BOP on Current Account Versus BOP on Capital Account

| Current Account | Capital Account |

BOP on current account includes the sum of three balances.

|

BOP on capital account includes the sum of two balances

|

| BOP on Current Account is also called Net Foreign Investment because it represents the contribution of foreign trade to Gross national product. | BOP on capital account includes all inward and outward moving capital and investments both Long term and short term).

|

| BOP on current account covers only earnings and spending. It totally excludes any borrowings and lending. | It only includes borrowings and lending by a country. |

Balance of Payment versus Balance of Trade

| Balance of Payment | Balance of Trade |

| It is a Broad Concept | It is a narrower Concept. |

| It includes the sum of both Capital and Current account put together. It includes all international transactions between a host/domestic country and Rest of the World. | It is defined as the difference between the value of exports of goods and services and value of imports of goods and services between countries. |

| It includes items of goods account, services account, unilateral transfers and capital accounts. | BOT= Value of Exports – Value of Imports.

|

|

A positive trade balance(Surplus) is always better and good for a country since it represents an increase in national income. |

Note for Students

There is a difference between the terminologies of Balance of Trade and Goods Balance. Goods or Merchandise Balance is defined as difference between the value of merchandise or goods exports and the value of merchandise or goods imports.

The Balance of Trade on the other hand includes both goods balance (Visible) and services (Invisibles) balance.

Should a negative trade balance (excess of imports over exports) be treated as undesirable for an economy?

The answer is No, because, a developing country needs to import vast quantities of capital goods and technologies to build a strong industrial base. Developing country hardly possess resources needed for industrialisation. They have to import all these resources and in the course of doing so, they have to experience a negative trade balance. Therefore, a negative trade balance cannot be described as undesirable in such a situation. Moreover, once the industrial base is setup, a country can reverse its negative trade balance into a positive trade balance by developing export oriented industries.

BOP Account of a Country

The items 1 to 7 show the total receipts from all sources. These receipts amount to Rs. 1000 Crores.

The items 1(a) to 7(a) Show the total payments on all accounts. These payments amount to Rs. 990 Crores. When item 8 included, the total payment is Rs. 1000 Crores, hence the total credit is equal to the total debit.

Thus, the current account and capital account Balance each other. Thus, the surplus in the current account is equal to the deficit in the capital account. A deficit in the current account is equal to the surplus in the capital account.

In the above-given table, the balance of current account shows a deficit of Rs. 200 crores but there is a corresponding surplus of Rs. 200 crores in the balance of the capital account.

Hence the credit and debit sides balance & the balance of payments is in equilibrium.

The balance of trade of a country may not balance. For instance, if exports exceed imports, there is a surplus and a favourable balance of trade and vice-versa. Only if the value of exports is equal to the value of imports, the balance of trade is said to be in equilibrium.

But the balance of payments always balances because every transaction must be settled. Hence total debits must be equal to the total credits.

Current Account Balance: An Evaluation

The very basic point is to understand what a current account deficit or surplus really means and how it is measured?

- It can be measured as the difference between the value of exports of goods and services and the value of imports of goods and services.

- A deficit simply means that a country is importing more goods and services than it is exporting.

- The current account also includes net incomes such as interests, dividends and unilateral transfers such as Foreign aids.

- Alternatively, Current Account can also be expressed as the difference between national savings and national investments.

- A current account deficit reflects a low level of national savings relative to investments (S<I). whereas, a Current account surplus reflects a high level of domestic savings relative to investments (S>I).

- Current Account = Saving – Investment.

Whether CAD is Necessarily Bad for an Economy or Not?

- In theory, a developing country running a CAD is not necessarily a bad thing. A deficit in current account can increase growth and economic development. Although recent examples and research show that developing countries that run a deficit may not grow faster mainly due to less developed financial markets and inefficient use of foreign capital (Foreign capital used to finance consumptions and interest payments).

- If a current account deficit is financed by borrowing, it is said to be more unsustainable. This is because borrowing is unsustainable in the long term and countries will be burdened with high-interest payments. E.g. Russia was unable to pay its foreign debt back in 1998. Other developing countries have experienced similar repayment problems Brazil, African countries (3rd World debt) Countries with large interest payments have little left over to spend on investment.

- A factor behind the Asian crisis of 1997 was that countries had run up large current account deficits by attracting capital flows (hot money) to finance the deficit. But, when confidence fell, these hot money flows dried up, leading to a rapid devaluation and crisis of confidence.

