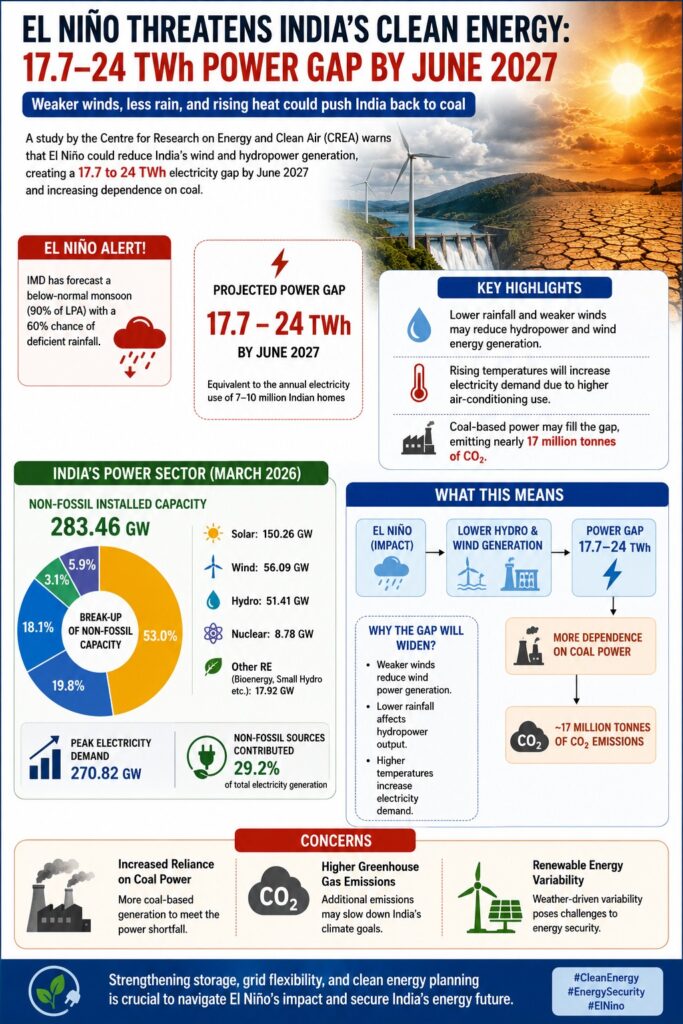

The Centre for Research on Energy and Clean Air (CREA) projects an 18 TWh clean-power shortfall for India by June 2027, driven by El Niño-linked weakness in wind and hydropower output and rising cooling demand. The finding exposes a gap between the record renewable capacity India has installed and the storage needed to actually deliver that capacity as power, forcing the shortfall to be filled by coal.

What has changed in India’s exposure to this El Niño cycle?

Monsoon deficit: June rainfall closed with an all-India deficit of about 40%, the fifth-lowest June since 1901, with the cumulative shortfall at 20% below normal by July 6.

IMD forecast: The India Meteorological Department has forecast below-normal southwest monsoon rainfall at 90% of the long-period average, with a 60% chance of a deficient season.

Generation gap: CREA projects a median shortfall of 17.7 TWh and a severe-case shortfall of 24 TWh, against India’s total 2025-26 generation of about 1,846 billion units.

Emissions cost: A coal-led response to the gap would release an estimated 17 million tonnes of additional carbon dioxide.

Is this a capacity shortfall or a utilisation shortfall?

Record capacity base: Non-fossil installed capacity reached 283.46 GW by March 31, including 150.26 GW of solar and 56.09 GW of wind.

Record additions: India added 44.6 GW of solar and 6 GW of wind capacity in 2025-26 alone.

Curtailment: Grid operators curtailed about 2.1 TWh of solar and wind generation last year to keep coal plants running.

Storage gap: CREA estimates roughly 10 GWh of battery storage could have averted this curtailment.

Why does the response default to coal rather than storage?

Coal’s continuing weight: Coal remains about 42% of installed capacity even as coal generation fell 3.69% over the year.

New coal pipeline: India is adding around 130 GW of new coal capacity to buffer peak demand, such as the 270.82 GW peak recorded on May 21.

Policy diagnosis: CREA director Nandikesh Sivalingam states India must move faster on batteries and grid upgrades to meet future demand surges.

Dispatch logic: Coal capacity can be dispatched on demand without storage investment, making it the default buffer despite its emissions cost.

Conclusion

India’s projected clean-power shortfall is a storage and grid-integration deficit, not a generation deficit. The 130 GW of new coal capacity being planned addresses the symptom of demand variability, not the missing battery and transmission investment needed to convert installed renewable capacity into reliable output. Without storage scaling alongside capacity addition, each future El Niño cycle will repeat the same coal fallback and its emissions cost.

The Prime Minister launched the Modified UDAN Scheme (Viksit UDAN) and inaugurated the New Terminal Building at Jodhpur Airport, marking the next phase of India’s regional aviation expansion.

About UDAN

UDAN (Ude Desh ka Aam Nagrik) was launched in October 2016 under the Ministry of Civil Aviation.

Objective: Make air travel affordable, accessible, and widespread by improving regional connectivity through the Regional Connectivity Scheme (RCS).

Achievements of UDAN

669 regional routes operationalised.

95 airports, heliports, and water aerodromes connected.

Over 1.66 crore passengers benefited.

Key Features of Modified UDAN (2026)

Approved: 25 March 2026.

