWS quota, raising whether the ceiling is still binding.

Sub-classification and creamy layer for SC/ST: The 2024 ruling reopened whether SCs form a homogeneous class and whether the better-off within them should be excluded.

The empirical gap: The absence of updated caste and income data on quota beneficiaries weakens both the elite-capture claim and its rebuttal.

EWS and reserved categories: The exclusion of SCs, STs, and OBCs from the EWS quota is debated as either fair balancing or fresh discrimination.

What are the challenges to applying a creamy layer to SC/STs?

Persistence of untouchability: Social exclusion continues irrespective of income, so an economic test may exclude those still facing discrimination.

Absence of reliable data: No comprehensive dataset tracks the income profile of SC and ST beneficiaries, making a fair income threshold hard to set.

Constitutional bar on judicial rewriting: Under Articles 341 and 342, only Parliament can alter SC and ST entitlements, limiting judicial intervention.

Risk of under-representation: An income filter could shrink the eligible pool and leave reserved seats unfilled where few qualify.

Definitional complexity: Fixing who counts as advanced within a socially stigmatised group is contested and administratively difficult.

Conclusion

The Centre’s position is that SC and ST reservation addresses caste-based social exclusion, not poverty, so the creamy layer test built for OBCs cannot be transposed onto them, and any change is a matter for Parliament. The dispute turns on an unresolved question of whether reservation is fundamentally a social-justice remedy or an economic one. Until Parliament acts or the Supreme Court settles the 2024 split, the creamy layer will not apply to SCs and STs.

Back2Basics:

Indra Sawhney v. Union of India (1992)

What it decided: A nine-judge Supreme Court bench upheld 27 percent OBC reservation based on the Mandal Commission report.

Creamy layer: It introduced the creamy layer exclusion for OBCs and confined it to them.

The ceiling: It capped total reservation at 50 percent, except in extraordinary circumstances.

Promotions: It barred reservation in promotions, a bar later addressed through the 77th Constitutional Amendment and Article 16(4A).

Reservations in India

About: Reservation is a form of protective discrimination that sets aside seats in education, public employment, and legislatures for historically disadvantaged groups.

Scale: It covers SCs, STs, OBCs, and EWS across central and State institutions, with categories and percentages varying by State.

Constitutional anchor: It flows from the equality code in Articles 14 to 16 read with the Directive Principle in Article 46, which directs the State to promote the interests of weaker sections.

Way Forward

Generate quota data: Collect updated caste-wise and income-wise data on beneficiaries to ground policy in evidence rather than assertion.

Respect the legislative domain: Leave changes to SC and ST entitlements to Parliament as required by Articles 341 and 342.

Target the most backward: Use the 2024 sub-classification power to reach the poorest castes within the SC list without diluting the social-justice basis.

Strengthen non-quota support: Expand scholarships, coaching, and infrastructure so advancement does not depend on reservation alone.