[WpProQuiz 1047]

[WpProQuiz_toplist 1047]

UPSC 2022 countdown has begun! Get your personal guidance plan now! (Click here)

[WpProQuiz 1047]

[WpProQuiz_toplist 1047]

UPSC 2022 countdown has begun! Get your personal guidance plan now! (Click here)

[WpProQuiz 1046]

[WpProQuiz_toplist 1046]

UPSC 2022 countdown has begun! Get your personal guidance plan now! (Click here)

The startup ecosystem which has been in overdrive for the past few years — propelled by a combination of factors, but largely, by the era of cheap money — is now showing signs of weakness.

Tech startups are about to witness a tough time ahead. Some startups will survive this period. Many may not. And changes in the dynamics of private markets will also have a bearing on public markets.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

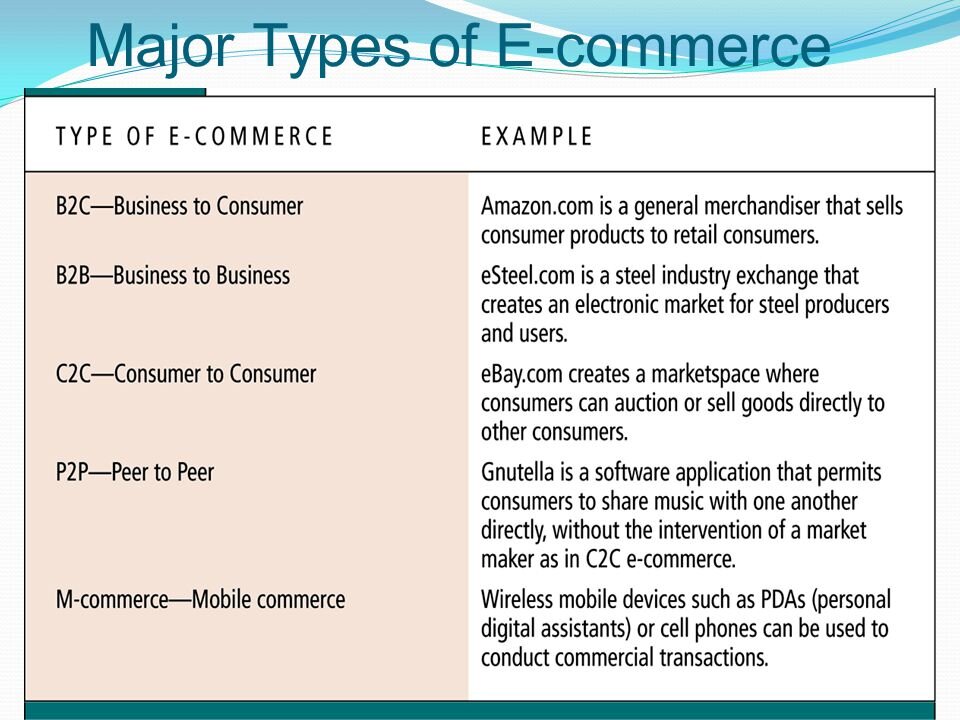

The proliferation of a wide range of e-commerce platforms has created convenience and increased consumer choice. However, these platforms also have given rise to several concerns as well.

The nature of our success in dealing with this change will lie in the ways in which we deal with the concerns of all players.

Topics for Today’s questions:

GS-1 Salient features of world’s physical geography

GS-2 Constitution of India- —historical underpinnings, evolution, features, amendments, significant provisions and basic structure.

GS-3 Applications of S&T in everyday life

GS-4 Public/Civil Services values and ethics in public administration: Status and problems; ethical concerns and dilemmas in government and private institutions; laws, rules, regulations and conscience as sources of ethical guidance;

Question 1)

Q.1 Highlight the various factors affecting salinity of the oceans. Also, elaborate upon horizontal and vertical distribution of ocean salinity. (15 Marks)

Question 2)

Q.2 Political instabilities in various states due to defections is a testament to the loopholes in the anti-defection law. In the context of this, examine the shortcomings and suggest a way forward. (10 Marks)

Question 3)

Q.3 The proliferation of a wide range of e-commerce platforms has created convenience and increased consumer choice. But their dominance has created several issues. Examine those issues and suggest solutions. (10 Marks)

Question 4)

Q.4 In context of the relationship between political executive and civil servants in India, highlight the significance of neutrality in the civil service. (10 Marks)

HOW TO ATTEMPT ANSWERS IN DAILY ANSWER WRITING ENHANCEMENT(AWE)?

Daily 4 questions from General studies 1, 2, 3, and 4 will be provided to you.

A Mentor’s Comment will be available for all answers. This can be used as a guidance tool but we encourage you to write original answers.

You can write your answer on an A4 sheet and scan/click pictures of the same.

Upload the scanned answer in the comment section of the same question.

Along with the scanned answer, please share your Razor payment ID, so that paid members are given priority.

If you upload the answer on the same day like the answer of 11th February is uploaded on 11th February then your answer will be checked within 72 hours. Also, reviews will be in the order of submission- First come first serve basis

If you are writing answers late, for example, 11th February is uploaded on 13th February , then these answers will be evaluated as per the mentor’s schedule.

We encourage you to write answers on the same day. However, if you are uploading an answer late then tag the mentor like @Staff so that the mentor is notified about your answer.

*In case your answer is not reviewed, reply to your answer saying *NOT CHECKED*.

As the political battle in Maharashtra moves to the Supreme Court, the role and powers of the Deputy Speaker are in focus.

In the context of the crisis, references have been made to the landmark judgment in ‘Kihoto Hollohan vs Zachillhu And Others’ (1992).

Try this PYQ:

Q.Which one of the following Schedules of the Constitution of India contains provisions regarding anti-defection?

(a) Second Schedule

(b) Fifth Schedule

(c) Eighth Schedule

(d) Tenth Schedule

Post your answers here.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

A NITI Aayog report has identified that is expected to grow to 2.35 crore by 2029-30.

Do you know?

According to a study released by NITI Aayog, the number of gig workers in India is estimated to be 77 lakh in 2020-21. Isn’t it too low to imagine? Seems like there is huge under-reporting.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

To reinforce its Indo-Pacific strategy, the US – along with Australia, New Zealand, UK and Japan – announced a new Partners in Blue Pacific (PBP) initiative.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)

The World Bank has approved a $250 million loan to support the Government of India’s road safety programme for seven States.

Do you know?

The ‘golden hour’ has been defined as ‘the time period lasting one hour following a traumatic injury during which there is the highest likelihood of preventing death by providing prompt medical care.

UPSC 2023 countdown has begun! Get your personal guidance plan now! (Click here)