Outlay: Nearly ₹29,000 crore over 10 years.

Develop 100 new aerodromes from unserved airstrips.

Note: An aerodrome is any defined location on land or water used for the arrival, departure, and movement of aircraft

Develop 200 modern helipads.

Continued Viability Gap Funding (VGF) for regional airlines.

Operations and Maintenance support for regional airports.

Promotes indigenous aircraft such as HAL Dhruv and Dornier under Atmanirbhar Bharat.

New Terminal Building, Jodhpur Airport

Built by the Airports Authority of India (AAI) at a cost of ₹480 crore.

Area: 23,342 sq. m.

Capacity: 20 lakh passengers annually and 1,500 passengers during peak hours.

Features 20 check-in counters, 6 aerobridges, advanced baggage handling, and sustainable design targeting a 5-Star GRIHA rating.

Significance

Improves connectivity to Tier-2, Tier-3, and remote regions.

Boosts tourism, trade, employment, and regional economic growth.

Strengthens last-mile air connectivity.

Supports the vision of Viksit Bharat 2047.

[2024] Consider the following airports: 1. Donyi Polo Airport 2. Kushinagar International Airport 3. Vijayawada International Airport In the recent past, which of the above have been constructed as Greenfield project?

The Government highlighted the achievements of the Ethanol Blended Petrol (EBP) Programme, its policy evolution, and clarified common misconceptions regarding E20 fuel.

What is the EBP Programme?

The EBP Programme promotes blending ethanol with petrol to:

Reduce crude oil imports and improve energy security.

Lower greenhouse gas emissions.

Increase farmers’ income.

Promote renewable transport fuel.

India achieved 20% ethanol blending (E20) in 2025-26, five years ahead of the target.

Policy Evolution

2003: EBP Programme launched.

2018: National Policy on Biofuels notified.

2021: E20 target advanced from 2030 to 2025-26.

2025-26: 20% blending achieved.

Key Achievements

Ethanol blending: <1.5% (2013-14) → 20% (2025-26)

Ethanol production capacity: 421 crore L → ~2,000 crore L

Foreign exchange saved: ₹1.90 lakh crore+

Crude oil substituted: 310 lakh MT

CO₂ emissions reduced: 930 lakh MT

Additional farmer income: ₹1.60 lakh crore+

Feedstocks

Sugarcane juice, Molasses, Maize, Surplus rice, and Other approved agricultural biomass

Key Facts on E20

Does not reduce mileage by 30%; actual impact is marginal.

No evidence of widespread engine damage after extensive testing.

Higher octane fuel improves combustion and lowers emissions.

Does not affect vehicle warranty or insurance.

Raw sugarcane juice is not mixed with petrol; ethanol is produced through fermentation and distillation.

Modern distilleries use Zero Liquid Discharge (ZLD) systems.

Fuel-grade ethanol contains no sugar and does not attract insects.

[2025] Consider the following statements: Statement I: Of the two major ethanol producers in the world, i.e., Brazil and the United States of America, the former produces more ethanol than the latter. Statement II: Unlike in the United States of America where corn is the principal feedstock for ethanol production, sugarcane is the principal feedstock for ethanol production in Brazil. Which one of the following is correct in respect of the above statements?

[A] Both Statement I and Statement II are correct and Statement II explains Statement I

[B] Both Statement I and Statement II are correct but Statement II does not explain Statement I

[C] Statement I is correct but Statement II is not correct

[D] Statement I is not correct but Statement II is correct

IRDAI is working on a disclosure framework and a possible commission cap for insurance intermediaries, using powers granted by the January 2026 amendment to the Insurance Act. The move exposes a tension between commission-driven competition for distribution access and policyholder protection, since insurers with largely similar products have long competed on payouts to intermediaries rather than on price. Gross commission outgo across the industry crossed Rs 1 lakh crore in FY25, with the commission expense ratio for non-life insurers rising from 6.21% to 6.86% in one year.

What twin-track regulatory response has IRDAI designed for insurance intermediaries?

Disclosure threshold: Intermediaries whose commission income exceeds a prescribed threshold must file detailed annual disclosures with the regulator.

Scope of disclosure: Required disclosures cover commission earnings, related-party transactions, profits from operations, and dividend repatriation to promoters or parent entities.

Public accountability mechanism: Intermediaries must publish this information on their own websites, not only file it with the regulator.

Parallel price-control track: IRDAI is separately drafting a proposal to cap commission payouts by insurers to distributors.

Legal basis: The commission cap is enabled by the January 2026 amendment to the Insurance Act, which for the first time empowered IRDAI to prescribe commission ceilings.

Sectoral range today: In the non-life segment, commission to brokers currently ranges from 2.5% to 10%, illustrated by the example of a $20 billion fleet airline paying $30 million in annual premium.

Why has commission-driven competition persisted despite calls for policyholder-centric conduct?

Product homogeneity: Insurers offer products broadly similar in coverage and pricing, which removes price and product design as competitive levers.

Commission as the substitute lever: Intermediaries decide which products to distribute based on commission structures and incentive payouts rather than product merit.

Distribution-channel competition: Insurers compete for access to intermediaries, not for the end policyholder, inverting the intended direction of market discipline.

Renewal-commission bias: Intermediaries favour products generating recurring renewal commissions, which skews recommendations toward insurer payout structures rather than policyholder need.