A Case for India’s Current Account Deficit

- A developing country like India will have more investment opportunities due to its huge domestic market size, but due to its low level of domestic savings, India will not be able to undertake all such opportunities on its own. Thus, a Current account deficit is quite natural.

- When India runs a CAD, it is increasingly getting dependent on foreign capital to finance it. It will lead to building up of liabilities to the rest of the World. Eventually, these liabilities need to be paid back. Common sense suggests that if India uses its borrowed foreign funds in unproductive spending’s that yields no long term productivity gains, then its ability to repay will be affected and will result in insolvency or Bankruptcy. This is what exactly happened in India during 1980’s and 1990’s leading to full-fledged Balance of Payment Crisis.

- During 1980’s and 1990’s, India was not able to generate enough surplus in its capital and current accounts to repay what it had borrowed leading to BOP crisis in 1991.

- Therefore, whether a country should run Current Account Deficit or not will depends on its borrowings from Abroad and on how the country uses its borrowings; if the borrowings/Foreign capital is used efficiently and in productive work then it will generate future revenues and profits that will be greater than the cost of borrowings; but if the borrowings/foreign capital is used inefficiently, and in unproductive works then profits will be less than the cost of borrowings. Hence losses.

Therefore, the key points to remember regarding CAD is as follows:

- If the deficit reflects the excess of imports over exports for a very long time, it may indicate problems and loss of domestic firms’ competitiveness.

- The deficit also reflects the excess of investment over savings, which could reflect a highly productive and growing economy. However, if the deficit is due to low savings rather than high investments, it could be due to unproductive consumption or badly manage government finances (Excess subsidies, high government expenditures, public debt etc.)

- If the foreign capital supporting investment is used productively to generate more output, jobs and exports, then CAD is not at all bad.

- If the foreign capital supporting investment is used unproductively to pay for earlier debt obligations or for consumption purposes, then CAD is bad for an economy.

Evaluation of CAD in India

Period one: 1956 to 1976

The period comprised the second, third, fourth and initial years of Fifth five-year plans. The period saw heavy deficits in the current account. The main reasons for high deficits were three wars with China (1962) and Pakistan (1965 and 1971), severe droughts and food crisis of 1965-66 and first oil price shock of 1973.

Period Two: 1976 to 1979

The period is considered as a golden period for India’s Current Account. The comfortable position was due to increase in private remittances (people working abroad and sending money to their families in home countries) from Gulf countries. The second reason was India witnessing a very strong growth in exports and a reduction in oil imports bill mainly due to fall in oil prices. Efforts were made towards export promotion instead of import substitution. Export subsidies were increased from 20% in 1979-80 to 25% in 1987-88 as a proportion of exports.

Period Three: 1980 to 1991

The period covered roughly the sixth and seventh five-year plan and was marked by a severe balance of payments difficulties. The earnings from private remittances started to fall during the seventh five-year plan. The gulf crisis of 1990-91 further worsened the current account problem.

Period Four: Situation since 1991

The situation since 1991 has been distinctly different from the situation that prevailed earlier. The current account deficit started to improve after 1993. The export performance of Indian industries improves considerably after 1993. The most significant years in India when it comes to current account were; 2001-02, 2002-03 and 2003-04. In all these years, the current account saw a surplus. It is the first time since independence that India witnessed a surplus in its current account. The period also saw strong capital inflows due to strong macroeconomic variables.

The reasons for satisfactory Balance of Payments situation was as follows:

- High Earnings from invisible (Private remittances from abroad and software exports). Earnings from invisible exceeded the deficits on trade account. India was the largest recipient of private remittances (70 Billion US $) in the World in 2012.

- Rise in external commercial borrowings. In addition to external commercial borrowings, the period also witnessed an increase in Non-Resident deposits.

- Role of Foreign Investments. The liberalized policy was put into place. FDI can happen in more markets, ownership structures.

Automatic routes were provided in many sectors where the investor merely has to notify RBI 30 days in advance from bringing the funds. Dividend balancing requirements have been removed.

Role of FIPB: In normal cases, it has to process in 6 months. It can even meet the investor in person to expedite the process. It is empowered to approve 100% FDI in cases of high technology transfers.

As per 2004-05, apart from a negative list, the automatic route within prescribed limits is to be followed by others. Procedures for FDI were also simplified and included things such as conversion of CBs and preference shares into equity.

