Payment Banks are the new stripped-down type of banks, which are expected to reach customers mainly through their mobile phones rather than traditional bank branches. They are expected to increase the financial inclusion in the country by providing banking services to the people who are currently out of the reach of banking services.

![]()

source

{kind=link}

- Features of Payment Banks

- Why these Banks were set up?

- Requirements for payment banks

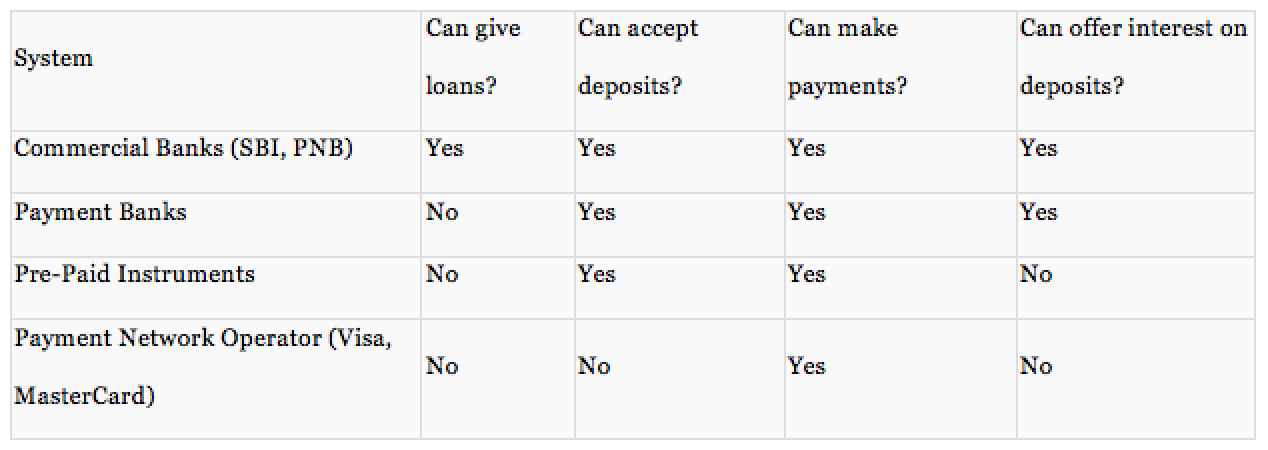

- Major difference between the payment banks, PPI and Commercial banks

- Approved payment banks in India

- Why does India need payment banks when we already have so many PSB?

- How these Payment Banks Will Survive, when they cannot lend?

- How can we make Payment Banks Viable?

- Way ahead

Features of Payment Banks

- Payments Banks can accept demand deposits (only current account and savings accounts) with a ceiling limit of Rs.1 lakh per customer.

- Payment Banks will pay interest at the rate notified by the RBI.

- Payment Banks can issue Debit Cards but not credit cards.

- Payment Banks cannot engage in lending services i.e. they cannot give loans, thus phasing out the fear of NPA.

- The Deposit up to Rs.1 lakh is insured by the DICGC (Deposit Insurance and Credit Guarantee Corporation), same as in bank accounts.

- Payment banks cannot involve in any credit risk and can only invest in less than one year G-Secs or treasury bills.

- Payment Banks will charge a fee as commission. This will be the sole earning for the banks.

- Payment bank will also have to maintain CRR (Cash reserve ratio) just like other Scheduled commercial banks (SBI, PNB, BoB, Dena, ICICI etc)

source

What’s the need for Payment banking in India?

- The goal behind creating these payment banks is to bring about financial inclusion, by making it easier for anyone to get a bank account. That’s also why the cash limit in the accounts is set to just Rs. 1 lakh.

- The Reserve Bank expects payment banks to target India’s migrant labourers, low-income households and small businesses, offering savings accounts and remittance services with a low transaction cost.

- These banks will enable poorer citizens who transact only in cash to take their first step into formal banking. The innovation is also expected to accelerate India’s journey into a cashless economy.

Approved payment banks in India

source

How will these banks will survive, when they cannot lend?

The questions are being raised as to how these new banks will be able to survive in absence of income from lending.

- The payments banks are expected to bring in to their fold millions of customers who are currently not within the fold of the formal financial system. This would lead to large volumes of transactions fetching the payments banks fees – a charge of even 1 or 2 per cent on a large volume can be lucrative on normal cash transfers, which will include government’s direct benefits transfer programmes.

- Moreover, new payments banks can also earn 7.0% or so on their investments in government securities.

- With no need for any provisions or losses on NPAs for these payment banks, they may become fitter banks than existing banks.

How can we make Payment Banks viable?

- Payment Banks will need to be more like these innovative consumer products businesses (particularly digital businesses).

- Digital technology, coupled with a rigorous approach to user interface/user experience and an asset-light strategy, making good use of cloud-based services, will play an important role in enabling Payment Banks to develop simple solutions and acquire customers at low marginal cost.

- The success of payment banks will depend on low-cost technology and high volume of transactions so that charges are reasonable and yet, profits are made.

- If the model is to be a success, a payment bank should neither offer fixed-deposit products nor savings bank accounts.

- Payment banks should offer small-ticket loan products because these products are required in rural areas, as these will discourage borrowers from approaching local moneylenders.

- If payments banks aren’t mandated to have a capital adequacy ratio, it will provide them relief.

- RBI should also reconsider an entry capital of Rs 100 crore for smaller banks, since such low entry-capital requirement may let non-serious players to throw their hat in the ring. This will also help weed out non-serious players from the bank licence fray.

Way ahead

The concept of new payments bank is compelling as it opens another route for inclusive banking. While time will tell how successful this model will be in incremental terms, the RBI on its part has given permission to probably the best players who are capable of making this a reality.

References:

Comments

5 responses to “Differentiated Banks – Payment Banks, Small Finance Banks, etc.”