Persistence of mis-selling: Mis-selling and under-cutting by insurers to secure business continue despite existing disclosure and conduct norms.

Digital paradox: Digital platforms, web aggregators and insurtech firms lower customer acquisition costs and raise price transparency, yet this has intensified rather than reduced competition for distribution access.

What does the scale of commission expenditure reveal about the distribution model?

Cross-industry threshold breached: Total commission paid by 26 life and 28 non-life insurers crossed the Rs 1 lakh crore mark in FY25.

Non-life sector breakdown: Public sector general insurers paid Rs 9,335 crore, private general insurers Rs 30,498 crore, standalone health insurers Rs 7,365 crore, and specialised insurers Rs 67 crore in commission for 2024-25.

Non-life aggregate: These four segments cumulatively totalled Rs 47,266 crore in gross commission expense for the entire non-life insurance industry.

Life insurance outlay: Life insurers paid Rs 60,800 crore in commission during 2024-25, exceeding the entire non-life industry’s commission outgo.

Rising commission expense ratio: The commission expense ratio, measured as commission expenses as a percentage of premium, rose from 6.21% in 2023-24 to 6.86% in 2024-25 for non-life insurers.

Direction of the trend: The ratio moved upward in the same year IRDAI issued its consultation paper, indicating the disclosure-stage proposal has not yet altered underlying commission behaviour.

What precondition is missing for a commission cap to correct mis-selling rather than relocate it?

Non-cash incentive channels: Insurers currently offer performance-linked incentives and other commercial benefits alongside commission, none of which a commission cap alone would touch.

Undefined enforcement mechanism: The consultation paper details disclosure content but does not specify how breaches of a future commission ceiling would be monitored or penalised.

Distribution-channel dependence unaddressed: A cap constrains payout levels but does not remove insurers’ underlying dependence on intermediaries to reach policyholders in a product-homogeneous market.

Threshold design gap: The disclosure obligation applies only above a prescribed commission-income threshold, leaving intermediaries below that threshold outside the enhanced-disclosure regime.

No linkage to policyholder outcomes: The proposed framework tracks intermediary earnings and related-party transactions but does not tie disclosure or caps to policyholder complaints or mis-selling data.

Will a commission cap eliminate the incentive to mis-sell or merely shift it to non-commission channels?

Incentive substitution risk: Insurers can replace capped commissions with performance-linked incentives, trips, or other non-cash benefits to retain intermediary loyalty.

Disclosure without a cap has not worked: The consultation paper preceded the cap proposal by weeks, and the commission expense ratio still rose in the same reporting year.

Cap without enforcement detail: IRDAI has not yet formally proposed a cap, and the reported draft carries no disclosed enforcement architecture.

Underlying driver untouched: Product homogeneity, the root cause of commission-based competition, is not addressed by either disclosure or a cap.

Segment disruption acknowledged: The article itself notes a commission cap “could disrupt the segment,” indicating the regulator anticipates displacement effects on distribution economics rather than a clean resolution.

Conclusion

IRDAI’s shift from disclosure norms to a commission cap signals that transparency alone has not corrected commission-driven mis-selling in a market where product homogeneity leaves commission as the primary competitive lever. Unless the cap is paired with enforcement against non-cash incentive substitutes, it risks displacing rather than eliminating the underlying incentive to compete for distribution access at the policyholder’s expense.

India is developing a standardised template for future High Speed Rail (HSR) corridors based on the experience of the Mumbai Ahmedabad High Speed Rail (MAHSR) project. The initiative aims to reduce costs, accelerate construction, strengthen indigenous manufacturing, and create a nationwide bullet train network.

Standardised High Speed Rail Model

MAHSR will serve as the blueprint for future bullet train corridors.

Common engineering standards for Piers and viaducts, Ballastless tracks, Station structures, Overhead electrification, and Signalling systems

Site specific foundation designs based on soil conditions.

Benefits:

Faster project execution

Lower construction costs

Easier maintenance and spare part management

Uniform training and procurement

Indigenous Manufacturing under Make in India

Integral Coach Factory (ICF) and BEML are developing 280 kmph indigenous high speed trainsets.

Indian companies are manufacturing Slab track systems, Construction equipment, and High speed rail components

Aditya Complex (Bengaluru) supports manufacturing of B-28 coaches.

IITs, skill development, and Japanese technology transfer are strengthening domestic capabilities.

Mumbai Ahmedabad High Speed Rail (MAHSR)

India’s first bullet train corridor, Length: 508 km, Stations: 12, Design Speed: 350 kmph, Operational Speed: 320 kmph, Travel Time: About 1 hour 58 minutes, Expected first operation: August 2027, and First operational section: Surat to Vapi

Technical Features

Technology: Based on Japanese Shinkansen technology

Electrification:2×25 kV AC overhead traction system. More than 20,000 OHE masts

Power Infrastructure:12 traction substations. 2 depot substations. 16 distribution substations

Track System: J-Slab ballastless track technology introduced in India for the first time.

Rolling Stock Depots: Sabarmati, Surat, and Thane

[2025] Consider the following statements: I. Indian Railways have prepared a National Rail Plan (NRP) to create a future ready railway system by 2028. II. Kavach’ is an Automatic Train Protection system, development in collaboration with Germany. III. ‘Kavach’ system consists of RFID tags fitted on track in station section. Which of the statements given above are not correct?