Source: World Bank, World Development Indicators

Source: World Bank, World Development Indicators

Source: World Bank, World Development Indicators

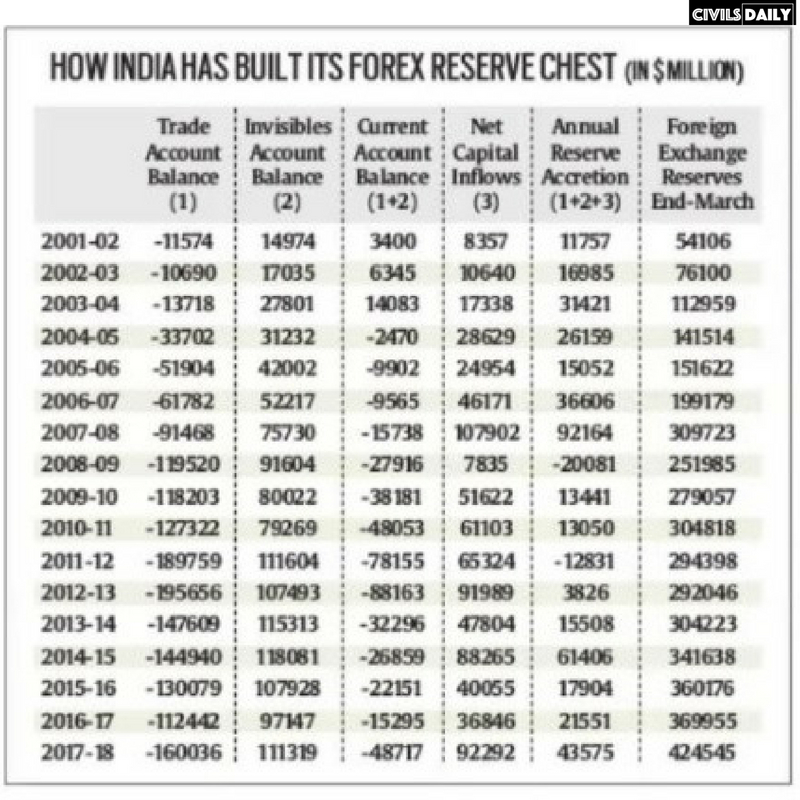

The Problem: New RBI data on India’s Balance of Payments (BoP) for 2017-18 show current account deficit (CAD) at $48.72 bn, the highest since the record $88.16 bn of 2012-13. With CAD expected to widen to $75 bn during this fiscal due to rising crude oil prices. India BOP situation can become vulnerable.

Forex as cushion: India’s forex reserves, at $424.55 billion as on March 2018, are actually the eighth largest in the world. Also, they can finance 10.9 months of imports, compared to 7.8 months in March 2014, 7 months in March 2013 (when there was a mini-BoP crisis, with the current account deficit hitting a peak), and 2.5 months in March 1991 (which forced the country to seek International Monetary Fund assistance).

Therefore, India is not on the verge of any severe BOP crisis as witnessed in 1991. The allusion to a “crisis” from that Balance of Payment standpoint is highly misplaced; the RBI’s current forex war chest is clearly sufficient, both to meet immediate import needs and to stave off a run on the rupee of the kind that was seen during May-August 2013.

How Countries accumulates Reserves:

In standard trade theory, Countries generally accumulate reserves by exporting more than what they import. However, India always had deficits on its merchandise trade account, with the value of its imports of goods far in excess of that of exports. At the same time, the country has traditionally enjoyed a surplus on its ‘invisibles’ account. Invisibles accounts basically cover receipts from export of software services, inward remittances by migrant workers, and tourism and — on the other side — payments towards interest, dividend and royalty on foreign loans, investments and technology/brands, besides on banking, insurance and shipping services.

But with the invisible account surpluses not exceeding trade deficits — it has resulted in the country consistently registering Current Account Deficits.

A country gets foreign exchange not only from exporting goods and services, but also from capital inflows (FDI, ECB and FPI), whether by way of foreign investment, commercial borrowings or external assistance. In India, for most years, net capital inflows have been more than CAD. The surplus capital flows have, then, gone into building foreign exchange reserves. The most extreme instance was in 2007-08, when net foreign capital inflows, at $107.90 billion, vastly exceeded the CAD of $15.74 billion, leading to reserve accretion of $92.16 billion during a single year. However, there have also been years, such as 2008-09 and 2011-12, which saw reserves depletion due to net capital inflows not being adequate to fund even the CAD.