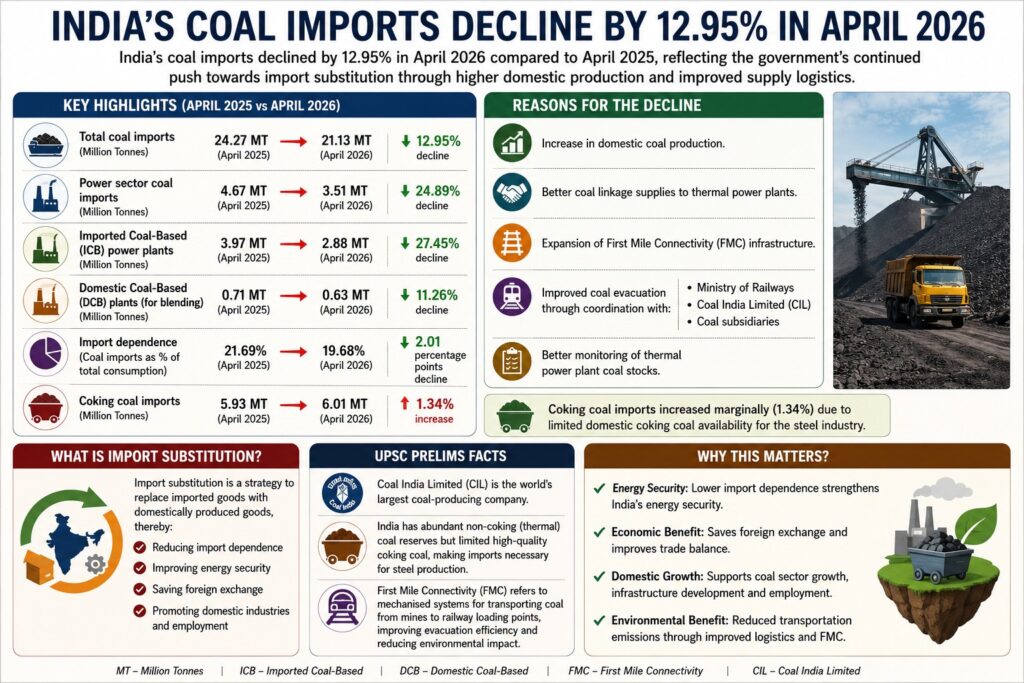

India’s coal imports declined by 12.95% in April 2026 compared to April 2025, reflecting the government’s continued push towards import substitution through higher domestic coal production and improved supply logistics.

Key Highlights

Total coal imports fell from 24.27 MT (April 2025) to 21.13 MT (April 2026), a decline of 12.95%.

Power sector coal imports declined by 24.89%, from 4.67 MT to 3.51 MT.

Imported Coal-Based (ICB) power plants recorded the steepest fall in imports: 3.97 MT → 2.88 MT (down 27.45%).

Domestic Coal-Based (DCB) plants importing coal for blending reduced imports by 11.26%: 0.71 MT → 0.63 MT.

Import dependence (coal imports as a share of total consumption) declined 21.69% → 19.68%.

Coking coal imports increased marginally by 1.34%: 5.93 MT → 6.01 MT, due to limited domestic coking coal availability for the steel industry.

Reasons for the Decline

Increase in domestic coal production.

Better coal linkage supplies to thermal power plants.

Expansion of First Mile Connectivity (FMC) infrastructure.

Improved coal evacuation through coordination with: Ministry of Railways, Coal India Limited (CIL), and Coal subsidiaries.

Better monitoring of thermal power plant coal stocks.

UPSC Prelims Facts

Coal India Limited (CIL) is the world’s largest coal-producing company.

India has abundant non-coking (thermal) coal reserves but limited high-quality coking coal, making imports necessary for steel production.

First Mile Connectivity (FMC) refers to mechanised systems for transporting coal from mines to railway loading points, improving evacuation efficiency and reducing environmental impact.

[2019] Consider the following statements: 1. Coal sector was nationalized by the Government of India under Indira Gandhi. 2. Now, coal blocks are allocated on lottery basis. 3. Till recently, India imported coal to meet the shortages of domestic supply, but now India is self-sufficient in coal product. Which of the statements given above is/are correct?

PYQ Relevance[UPSC 2022] Do you think India will meet 50 percent of its energy needs from renewable energy by 2030? Justify your answer. How will the shift of subsidies from fossil fuels to renewables help achieve the above objective? Explain. Linkage: The PYQ asks whether India can meet 50% renewable energy needs by 2030 and whether shifting subsidies from fossil fuels to renewables helps achieve it. The article shows that even with strong renewable capacity growth, meeting such targets depends on coordinating generation, transmission, storage and distribution, not subsidy shifts alone.

Mentor’s Comment

The Indian National Science Academy (INSA) released a policy brief in May 2026 proposing a unified, four-pillar national energy framework. As India’s energy mix diversifies, the binding challenge shifts from expanding capacity to coordinating generation, transmission, storage and distribution across a fragmented institutional landscape. India’s energy transition has moved from an input problem of building capacity to an output problem of coordinating a system it has deliberately diversified. The INSA’s four-pillar framework formalises this shift through institutional integration rather than further capacity expansion.

Why has India’s energy transition reached a point where coordination, not capacity, is the binding constraint?

Renewable capacity has scaled sharply: Installed renewable capacity grew from approximately 40 GW in 2015 to approximately 260 GW by 2025, a more than six-fold increase.

Import dependence persists despite expansion: Domestic energy production continues to grow, but India remains dependent on imports for a significant share of oil and natural gas requirements.

Demand growth adds to system complexity: Energy demand is expected to grow steadily as economic development, industrialisation and urbanisation continue.

Multiple objectives must be managed together: Energy security, affordability, sustainability and economic growth compete for priority, requiring coordinated planning across sectors and fuels.

Access foundations are already built: The Saubhagya Scheme and the Pradhan Mantri Ujjwala Yojana have delivered near-universal household electrification and clean cooking fuel access, shifting the policy problem from access to integration.

Two national targets set the horizon: India has committed to energy self-reliance by 2047 and net-zero emissions by 2070, both of which require an increasingly integrated approach to planning and governance.

What does the INSA’s four-pillar framework propose to structure this coordination?

Adequacy: Ensures reliable and diversified energy supply through a balanced portfolio of conventional and emerging sources, backed by modern infrastructure, storage and digital technologies.

Access: Builds on existing electrification and clean cooking gains to strengthen last-mile delivery, improve service quality and expand decentralised energy solutions.

Affordability: Relies on innovative financing mechanisms, efficient markets and consumer-focused safeguards to keep the transition economically viable for households, businesses and industries.

Appropriate sustainability: Rejects a one-size-fits-all model and aligns sustainability pathways with India’s developmental priorities, resource endowments, and social and regional context.

Cross-cutting enablers are named separately: Circular economy practices and Carbon Capture, Utilisation and Storage (CCUS) are identified as enablers that support renewable deployment and reduce industrial emissions.

How does the framework sequence implementation across time?

Near-term priorities are capacity-and-institution focused: Strengthening infrastructure, accelerating renewable deployment, supporting emerging technologies such as green hydrogen, and building institutional mechanisms for long-term coordination.

Long-term emphasis shifts toward integration: Over time, the focus moves toward deeper integration of low-carbon technologies, expanded use of bio-resources, and a more interconnected, resilient energy ecosystem.

The transition is treated as multi-decade, not single-cycle: The framework explicitly recognises that energy transitions occur over decades, avoiding premature closure on any single pathway.

Region-specific pathways are built into the design: The sustainability pillar supports local communities, workforce development and region-specific transition pathways rather than a uniform national template.

Can a single national framework unify a deliberately diversified and decentralised energy system?

Diversification was itself the policy achievement: India deliberately diversified its energy mix, growing renewable capacity six-fold while pursuing decentralised solutions under the access pillar.

The same brief now demands coordination across that diversity: As the energy ecosystem becomes more diverse, the brief argues that coordination among generation, transmission, storage, distribution and emerging technologies becomes increasingly necessary.

No single technology is assigned the transition: Coal, renewables, biomass, natural gas, waste-to-energy systems and emerging clean technologies are each given a continuing role, ruling out any single-pathway solution.

The framework unifies without standardising: The appropriate sustainability pillar explicitly rejects a one-size-fits-all approach, meaning a “unified” framework must accommodate region-specific and sector-specific variation rather than remove it.

Institutional authority remains unspecified: The brief calls for developing institutional mechanisms to facilitate long-term coordination but does not identify which entity holds authority when the four pillars’ objectives conflict across sectors.

Conclusion

India’s energy transition problem has shifted from expanding capacity to coordinating a system it has deliberately diversified. The INSA’s four-pillar framework formalises adequacy, access, affordability and sustainability as national objectives, but leaves unresolved which institutional mechanism will adjudicate conflicts between diversification and unification as the transition deepens. Coordination, not capacity, is now the binding constraint on India’s energy security by 2047 and its net-zero target by 2070.