India and Brazil Case Study: They both represent unique cases of emerging economies that have built foreign exchange reserves largely on the strength of their capital account by attracting inflows of foreign funds (FDI, FPI ECB) rather than current account of the BoP.

India is even more unique because its currency, unlike the Brazilian real, is relatively stable, and not under frequent speculative attacks. In theory, a country can keep attracting capital flows to fund CADs so long as its growth prospects are seen to be good, and the investment environment is equally welcoming. It would help, though, if such foreign investment also goes towards augmenting the economy’s manufacturing and services export capacities, as opposed to simply producing or even importing for the domestic market. In the long run, that can help narrow the CAD to more sustainable levels.

The Present Situation: The CAD fell sharply from $88.16 billion in 2012-13 to $15.30 billion in 2016-17, mainly because of India’s oil import bill nearly halving from $164.04 billion to $86.87 billion. However, in 2017-18, the CAD rose to $48.72 billion, courtesy resurgent global crude prices, and is expected to cross $75 billion this fiscal.

There are signs of capital flows slowing down as well. Foreign portfolio investors have, since April 1, made $7.9 billion worth of net sales in Indian equity and debt markets. This is part of a larger sell-off pattern across emerging market economies, in response to rising interest rates in the US, and the European Central Bank’s plans to end its monetary stimulus programme by the end of 2018.

The Swiss investment bank Credit Suisse has forecast net capital flows to India for 2018-19 at $55 billion, which will be lower than the projected CAD of $75 billion. In the event, forex reserves may decline for the first time since 2011-12. The RBI’s data already show the total official reserves as on June 8 at $413.11 billion, a dip of $ 11.43 billion over the level of end-March 2018.

Solving Exports Paradox: Solutions

The factors affecting exports are both domestic and global. External factors consist of global economic conditions, tariff barriers imposed by partner countries, lack of market access, lack of export diversification, Trade wars, Volatility in international currency markets, geopolitical risks, regional trading agreements etc. Domestic factors include macroeconomy management, price elasticity of exports (if price of an exported good is increased by one percent, by how much percentage will the demand fall), exchange rate competency, inflation risk in the economy, government trade policies.

A combination of these factors determines the productivity and overall competitiveness of exports. Therefore, the current decline in India’s exports must be analysed by taking into account the state of play of these external and internal factors.

Many policy thinkers argue that an overvalued rupee is partially responsible for the recent decline in India’s exports. To understand the relationship between exports and exchange rate, we need to look at the growth of India’s exports and real effective exchange rate (REER) between 2002 and 2015.

Till 2013, the relationship between export growth and REER was mixed ( See chart). After this period, it exhibits a clear trend that an overvalued rupee has affected the growth of India’s exports.

This corroborates a well-tested hypothesis that “a stronger currency is not good for export outlook”. Many countries in East Asia including China pursued the strategy of relatively undervalued currency to make their exports competitive in global market under their export led industrialisation.

Therefore, in a highly complex and competitive world, where countries are competing for their export interest, the value of currency must be fairly placed vis-à-vis competing currencies to make one’s export competitive.

Another factor behind the steep decline in India’s exports could be over-dependence on a few markets such as the US and European Union countries which together account for 40 per cent share in India’s total exports. It is particularly important in view of falling demand, stagnant growth and resultant aggregate demand in these countries.

While, India is extensively diversifying its exports market towards Asia through regional and bilateral trading agreements. It has made limited progress in terms of diversifying its exports to non-traditional markets such as South America, Africa and Central and Eastern European countries. Therefore, the diversification of India’s exports market is essential for long term export strategy.

Exchange rate management and competitiveness of Rupee will help in revival of India’s exports. However, exchange rate alone will not resolve India’s export challenge.

India should make continuous efforts in alleviating supply-side bottlenecks to boost sectoral productivity and export competitiveness.

India should adopt a calibrated approach towards structural reforms (connectivity, labour laws, ease of doing, MSME promotion etc) to address cyclical as well as structural factors at the external and internal fronts, which are adversely affecting our export performance.

On the external front, India should engage with likeminded countries and sign free trade agreements which would help us in securing better market access, diversifying our exports and provide greater space for our producers to participate in global production networks.

On the internal front, India should emphasise on reforming domestic policies and institutions dealing with macroeconomic management (exchange rate, inflation and interest rates), standards, intellectual property rights, trade facilitation, and organisations vis-à-vis operational aspects of trade and investment rules and regulations.

Comments

2 responses to “India’s BOP Performance: Balance of Payment versus Balance of Trade, Current Account versus Capital Account”