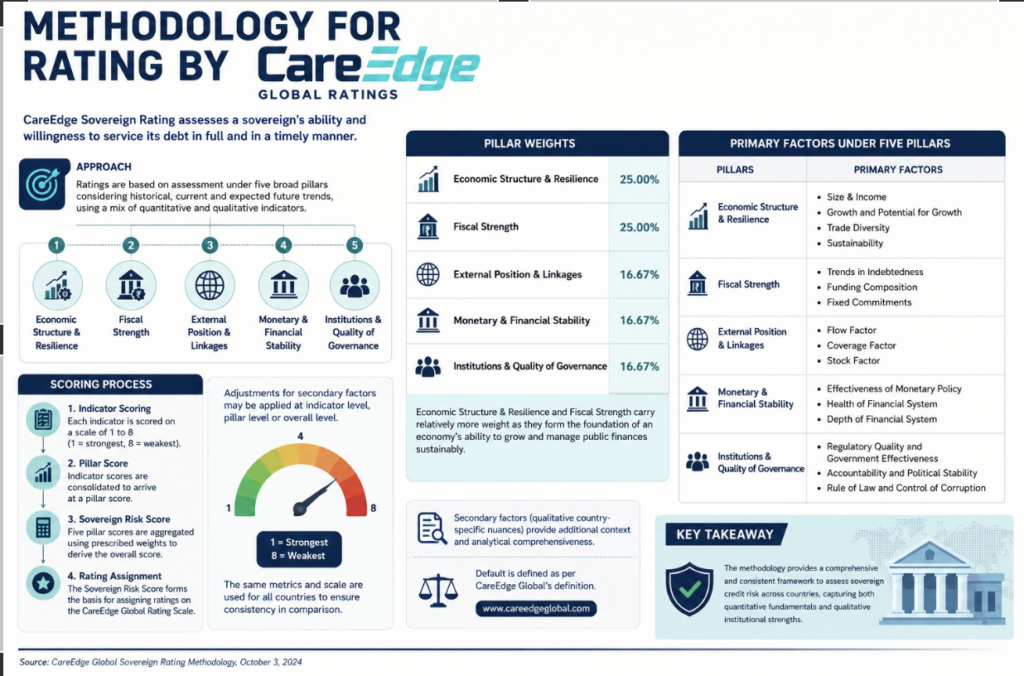

Union Minister of Commerce, at a London business conference, accused global sovereign credit rating agencies of being “unfair to India” while praising India-headquartered CareEdge Ratings as “objective.” The remark reopens a standing government charge that international agencies keep India’s rating just above junk grade by over-weighting subjective, opinion-based judgments of “willingness to repay” over India’s stronger, verifiable “ability to repay” data.

What are sovereign credit ratings?

A sovereign credit rating is an independent evaluation of a country’s creditworthiness.

It measures a government’s ability and willingness to repay its debt obligations, helping global investors assess the risk of investing in that nation’s bonds or lending it money.

Working: Ratings are assigned by independent credit rating agencies, most notably Standard & Poor’s (S&P), Moody’s, and Fitch Ratings.

High Ratings (e.g., AAA, Aaa): Signal strong economic stability, low risk of default, and allow the government to borrow money at lower interest rates.

Low Ratings (e.g., BB+, Ba1): Indicate higher credit risk and are typically labeled as “speculative” or “junk” grade, forcing the country to pay higher interest to compensate investors for the increased risk.

How do rating agencies define and measure sovereign creditworthiness?

Rating universe: India is rated by seven international sovereign credit rating agencies, S&P, Moody’s, Morningstar DBRS, Fitch, Japanese Credit Rating Agency (JCRA), Rating and Investment Information (R&I), and CareEdge Ratings. The three most widely accepted globally are S&P, Fitch, and Moody’s.

Rated entities: The same alphabet-scale logic applies not only to sovereigns but to companies, municipal corporations, and state governments.

Scale mechanics: Fitch and S&P run from AAA downward through AA+, AA, AA-, A+, A, A- into the B-grade band, ending at D for default. Moody’s follows an identical structure using different letters, starting at Aaa.

Price-of-risk function: The rating fixes the interest rate at which an entity can borrow. AAA signals zero default risk and the lowest borrowing cost; each downward notch raises the rate to compensate lenders for higher perceived risk.

The dual metric: Ability to repay is quantitative, drawn from hard, verifiable macroeconomic data. Willingness to repay is qualitative, resting on an agency’s opinion of intent rather than capacity. This distinction structures India’s later grievance against the agencies.

What has India’s rating trajectory looked like?

Persistent floor: Across most agencies, India has stayed at the lowest rung of investment grade, a grade or two above junk status, the threshold at which institutions stop lending for fear of default.

Long stagnation: Until recently, this rating stayed unchanged for more than a decade, and in some cases for nearly two decades.

S&P upgrade: S&P raised India’s long-term sovereign rating to BBB from BBB- in August 2025, its first upgrade of India in 18 years.

Moody’s upgrade: Moody’s raised India to Baa2 (equivalent to BBB) from Baa3 in 2017, its first upgrade of India in 13 years.

Other 2025 movements: R&I upgraded India to BBB+ from BBB in September 2025; Morningstar DBRS upgraded India to BBB in May 2025.

Why does the government call the ratings agencies’ methodology unfair to India?

Persisting grievance despite upgrades: Even after the 2025 upgrades, India’s rating remains just above junk grade. India argues that agencies have not credited India’s growth story, its fundamentals, or its sovereign capabilities as a rating agency should.

Official continuity: The Finance Minister of India has separately called for reform of the agencies’ methodologies, establishing this as a standing government position rather than a one-off remark.

Economic Survey precedent: The 2020-21 Economic Survey devoted a full chapter to the issue. It noted this was the first time the world’s fifth-largest economy had been assigned such a low rating.

Ability case made: The Survey argued India’s macroeconomic fundamentals were strong enough to demonstrate ability to repay debt.

Willingness case made: It also argued India’s record of never defaulting on sovereign debt despite multiple crises should establish willingness to repay.

Core allegation: The central charge is that agencies weigh the qualitative willingness metric (grounded in the opinions of a small group of experts and prone to subjectivity) more heavily than the quantitative ability metric, on which India performs comparatively well but which carries lower weightage.

Why is CareEdge Ratings being held up as the corrective model?

Origin and perception: CareEdge is the first sovereign ratings agency headquartered in India, feeding the perception that it can better capture the ground realities of the Indian economy.

Methodological difference: CareEdge’s own methodology note assigns primary importance to quantitative factors, directly inverting the qualitative-heavy approach India accuses the major agencies of using.

Political endorsement: Goyal singling out CareEdge as “objective” aligns with the government’s broader argument that a quantitative-first method would rate India more favourably.

Conclusion

India’s persistently sub-BBB sovereign rating, despite improving fundamentals, stems from ratings agencies’ structural preference for qualitative, opinion-driven assessments of willingness to repay over quantitative measures of ability to repay. This is a metric on which India performs well. The government’s promotion of CareEdge Ratings, a domestic agency that weights quantitative factors more heavily, functions less as a technical fix than as an assertion that India deserves to be rated on its own terms. This does not resolve who sets the criteria for creditworthiness: India’s grievance can only be addressed if the major agencies alter their own weighting, a decision outside New Delhi’s control. Until then, India’s rating will likely continue to lag its economic weight.

PYQ Relevance

[UPSC 2017] Among several factors for India’s potential growth, the savings rate is the most effective one. Do you agree? What are the other factors available for growth potential?

Linkage: Sovereign credit ratings directly influence investment flows and borrowing costs, which affect capital formation and India’s long-term growth potential. The article argues that global rating agencies undervalue India’s macroeconomic strengths and growth prospects, thereby increasing borrowing costs despite strong economic fundamentals.

The closure of the Strait of Hormuz in 2026 disrupted India’s crude oil and LPG supply chains, testing the country’s energy security architecture in real time. India’s refineries absorbed the crude shock through rapid sourcing diversification, but the same crisis exposed that LPG dependence is structurally different and cannot be diversified the same way, pushing coal based DME production onto the national agenda.

How did India’s refining sector convert two decades of indigenous investment into crisis resilience during the 2026 Hormuz disruption?

Diversified supplier base: India’s crude supplier base nearly tripled over two decades, forcing refineries to build capability to process multiple crude specifications rather than a single feedstock.

Indigenous technical capability: Investments in indigenous research, metallurgy, process innovation, and workforce training gave refineries the ability to process feedstock across a broad range of specifications.

Speed of the pivot: Within weeks of the Hormuz closure, non-Hormuz sourcing rose from 55% to 70% of India’s crude intake.

LPG production surge: Under the LPG control order, domestic LPG production rose from 35 Thousand Metric Tonnes (TMT) per day to 54 TMT per day within five days. Engineers achieved this by adjusting fractionation and cracking units in real time.

Engineering, not accounting: The production increase was an outcome of technical capability, not a redirection of existing supply.

Did refinery flexibility solve India’s LPG vulnerability, or did it only manage the immediate crisis?

Different nature of the two problems: Refinery flexibility solved the problem of keeping crude flowing through a fixed set of plants. It did not solve the deeper problem of LPG import concentration.

Crude diversification is engineerable: A refinery can be engineered to process crude from 40 different countries.

LPG diversification is not engineerable: LPG cannot be sourced from 40 different geographies. The molecule is drawn overwhelmingly from a handful of Gulf and Atlantic Basin producers.

Refining efficiency is not the solution: Processing the same imported molecule more efficiently does not reduce the underlying dependence.

The real solution is substitution: The long-term fix requires producing a domestic molecule that serves the same function as LPG.

What is Dimethyl Ether (DME), and how does India propose to substitute a domestic molecule for imported LPG?

Definition: DME is a clean-burning gas chemically similar to LPG. It blends directly into existing cylinders and pipelines, so it requires no new distribution infrastructure.

Production route: DME is produced through coal gasification. Coal gasification converts coal into syngas, and syngas is then converted into DME.

Resource base: India possesses some of the world’s largest coal reserves, giving it abundant raw material for DME production.

Regulatory approval: The Bureau of Indian Standards has approved blending up to 20% DME with LPG.

Quantified impact: A 20% blend sourced from coal gasification could displace roughly 6.3 million tonnes of LPG imports annually, saving nearly ₹34,000 crore in foreign exchange each year.

Origin of the technology: Scientists at CSIR’s National Chemical Laboratory developed the indigenous technology for converting methanol into DME years before the crisis.

Is India’s coal gasification ambition backed by matching execution capacity?

Policy commitment: The Union Cabinet approved a ₹37,500 crore scheme to promote surface coal and lignite gasification, citing the West Asia crisis as part of its rationale.

Scale of ambition: The scheme targets 100 million tonnes of coal gasification annually by 2030.

Investment incentive: The scheme provides an incentive of up to 20% of plant and machinery costs.

Tenure certainty: The scheme extends coal linkage tenure to 30 years. Capital-intensive projects need this horizon before committing investment.

Fast-tracked approval: The Centre for High Technology under the Ministry of Petroleum and Natural Gas approved scaling up the indigenous DME pilot technology within the crisis window, without the delay typical of technology-to-deployment transitions.

Feedstock gap: India’s coal has a higher ash content than the cleaner coal that underpinned China’s coal-to-chemicals industry.

Capacity gap: Domestic gasification capacity remains far below the scheme’s stated ambition.

Nature of the remaining challenge: Closing this gap is a question of industrial discipline and investment. Policy intent has already been settled.

Conclusion

India’s refinery flexibility during the Hormuz crisis proved that indigenous technical capability, once built, can absorb supply shocks. This capability did not solve India’s LPG dependence. LPG is sourced from a handful of Gulf and Atlantic Basin producers and cannot be diversified the way crude oil can. Coal-based DME production is the domestic substitute for the imported molecule. Policy commitment for it is now in place through the coal gasification scheme. What remains is execution: closing the ash-content gap and scaling gasification capacity to the technical depth China has spent two decades building.

Value Addition

What is Coal Chemistry?

Coal chemistry refers to the conversion of coal into high-value chemicals, fuels and industrial feedstocks through physical and chemical processes instead of burning it directly for power generation.

It enables coal to produce cleaner fuels, fertilizers, petrochemicals and specialty chemicals, thereby improving the economic value of domestic coal resources.

Major Products of Coal Chemistry

Process

Output

Coal Gasification

Syngas (CO + H₂)

Syngas Conversion

Methanol

Methanol Conversion

Dimethyl Ether (DME)

Fischer-Tropsch Process

Synthetic Diesel

Coal-to-Chemicals

Ammonia, Urea, Olefins, Hydrogen

What is Coal Gasification?

Coal gasification is the process of converting coal into synthesis gas (syngas) by reacting coal with oxygen, steam and controlled heat under high pressure.

Instead of burning coal directly, it transforms coal into a cleaner intermediate fuel that can be further processed into Hydrogen, Methanol, Dimethyl Ether (DME), Synthetic Natural Gas (SNG), Fertilisers, and Petrochemicals

What is Dimethyl Ether (DME)?

Dimethyl Ether (DME) is a clean-burning gaseous fuel produced from methanol derived through coal gasification.

Key Features

Chemically similar to LPG

Can be blended with LPG

Compatible with existing LPG cylinders and pipelines

Produces lower particulate emissions

Reduces dependence on imported LPG

Can also serve as a clean industrial and transport fuel

PYQ Relevance

[UPSC 2017] Access to affordable, reliable, sustainable and modern energy is the sine qua non to achieve Sustainable Development Goals (SDGs). Comment on the progress made in India in this regard

Linkage: The PYQ tests India’s strategy to achieve energy security through indigenous energy resources, cleaner technologies, and sustainable industrial development. The article highlights coal gasification and coal chemistry as indigenous clean-coal technologies that can reduce LPG imports, strengthen energy security, and support India’s transition towards reliable and sustainable energy systems.

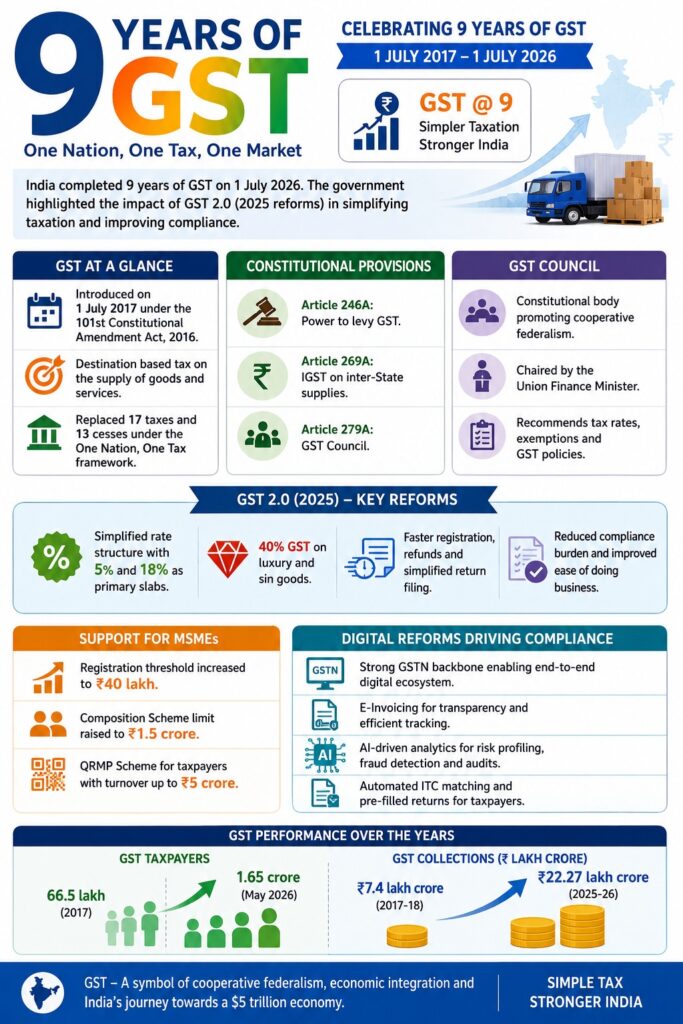

India completed 9 years of GST on 1 July 2026. The government highlighted the impact of GST 2.0 (2025 reforms) in simplifying taxation and improving compliance.

GST at a Glance

Introduced on 1 July 2017 under the 101st Constitutional Amendment Act, 2016.

Destination based tax on the supply of goods and services.

Replaced 17 taxes and 13 cesses under the One Nation, One Tax framework.

Constitutional Provisions

Article 246A: Power to levy GST.

Article 269A: IGST on inter-State supplies.

Article 279A: GST Council.

GST Council

Constitutional body promoting cooperative federalism.

Chaired by the Union Finance Minister.

Recommends tax rates, exemptions and GST policies.

GST 2.0 (2025)

Simplified rate structure with 5% and 18% as primary slabs.

40% GST on luxury and sin goods.

Faster registration, refunds and simplified return filing.

MSME Support

Registration threshold increased to ₹40 lakh.

Composition Scheme limit raised to ₹1.5 crore.

QRMP Scheme for taxpayers with turnover up to ₹5 crore.

[2017] What is/are the most likely advantages of implementing ‘Goods and Services Tax (GST)’? 1. It will replace multiple taxes collected by multiple authorities and will thus create a single market in India. 2. It will drastically reduce the ‘Current Account Deficit’ of India and will enable it to increase its foreign exchange reserves. 3. It will enormously increase the growth and size of economy of India and will enable it to overtake China in the near future. Select the correct answer using the code given below: