Author: B2B

-

Economics of Animal Rearing in India

Economics of Animal Rearing

India’s Position in Global Livestock Economy.

Importance of Livestock sector in the Indian Economy.

Importance of Livestock sector in achieving Inclusive Growth in India

- Distribution of livestock is more equitable than that of land. In 2003 marginal farm households (≤1.0h hectare of land) who comprised 48% of the rural households controlled more than half of country’s cattle and buffalo and two-thirds of small animals and poultry as against 24% of land. Between 1991-92 and 2002-03 their share in land area increased by 9 percentage points and in different livestock species by 10-25 percentage points.

- Livestock has been an important source of livelihood for small farmers. They contributed about 16% to their income, more so in states like Gujarat (24.4%), Haryana (24.2%), Punjab (20.2%) and Bihar (18.7%).

- The agricultural sector engages about 57% of the total working population and about 73% of the rural labour force. Livestock employed 8.8% of the agricultural work force albeit it varied widely from 3% in North-Eastern states to 40-48% in Punjab and Haryana. Animal husbandry promotes gender equity. More than three-fourth of the labour demand in livestock production is met by women. The share of women employment in livestock sector is around 90% in Punjab and Haryana where dairying is a prominent activity and animals are stallfed.

- The distribution patterns of income and employment show that small farm households hold more opportunities in livestock production. The growth in livestock sector is demand-driven, inclusive and pro-poor. Incidence of rural poverty is less in states like Punjab, Haryana, Jammu & Kashmir, Himachal Pradesh, Kerala, Gujarat, and Rajasthan where livestock accounts for a sizeable share of agricultural income as well as employment. Empirical evidence from India as well as from many other developing countries suggests that livestock development has been an important route for the poor households to escape poverty.

Livestock population (2012 Livestock census)

Sl. No Species Number (in millions)

Ranking in the world population 01 Cattle 190.9 Second 02 Buffaloes 108.7 First Total (including Mithun and Yak) 300 First 03 Sheep 65.0 Third 04 Goats 135.2 Second 05 Pigs 10.3 – 06 Others 1.7 – Total livestock 512.3 Total poultry 729.2 Seventh 07 Duck – Fifth

08 Chicken – 09 Camel – Tenth Schemes/Policies Launched for Livestock Sector by the Government

National Livestock Mission

The National Livestock Mission (NLM) has commenced from 2014-15. The Mission is designed to cover all the activities required to ensure quantitative and qualitative improvement in livestock production systems and capacity building of all stakeholders. The Mission will cover everything germane to improvement of livestock productivity and support projects and initiatives required for that purpose subject. This Mission is formulated with the objective of sustainable development of livestock sector, focusing on improving availability of quality feed and fodder. NLM is implemented in all States including Sikkim.

NLM has 4 submissions as follows:

The Sub-Mission on Fodder and Feed Development will address the problems of scarcity of animal feed resources, in order to give a push to the livestock sector making it a competitive enterprise for India, and also to harness its export potential. The major objective is to reduce the deficit to nil.

Under Sub-Mission on Livestock Development, there are provisions for productivity enhancement, entrepreneurship development and employment generation (bankable projects), strengthening of infrastructure of state farms with respect to modernization, automation and biosecurity, conservation of threatened breeds, minor livestock development, rural slaughter houses, fallen animals and livestock insurance.

Sub-Mission on Pig Development in North-Eastern Region: There has been persistent demand from the North Eastern States seeking support for all round development of piggery in the region. For the first time, under NLM a Sub-Mission on Pig Development in North-Eastern Region is provided wherein Government of India would support the State Piggery Farms, and importation of germplasm so that eventually the masses get the benefit as it is linked to livelihood and contributes in providing protein-rich food in 8 States of the NER.

Sub-Mission on Skill Development, Technology Transfer and Extension: The extension machinery at field level for livestock activities is very weak. As a result, farmers are not able to adopt the technologies developed by research institutions. The emergence of new technologies and practices require linkages between stakeholders and this sub-mission will enable a wider outreach to the farmers.All the States, including NER States may avail the benefits of the multiple components and the flexibility of choosing them under NLM for a sustainable livestock development.

Rashtriya Gokul Mission

Key features of the mission

- The Mission aims to conserve and develop indigenous breeds in a focused and scientific manner and for that breeding facilities will be set up for varieties with high-genetic pedigree”. Indigenous cattle are largely ignored in India despite the fact that they are better adapted to the country’s climate”.

- The aim of the mission is to protect Indigenous cow from being cross-bred into different varieties.

- Focus will be largely to give a push to local breeding programme on the line of elite local breeds like Gir, Sahiwal, Rathi to enhance milk production.

- The local cow breed will be protected through traditional-style “gaushalas” or cattle-care centres. • The scheme has provision to acknowledge those farmers who works rigorously in the direction. • The “Gopal Ratna” awards will be conferred to them. • The scheme also makes a point about upkeep of cattle after their milk producing phase gets over and then they often used for the purpose of meat. Official reaction.

- An amount of Rs 500 crore has been earmarked for Bovine Breeding and Dairy Development programme and out of which Rs 150 crore will be specially allocated for the protection of indigenous cow breeds.

Idea behind the Mission?

- The idea is to increase milk production which is dismal in comparison to US, UK, and Israel.

- Though India has attained the numero uno position in milk production but that is only because the country is home of world’s largest livestock population.

- Through the programme, the aim is to increase high yield per cow which is very low in comparison to the European countries like US. Low yield per cow in India

- The average daily milk yield for crossbred cattle in India is at 7.1 kg per day while it is at 25.6 in UK, US (32.8) and Israel (38.6).

- The reason behind the low yield in India is because of intrinsic and extrinsic factors both.

- The intrinsic factor is low genetic potential while extrinsic is related with number of reasons like poor nutrition and feed management, inferior farm management practices and inefficient implementation of breed improvement programs.

- At present, India is largely using Jersey, a native of Netherlands and British origin Holstein for cross-breeding purposes.

Operation flood/ White Revolution in India:

‘Operation flood’ a program started by National Dairy Development Board (NDDB) in 1970 made India the largest producer of the milk in the world. This program with its whopping success was called as ‘The White Revolution’. The main architect of this successful project was Dr. Verghese Kurien, also called the father of White Revolution.

In 1949 Mr. Kurien joined Kaira District Co-operative Milk Producers’ Union (KDCMPUL), now famous as Amul.

Kurien has since then built this organization into one of the largest and most successful institutions in India. The Amul pattern of cooperatives had been so successful, in 1965, then Prime Minister of India, Shri Lal Bahadur Shastri, created the National Dairy Development Board (NDDB) to replicate the program on a nationwide basis citing Kurien’s “extraordinary and dynamic leadership” upon naming him chairman.

Operation Flood Phases

The Operation Flood was completed in three phases:

Phase I (1970-79):- During this phase 18 of the country’s main milk sheds were connected to the consumers of the four metros viz. Mumbai, Delhi, Chennai and Kolkata. The total cost of this phase was Rs.116crores. The main objectives were, commanding share of milk market and speed up development of dairy animals respectively hinter- lands of rural areas.

Phase II (1981–1985):- The management increased the milk sheds from 18 to 136; 290 urban markets expanded the outlets for milk. By the end of 1985, a self-sustaining system of 43,000 village cooperatives with 42.5 lakh milk producers were covered. Domestic milk powder production increased from 22,000 tons in the pre-project year to 140,000 tons by 1989, all of the increase coming from dairies set up under Operation Flood.

Phase III (1985–1996):- The dairy cooperatives were enabled to expand and strengthen the infrastructure required to procure and market increasing volumes of milk. Veterinary first-aid health care services, feed and artificial insemination services for cooperative members were extended, along with intensified member education. It went with adding 30,000 new dairy cooperatives to the 42,000 existing societies organized during Phase II. Milk sheds peaked to 173 in 1988-89 with the numbers of women members and Women’s Dairy Cooperative Societies increasing significantly.

Amul: (“priceless” in Sanskrit. The brand name “Amul,” from the Sanskrit “Amoolya,” formed in 1946, is a dairy cooperative in India.

It is a brand name managed by an apex cooperative organization, Gujarat Co-operative Milk Marketing Federation Ltd. (GCMMF), which today is jointly owned by some 2.8 million milk producers in Gujarat, India. The White Revolution’s model dairy board was that of Amul. The whole program of NDDB was largely based the working of this dairy board. The three-tier ‘Amul Model’ has been instrumental in bringing about the White Revolution in the country.

Achievements of the White Revolution

- The phenomenal growth of milk production in India – from 20 million MT to 100 million MT in a span of just 40 years – has been made possible only because of the dairy cooperative movement. This has propelled India to emerge as the largest milk producing country in the World today.

- The dairy cooperative movement has also encouraged Indian dairy farmers to keep more animals, which has resulted in the 500 million cattle & buffalo population in the country – the largest in the World.

- The dairy cooperative movement has spread across the length and breadth of the country, covering more than 125,000 villages of 180 Districts in 22 States.

- The movement has been successful because of a well-developed procurement system & supportive federal structures at District & State levels.

Blue Revolution in India

Realizing the immense scope for development of fisheries and aquaculture, the Government of India has restructured the Central Plan Scheme under an umbrella of Blue Revolution.

The restructured Central Sector Scheme on Blue Revolution: Integrated Development and Management of Fisheries (CSS) approved by the Government provides for a focused development and management of the fisheries sector to increase both fish production and fish productivity from aquaculture and fisheries resources of the inland and marine fisheries sector including deep sea fishing.

The scheme has the following components:

i. National Fisheries Development Board (NFDB) and its activities.

ii. Development of Inland Fisheries and Aquaculture.

iii. Development of Marine Fisheries, Infrastructure and Post-Harvest Operations.

iv. Strengthening of Database & Geographical Information System of the Fisheries Sector.

v. Institutional Arrangement for Fisheries Sector.

vi. Monitoring, Control and Surveillance (MCS) and other need-based Interventions.

vii. National Scheme on Welfare of Fishermen.The Scheme Blue Revolution: Integrated Development and Management of Fisheries is being implemented in consultation with all States & UTs. Besides the activities undertaken under both the marine and inland sectors, no specific role for the coastal states has been defined.

The Blue Revolution is being implemented to achieve economic prosperity of fishermen and fish farmers and to contribute towards food and nutritional security through optimum utilization of water resources for fisheries development in a sustainable manner, keeping in view the bio-security and environmental concerns.

Under the scheme, it has been targeted to enhance the fish production from 107.95 lakh tonnes in 2015-16 to about 150 lakh tonnes by the end of the financial year 2019-20. It is also expected to augment the export earnings with a focus on increased benefit flow to the fishers and fish farmers to attain the target of doubling their income.

The Department has prepared a detailed National Fisheries Action Plan-2020(NFAP) for the next 5 years with an aim of enhancing fish production and productivity and to achieve the concept of Blue Revolution. The approach was initiated considering the various fisheries resources available in the country like ponds & tanks, wetlands, brackish water, cold water, lakes & reservoirs, rivers and canals and the marine sector.

Challenges faced by the fisheries sector

- Shortage of quality and healthy fish seeds and other critical inputs.

- Lack of resource-specific fishing vessels and reliable resource and updated data.

- Inadequate awareness about nutritional and economic benefits of fish.

- Inadequate extension staff for fisheries and training for fishers and fisheries personnel.

- Absence of standardization and branding of fish products.

The Way Forward

- Schemes of integrated approach for enhancing inland fish production and productivity with forward and backward linkages.

- Large scale adoption of culture-based capture fisheries and cage culture in reservoirs and larger water bodies are to be taken up.

- Sustainable exploitation of marine fishery resources especially deep sea resources and enhancement of marine fish production through sea farming, mariculture.

Poultry Sector in India

Growth of India’s Poultry sector in Recent years

- Indian Poultry Industry is one of the fastest growing segments of the agricultural sector today in India. As the production of agricultural crops has been rising at a rate of 1.5 to 2% per annum while the production of eggs and broilers has been rising at a rate of 8 to 10% per annum. Today India is world’s fifth largest egg producer in the world. Indian broiler production at 3.8 million tons is the fourth largest in the world after US, Brazil and China.

- The broiler growing companies are becoming bigger and the feed mills are getting larger. More than 60 per cent of the feed is being processed. The layer farming with 220 million layers is growing at six to eight per cent and the egg prices are at record high.

- The 67,000-crore Indian poultry industry is expected to report higher margins in the years to come.

- The Indian Poultry Industry has undergone a paradigm shift in structure and operation. A very significant feature of India’s poultry industry is its transformation from a mere backyard activity into a major commercial activity in just about four decades which seems to be really fast. The kind of transformation has involved sizeable investments in breeding, hatching, rearing and processing. Indian farmers have moved from rearing non-descript birds to today’s rearing hybrids such as Hyaline, Shaver, and Babcock which ensure faster growth, good livability, excellent feed conversion and high profits to the rearers.

- The organized sector of Indian Poultry Industry is contributing nearly 70% of the total output and the rest 30% in the unorganized sector.

- Due to the demand for poultry increasing and production reaching 37 billion eggs and 1 billion broilers, the Poultry Industry today employs around 1.6 million people. At least 80% of employment in Indian Poultry Industry generates directly by the farmers, while 20 % is engaged in feed, pharmaceuticals, equipment and other services according to the requirement. Additionally, there might be similar number of people roughly 1.6 million who are engaged in marketing and other channels servicing the poultry sector.

Reason Behind this growth

- The contributing factors behind this growth are – growth in per capita income, a growing urban population and falling poultry prices.

- The Indian Poultry Industry has grown largely due to the initiative of private enterprises, minimal government intervention, and very considerable indigenous poultry genetics capabilities, and support from the complementary veterinary health, poultry feed, poultry equipment, and poultry processing sectors. India is one of the few countries in the world that has put into place a sustained Specific Pathogen Free (SPF) egg production project.

Challenges the Poultry sector is facing

- In last 2 years the Poultry sector is facing distress due to number of factors

- There is disparity between states and hence an impairment in growth of the sector. About 60% of the egg production comes from Andhra Pradesh. Commercial poultry farming yet to make a mark in states like Odisha, Bihar, MP, Rajasthan. This disparity has resulted in uncertainty in sector.

- Recent heatwaves in Andhra Pradesh and Telangana region has resulted in high chicken prices due to killing of birds. As a result, poultry feed demand has fallen.

- Avian influenza was another issue which has resulted which has devastating effect on Indian poultry, and it still continues to haunt the sector due to low demand and less exports

- Shortage of raw material is another issue. Price of soybean meal, the major and only source of protein has increased about 75%, which has forced the feed manufacturers to comprise in terms of diet given to birds.

- Shortage of human resources is another problem because of the absence of veterinarians, researchers, in areas where expertise knowledge is required.

- Indian poultry sector is still unable to tap the benefit of international market. Lack of adequate cold storage, warehouses is the major factor affecting poultry sector in India.

- Majority of the production is by unorganized which is another threat faced by sector.

- Usually, summer sees a production drop of five to 10 per cent; this year, with the heat and drought, there is a 25-30 per cent drop. The drought has hit water supply for the birds and the latter’s mortality rate has risen in recent months, pushing up prices for broilers and eggs.

Way Forward

The Following measures should be taken by the Government to improve the situation.

- Strong marketing network to set the industry free from the clutches of middlemen.

- Government support to public poultry educational and R&D institutions.

- Building infrastructure to meet the growing manpower demand of the poultry sector.

- Promote both mass production as well as production by masses.

- Support and promotion of the processing sector.

- Insurance against losses.

- Provision of subsidies, and credit

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Food processing and related industries in India- scope and significance, location, upstream and downstream requirements, supply chain management.

- Food Processing Industry: Definition and Dimensions; Channels of Transitions; Inter linkages between Agriculture and Industry.

- Food Processing Industry: Food Based Industry versus Non- Food Based; Location, Upstream, Downstream Requirements.

- Food Processing Industry: Forward, Backward Linkages; Food Processing Industry and Economic Development

- Food Processing Industry in India: Growth Drivers, FDI Policy, Investment Opportunities; Schemes Related to Food Processing Sector.

- Supply Chain Management in Indian Agriculture

-

Supply Chain Management in Indian Agriculture

Supply Chain Management in Indian Agriculture

Definition:

“Supply chain means flow & movement of goods from the producers to the final consumers”.

Supply Chain is a sequence of flows that aim to meet final customer requirements, that take place within and between different stages along a continuum, from production to final consumption.

The Supply Chain not only includes the producer and its suppliers, but also, depending on the logistic flows, transporters, warehouses, retailers, and consumers themselves. In a broader sense, supply chains also includes, new product development, marketing, operations, distribution, finance and customer service.

A Graphical Presentation of Supply Chain

Supply Chain Management: The term ‘Supply Chain Management’ is relatively new. It first appeared in logistics literature in the 1980s, as an inventory management approach with emphasis on the supply of raw materials. Logistics managers in retail, grocery, and other high inventory industries began to realize that a significant competitive advantage could be derived through the management of materials that flow in their ‘inbound’ and ‘outbound’ channels.

Supply Chain Management involves following processes:

- Integrated Planning

- Implementation

- Coordination

- Control

Therefore, SCM is the integrated planning, implementation, coordination and control of all Agri-business processes and activities necessary to produce and deliver, as efficiently as possible, products that satisfies consumer preferences and requirements.

Contrasting Supply Chain Management with Traditional Management Chain

Element Traditional Management Supply Chain Management Inventory management approach Independent Efforts. Joint reduction in channel inventories. Total cost approach Minimize firm costs Channel-wide cost efficiencies Time horizon Short-term Long-term Amount of information sharing and monitoring Limited to needs of own current transactions As required for planning and monitoring purposes Amount of coordination of multiple levels in the channel Single contact for the transaction between channel pairs Multiple contacts between levels in firms and levels of channel Joint planning Transaction-based On-going Breadth of supplier base Large to increase competition and spread risk Small to increase coordination Channel leadership Not needed Needed for coordination focus Speed of operations, information and inventory flows ‘Warehouse’ orientation (storage, safety stock). Interrupted by barriers to flows. Localized to channel pairs ‘Distribution Centre’ orientation (focus on turnover speed). Interconnecting flows; JIT, Quick Response across the channel Agriculture Supply Chain Networks

An agriculture supply chain system comprises organizations/cooperatives that are responsible for the production and distribution of vegetable/Fruits/Cereals/Pulses or animal-based products. In general, we distinguish two main types:

- ‘Agriculture food supply chains for fresh agricultural products’ (such as fresh vegetables, flowers, fruit). In general, these chains may comprise growers, auctions, wholesalers, importers and exporters, retailers and speciality shops and their input and service suppliers. Basically, all of these stages leave the intrinsic characteristics of the product grown or produced untouched. The main processes are the handling, conditioned storing, packing, transportation and especially trading of these goods.

- ‘Agriculture food supply chains for processed food products’ (such as portioned meats, snacks, juices, desserts, canned food products). In these chains, agricultural products are used as raw materials for producing consumer products with higher added value. In most cases, conservation and conditioning processes extend the shelf-life of the products.

Issues Related to Agriculture Supply Chains

Participants in Agriculture supply chains, e.g. farmers, traders, processors, retailers, etc, understand that original good quality products can be subject to quality decay because of an inadequate action of another participant.

For example, when a farm leaves a can of milk for pick-up on a roadside, under the sun, without any cover, there will be a loss of quality that may even render the raw material unfit for processing.

Similarly, if processors, on the other hand, use packaging items and/or technologies that do not maintain freshness and nutritional characteristics of their products as much as possible, retailers will be likely to face customer complaints.

Characteristics of Agriculture Supply Chains and its impact on Logistics

Supply Chain Stage Issues with Product & Process Characteristics Impact on Logistic/Flow of goods. Overall Shelf-life constraints for raw materials, intermediates and finished products and changes in product quality level while progressing the supply chain (decay). Recycling of Materials Required.

• Timing constraints (goods have to be supplied quickly to avoid decay). • Information requirements (correct information of goods is essential).

Growers / Producers • Long production times (producing new or additional agro-products takes a lot of time) • Seasonality in production • Variability of quality and quantity of supply

• Responsiveness • Flexibility in process and planning

Food processing industry • High volume, low variety (although the variety is increasing) production systems • Highly sophisticated capital-intensive machinery leading to the need to maintain capacity utilization

• Variable process yield in quantity and quality due to biological variations, seasonality, random factors connected with weather, pests, other biological hazards

• A possible necessity to wait for the results of quality tests

• Alternative installations, alternative recipes, product-dependent cleaning and processing times, carry over of raw materials between successive product lots, etc.

• Storage buffer capacity is restricted, when material, intermediates or finished products can only be kept in special tanks or containers

• Necessity to value all parts because of the complementary nature of agricultural inputs (for example, beef cannot be produced without the co-product hides)

• Necessity for lot traceability of work in process due to quality and environmental requirements and product responsibility

• Importance of production planning and scheduling focusing on high capacity utilization • Flexibility of recipes

• Timing constraints, ICT possibility to confine products

• Flexible production planning that can handle this complexity

• Need for configurations that facilitate tracking and tracing

Auctions / Wholesalers/ Retailers • Variability of quality and quantity of supply of farm-based inputs • Seasonal supply of products requires global (year-round) sourcing

• Requirements for conditioned transportation and storage means

• Pricing issues • Timing constraints

• Need for conditioning

• Pre-information on quality status of products

Issues Related to Supply Chain Management in India

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Food Processing Industry in India: Growth Drivers, FDI Policy, Investment Opportunities; Schemes Related to Food Processing Sector.

Food Processing Industry in India:

A Snapshot

- The Indian food industry is poised for huge growth, increasing its contribution to world food trade every year.

- In India, the food sector has emerged as a high-growth and high-profit sector due to its immense potential for value addition, particularly within the food processing industry.

- Accounting for about 32 per cent of the country’s total food market, The Government of India has been instrumental in the growth and development of the food processing industry.

- The government through the Ministry of Food Processing Industries (MoFPI) is making all efforts to encourage investments in the business.

- It has approved proposals for joint ventures (JV), foreign collaborations, industrial licenses, and 100 per cent export oriented units.

- Food processing industry in India is a sunrise sector that has gained prominence in the recent years. Availability of raw materials, changing lifestyles and appropriate fiscal policies has given a considerable push to the industry’s growth.

- This sector serves as a vital link between the agriculture and industrial segments of the economy. Strengthening this link is of critical importance to reduce waste of agricultural raw materials, improve the value of agricultural produce by increasing shelf-life as well as by fortifying the nutritive capacity of the food products; ensure remunerative prices to farmers as well as affordable prices to consumers.

- Adequate focus on this sector could greatly alleviate our concerns on food security and food inflation.

- India already is a leading exporter of several food products. To ensure that this sector gets the stimulus it deserves, Ministry of Food Processing Industries is implementing a number of schemes for Infrastructure development, technology up-gradation & modernization, human resources development and R&D in the Food Processing Sector.

The Ministry of Food Processing Industry defines Food Processing to include under food processing industries, items pertaining to these two processes viz

(a) Manufactured Processes: If any raw product of agriculture, animal husbandry or fisheries is transformed through a process [involving employees, power, machines or money] in such a way that its original physical properties undergo a change and if the transformed product is edible and has commercial value, then it comes within the domain of Food Processing Industries.

(b) Other Value-Added Processes: Hence, if there is significant value addition (increased shelf life, shelled and ready for consumption etc.) such produce also comes under food processing, even if it does not undergo manufacturing processes.

The Growth of Food Processing Industry in India

As seen in the graph above, the contribution of food processing sector to GDP has been growing faster than that of the agriculture sector.

If the contribution to GDP of both agricultural sector and food processing sector were growing at the same rate, then it would mean that the growth in food processing sector is only due to increased agricultural raw material supply.

However, what this graph indicates is that more and more agricultural products are being converted (in value terms) to food products. This means that the level of processing in value terms has been increasing in India.

Person Employed by the Food Processing Industries

Food Processing Industry is one of the major employment intensive segments constituting 12.13 per cent of employment generated in all Registered Factory sector in 2011- 12.

According to the latest Annual Survey of Industries (ASI) for 2011-12, the total number of persons engaged in registered food processing sector is 17.77 lakhs.

During the last 5 years ending 2011-12, employment in registered food processing sector has been increasing at an Annual Average Growth Rate of 3.79 per cent. Unregistered food processing sector supports employment to 47.9 lakh workers as per the NSSO 67thRound, 2010-11.

Export Performance of the Food Processing Sector

All agricultural produce when exported undergo an element of processing. Hence all edible agricultural commodities exported are included in the export data. The value of exports in the sector has been showing an increasing trend with Average Annual Growth Rate (AAGR) of 20.53 per cent for five years ending 2013-14.

The value of processed food exports during 2013-14 was of the order of US $ 37.79 Billion (total exports US $ 312 Billion) constituting 12.1 per cent of India’s total exports.

Food Processing Industry in India: Growth Drivers, FDI Policy, Investment Opportunities

Growth Drivers

Factors Contributing to Growth of the Food Processing Sector.

FDI Policy

Schemes Related to Food Processing Sector in India

Pradhan Mantri Kisan Sampada Yojana

- PM Kisan SAMPADA Yojana is a comprehensive package which will result in creation of modern infrastructure with efficient supply chain management from farm gate to retail outlet.

- It will not only provide a big boost to the growth of food processing sector in the country but also help in providing better process to farmers and is a big step towards doubling of farmers income, creating huge employment opportunities especially in the rural areas, reducing wastage of agricultural produce, increasing the processing level and enhancing the export of the processed foods.

Mega Food Parks

- The Scheme of Mega Food Park aims at providing a mechanism to link agricultural production to the market by bringing together farmers, processors and retailers so as to ensure maximizing value addition, minimizing wastage, increasing farmers’ income and creating employment opportunities particularly in rural sector.

- The Mega Food Park Scheme is based on “Cluster” approach and envisages creation of state of art support infrastructure in a well-defined agri/ horticultural zone for setting up of modern food processing units along with well-established supply chain.

- Mega food park typically consists of supply chain infrastructure including collection centers, primary processing centers, central processing centers, cold chain and around 30-35 fully developed plots for entrepreneurs to set up food processing units.

- The Mega Food Park project is implemented by a Special Purpose Vehicle (SPV) which is a Body Corporate registered under the Companies Act. However, State Government, State Government entities and Cooperatives are not required to form a separate SPV for implementation of Mega Food Park project. Subject to fulfillment of the conditions of the Scheme Guidelines, the funds are released to the SPVs.

- So far Nine Mega Food Parks, namely, Patanjali Food and Herbal Park, Haridwar, Srini Food Park, Chittoor, North East Mega Food Park, Nalbari, International Mega Food Park, Fazilka, Integrated Food Park,Tumkur, Jharkhand Mega Food Park, Ranchi, Indus Mega Food Park, Khargoan, Jangipur Bengal Mega Food Park, Murshidabad and MITS Mega Food Park Pvt Ltd, Rayagada are functional .

Integrated Cold Chains and Value Addition Infrastructure

- The objective of the Scheme of Cold Chain, Value Addition and Preservation Infrastructure is to provide integrated cold chain and preservation infrastructure facilities, without any break, from the farm gate to the consumer.

- It covers pre-cooling facilities at production sites, reefer vans, mobile cooling units as well as value addition centres which include infrastructural facilities like Processing/ Multi-line Processing/ Collection Centres, etc. for horticulture, organic produce, marine, dairy, meat and poultry etc.

- The integrated cold chain project is set up by Partnership/ Proprietorship Firms, Companies, Corporations, Cooperatives, Self Help Groups (SHGs), Farmer Producer Organizations (FPOs), NGOs, Central/ State PSUs, etc. subject to fulfilment of eligibility conditions of scheme guidelines.

Schemes for Creation/Expansion of Food Processing/Processing Facilities

- The main objective of the Scheme is creation of processing and preservation capacities and modernisation/ expansion of existing food processing units with a view to increasing the level of processing, value addition leading to reduction of wastage.

- The setting up of new units and modernization/ expansion of existing units are covered under the scheme. The processing units undertake a wide range of processing activities depending on the processing sectors which results in value addition and/ or enhancing shelf life of the processed products.

- Scheme is implemented through organizations such as Central & State PSUs/ Joint Ventures/ Farmer Producers Organization (FPOs)/ NGOs/ Cooperatives/ SHG’s/ Pvt. Ltd companies/ individuals proprietorship firms engaged in establishment/ upgradation/ modernization of food processing units. Proposals under the scheme are invited through Expression of Interest (EOI) and Project Management Agencies (PMA) are engaged by MOFPI to assist in the implementation of the scheme.

Agro Processing Clusters:

- The scheme aims at development of modern infrastructure and common facilities to encourage group of entrepreneurs to set up food processing units based on cluster approach. Under the scheme, effective backward and forward linkages are created by linking groups of producers/ farmers to the processors and markets through well-equipped supply chain consisting of modern infrastructure for food processing closer to production areas and provision of integrated/ complete preservation infrastructure facilities from the farm gate to the consumer.

- Each clusters have two basic components i.e. Basic Enabling Infrastructure (roads, water supply, power supply, drainage, ETP etc.), Core Infrastructure/ Common facilities (ware houses, cold storages, IQF, tetra pack, sorting, grading etc) and at least 5 food processing units with a minimum investment of Rs. 25 crore. The units are set up simultaneous along with creation of common infrastructure.

- The Project Execution Agency (PEA) which is responsible for overall implementation of the projects undertakes various activities including formulation of the Detailed Project Report (DPR), procurement/ purchase of land, arranging finance, creating infrastructure, ensuring external infrastructure linkages for the project etc. PEA may sell/ lease plots in agro-processing cluster to other food processing units but the common facilities in the cluster cannot be sold or leased out.

Scheme for Creation of Backward and Forward Linkages

- The objective of the scheme is to provide effective and seamless backward and forward integration for processed food industry by plugging the gaps in supply chain in terms of availability of raw material and linkages with the market. Under the scheme, financial assistance is provided for setting up of primary processing centers/ collection centers at farm gate and modern retail outlets at the front end along with connectivity through insulated/ refrigerated transport.

- The Scheme is applicable to perishable horticulture and non-horticulture produce such as, fruits, vegetables, dairy products, meat, poultry, fish, Ready to Cook Food Products, Honey, Coconut, Spices, Mushroom, Retails Shops for Perishable Food Products etc.

- The Scheme would enable linking of farmers to processors and the market for ensuring remunerative prices for agri produce.

Food Safety and Quality Assurance Infrastructure

- Quality and Food Safety have become competitive edge in the global market for food products. For the all-around development of the food processing sector in the country, various aspect of Total Quality Management (TQM) such as quality control, quality system and quality assurance should operate in a horizontal fashion.

- Apart from this, in the interest of consumer safety and public health, there is a need to ensure that the quality food products manufactured and sold in the market meet the stringent parameters prescribed by the food safety regulator.

- Keeping in view the aforesaid objectives, government has been extending financial assistance under the scheme under the following components:

- Setting up and upgradation of quality control/Food Testing Laboratories.

- HACCP/ISO Standards/Food Safety/Quality Management System

National Mission on food processing:

- Ministry of Food Processing Industries (MOFPI) implemented a new Centrally Sponsored Scheme (CSS) National Mission on Food Processing (NMFP) on 1st April 2012 for implementation through States/UTs.

- The NMFP visualizes establishment of a National Mission as well as corresponding Missions in the State and District level. The major objectives of this schemes are as follows:

- To augment the capacity of food processors working to upscale their operations through capital infusion, technology transfer, skill up gradation and handholding support.

- To support established self-help groups working in food processing sector to facilitate them to achieve SME status.

- Capacity development and skill upgradation through institutional training to ensure sustainable employment opportunities to the people and also to reduce the gap in requirement and availability of skilled manpower in food processing sector.

- To raise the standards of food safety and hygiene to the globally accepted norms.

- To facilitate food processing industries to adopt HACCP and ISO certification norms

- To augment farm gate infrastructure, supply chain logistic, storage and processing capacity.

- To provide better support system to organized food processing sector

Major Programs / Schemes to be covered under NMFP during 2012-13 are;

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Food Processing Industry: Forward, Backward Linkages; Food Processing Industry and Economic Development

Food Processing Industry: Scope, Importance & Significance in Economic Development

The Economic Linkage Effects of Food Processing Industry

Linkages is a phenomenon which measures the capability of an industry to generate demand for the products of the other industries. Form the point of view of development strategy, linkages are one of the essential feature of an industry. Linkages are of three types: Forward, Backward and sideways.

Forward Linkage: It is when, the establishment of a processing industry can lead to the development and establishment of the number of advanced stage industries. Example, Forest Industry, when established as a base industry, results in establishment of vast number of advanced processing industries like: manufacturing of paper, paper bags, stationary, boxes made of paper, cartons, wooden boxes etc.

There are many other examples: products such as vegetable oils and rubber are used in a wide variety of manufacturing industries; based on the preparation of hides and skins, tanning operations can be started, as can the manufacture of footwear and other leather goods.

Backward Linkage: The feedback effects generated by a base industry on the development of the base sector is called backward linkage. The development of the food processing industry has many feed back effects on the agriculture sector itself.

For Example, once a food processing industry is established, it results in increasing the demand of raw materials provided by the agriculture sector. The establishment of processing facilities is itself an essential first step towards stimulating both consumer demand for the processed product and an adequate supply of the raw material.

The provision of transport, power and other infra-structural facilities required for agro-industries also benefits agricultural production. The development of these and other industries provides a more favourable atmosphere for technical progress and the acceptance of new ideas in farming itself.

Sideways Linkage: Sideways linkages are mostly derived from the use of by products and waste products of the main base industrial activity. For example: many food processing industries using agriculture raw materials produce waste that can be used further in production of fuel, bio-fuels, paper pulp and fertilizer. The production of sugar results in production of molasses as a waste product, which is used by the Alcohol Brewing industry in the production of ethanol.

The capacity of Food Processing industry to generate demand and employment in other industries is the important aspect of the processing industry. It works because of processing industry growing potential for activating backward, forward and sideway linkages.

The Food Processing Industry and Economic Development

Backward Channel

Forward Channel.

The growth of Food Processing Industry at different stages of Development.

The Initial Stage/Less Developed Countries

The Intermediate Stage/Middle Income Countries

The More Advanced Middle-Income Stage

The Final Stage/Developed Countries

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Food Processing Industry: Food Based Industry versus Non- Food Based; Location, Upstream, Downstream Requirements.

Food Processing Industry: Location, Upstream, Downstream Requirements

Food Based Agro-processing Industry versus Non- Food Based Agro-Processing Industry

Upstream versus Downstream Food Processing Industries.

Potential for Food Processing Industry in India

Advantages of the Food Processing Industries

Factors Determining Location of Food Processing Industries

There are, however, few exceptions:

- For most grains (cereals), shipment of the raw material in bulk is frequently easier, while many bakery products are highly perishable and thus require production to be located close to the market.

- Oilseeds (except for the more perishable ones such as olives and palm fruit) are also an exception and can be transported equally easily and cheaply in raw form or as oil, cake or meal, so there is more technical freedom of choice in the location of processing.

- The same is true for the later stages of processing of some commodities. For example, while raw cotton loses weight in ginning, which is consequently carried out in the producing area, yarn, textiles and clothing can all be transported equally easily and cheaply.

Technical and Exports Considerations in deciding location

- Where there is a high degree of technical freedom in the choice of location, industries have frequently tended to be located in proximity to the markets because of the more efficient labour supply, better infrastructure and lower distribution costs in the large market centres.

- With production for export, this factor has often tended to favour the location of processing in the importing country. This tendency has been reinforced by other factors, including the need for additional raw materials and auxiliary materials (particularly chemicals) that may not be readily available in the raw material-producing country; the greater flexibility in deciding the type of processing according to the end use for which the product is required; and the greater regularity of supply and continuity of operations that are possible when raw materials are drawn from several different parts of the world.

- However, with improved infrastructure, enhanced labour efficiency and growing domestic markets in the developing countries, there is increased potential for expanding such processing in the countries where the raw materials are produced.

- In addition, with growing liberalization of world trade, more developing countries will be able to take advantage of lower labour costs to expand their exports of agro-industrial products.

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Food Processing Industry: Definition and Dimensions; Channels of Transitions; Inter linkages between Agriculture and Industry.

Food Processing Industry in India

Food Processing Industry: Definition and Dimensions

Understanding the Channels of Transitions

Food Economy and Industrial sector have traditionally been viewed as two separate sectors of the economy. They differ both in terms of their characteristics (role in economic growth, share in GDP, share in total output, role in poverty reduction etc.) and potential to generate employment.

The Food sector or Agriculture is considered to be a traditional sector of the economy. Agriculture has been considered the hallmark of First stage development with features like:

The Industrial sector is considered to be a modern sector of the economy and represents the second and most important stage of development. The Industrial sector has modern features like:

The Transition from Agriculture to Industry:

- Over the years, with the development of the economy, the traditional agriculture sector becomes less and less productive due to disguised employment (large no of people working on a small land without contributing to production increase).

- At this Juncture, the agriculture sector with excess supply of labour will start supplying labour force to the Industries and manufacturing sector.

- The disguised labour employed in the agriculture sector will become more productive in the factories, where they will contribute in Increasing production.

- At the same time, the remaining labour force in the agriculture sector will also become more productive (no of people are working is equal to no of people required) and their wages will increase.

- This is how a standard economy makes transition from low productive agriculture sector to high productive industrial sector. The degree of this transition and Industrialisation has been taken to be the most important indicator of a country’s progress along the development path.

The New literature on Changing Role & Interlinkages between Agriculture and Industry

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University -

Investment Models

- Investment Models: Public Sector Led Investment Model; Private Sector Led Investment Model

- Public-Private Partnership Model: Definitions; Need for PPP; Prerequisites.

- Public Private Partnership Models: Contracting, Build Operate Transfer, Design Build Finance Operate (DBFO), Concessions, Build Operate Transfer, EPC Model, Swiss Challenge Model, HAM Model.

-

Public Private Partnership Models: Contracting, Build Operate Transfer, Design Build Finance Operate (DBFO), Concessions, Build Operate Transfer, EPC Model, Swiss Challenge Model, HAM Model.

Public Private Partnership Models

PPP Model: Contracting

PPP Model: Build Operate Transfer

PPP Model: Design Build Finance Operate (DBFO) Concessions

PPP Model: Concessions

PPP Model: Private ownership of Asset

The private sector remains responsible for design, construction and operation of an infrastructure facility and in some cases the public sector may relinquish the right of ownership of assets to the private sector.

Three main types of PPP models with private ownership of assets:

Model: Build Operate Transfer.

The private sector builds, owns and operates a facility, and sells the product/service to its users or beneficiaries. This is the most common form of private participation in the power sector in many countries (examples are numerous).

For a BOO power project, the Government (or a power distribution company) may or may not have a long-term power purchase agreement (commonly known as off-take agreement) at an agreed price from the project operator.

In many respects, licensing may be considered as a variant of the BOO model of private participation. The Government grants licences to private undertakings to provide services such as fixed line and mobile telephony, Internet service, television and radio broadcast, public transport, and catering services on the railways. However, licensing may also be considered as a form of “concession” with private ownership of assets. Licensing allows competitive pressure in the market by allowing multiple operators, such as in mobile telephony, to provide competing services.

Why BOO may be beneficial?

- It is argued that by aggregating design, construction and operation of infrastructure services into one contract, important benefits could be achieved through creation of synergies.

- As the same entity builds and operates the services, and is only paid for the successful supply of services at a pre-defined standard, it has no incentive to reduce the quality or quantity of services.

- Compared with the traditional public sector procurement model, where design, construction and operation aspects are usually separated, this form of contractual agreement reduces the risks of cost overruns during the design and construction phases or of choosing an inefficient technology, since the operator’s future earnings depend on controlling costs.

- The public sector’s main advantages lie in the relief from bearing the costs of design and construction, the transfer of certain risks to the private sector and the promise of better project design, construction and operation.

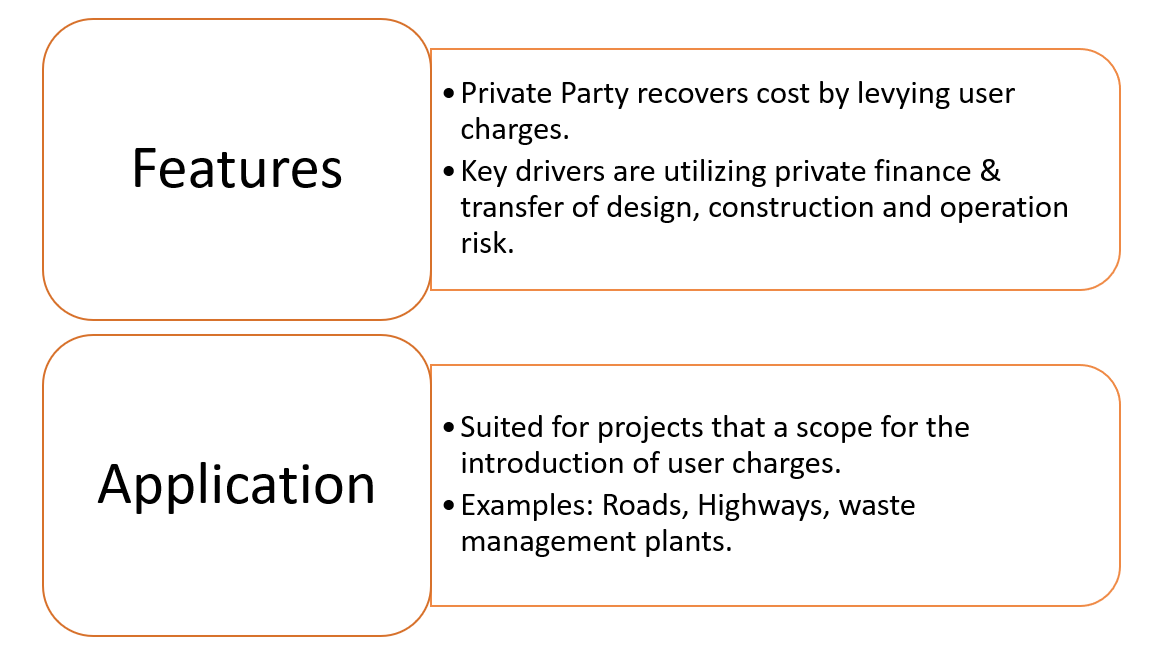

Private Finance Initiative (PFI) model:

In this model, the private sector similar to the BOO model builds, owns and operates a facility. However, the public sector (unlike the users in a BOO model) purchases the services from the private sector through a long-term agreement.

PFI projects therefore, bear direct financial obligations to the government in any event. In addition, explicit and implicit contingent liabilities may also arise due to loan guarantees provided to lenders and default of a public or private entity on non-guaranteed loans.

In the PFI model, asset ownership at the end of the contract period may or may not be transferred to the public sector. The PFI model also has many variants.

Divestiture Model:

In this form a private entity buys an equity stake in a state-owned enterprise. However, the private stake may or may not imply private management of the enterprise. True privatization, however, involves a transfer of deed of title from the public sector to a private undertaking. This may be done either through outright sale or through public floatation of shares of a previously corporatized state enterprise.

Major Issues in PPP Development.

Risk is inherent in all PPP projects as in any other infrastructure projects. The main types of risks include:

Recent Advancements in PPP Models

EPC MODEL: Engineering, Procurement and Construction.

EPC is a popular model being adopted globally in many projects like road construction, roof-top solar projects, etc. Before government chose EPC over PPP in 2014, road construction rate had dwindled significantly to around just 3km per day.

Problems faced by private Players under PPP(BOT) leading to inefficient implementation:

- Delay in land acquisition by the govt and institutional clearances like forest clearance, defence land handovers hampered pace of construction.

- Under PPP, capital completely or partly was to be raised by private player through issuing private equity bonds and borrowing from banks. But –

- Due to delayed implementation, private players weren’t able to pay back loan in time adding to NPA in banks, eventually instigating many banks to stop lending loans

- Delayed implementation also affected fund raising through private equities as they couldn’t find investors for new ventures

- Another area where private players faced difficulty was in assessing the traffic on roads and subsequent designing of roads.

- Due to Above mentioned problems the balance sheets of builders were over stretched and thus forced them to exit projects.

Highway sector in India is responsible for job creation for millions of people and has a multiplier effect on the economy. Hence government took immediate measures to boost the sector by adopting EPC Model and the acronym stands for Engineering, Procurement and Construction.

How is EPC different and better than PPP?

- Govt here bears the entire financial burden and funds the project. Capital is either raised by issuing bonds like NHAI bonds or by taking steps to secure road toll receivables post construction. Note that the fund here is not raised through banks.

- Govt now takes care of clearances, acquiring land and estimating the traffic a very huge exercise that had to be done by private parties earlier.

- With decreased risk on private builders and increased incentives for early road construction, it creates comfortable base to lure investors to carry on the EPC work i.e. the contractor now designs the installation, procures the necessary materials and builds the project, either directly or by subcontracting part of the work.

- Timeline required to construct reduces remarkably.

- In a nutshell, while the government takes responsibility of raising capital, procuring clearances and such, the private builder constructs roads. Thus, significant surge in road construction pace is expected.

Recent decision of NDA govt in Mar 2016 to develop, operate and maintain the wayside amenities alongside National highways across India through EPC model is another example for an EPC project.

HAM MODEL

What is Hybrid annuity model?

- HAM is a Combination of EPC model and BOT-Annuity model. Under this model. The government will provide 40 percent of the project cost to the developer to start work while the remaining investment has to be made by the developer.

Why do we require HAM?

- Most of the earliest highway projects allocated through PPP mode were implemented through BOT –TOLL MODE. under this model the private party is selected to build, maintain and operate the road based on the fact that which private bidder offered maximum sharing of toll revenue to the government. Here, all the risks- land acquisition and compensation risk, construction risk (i.e risk associated with cost of project), traffic risk and commercial risk lies with the private party. The private party is dependent on toll for its revenues. The government is only responsible for regulatory clearances.

- To reduce the risk for private player, and to attract private players, The second model of PPP i.e. BOT-ANNUITY model was introduced under which the private player would built, maintain and operate the Project and government would pay the private player annually fixed amount of annuity. Though it was a better model than BOT-TOLL because it reduced traffic and commercial risk however cost risk remained as private player was solely responsible for the cost incurred in the project.

- In last few years many of the highway projects were stuck due to various reasons like Loss of promoter’s interest, Land acquisition issue, environmental reasons, excessive and unrealistic bidding by the private players and Lack of fund availability for private players due to high NPAs of the banks and lack of long term financing options in India.

- To counter this and to remove the deficiencies of government brought in EPC model. EPC stands for engineering, procurement and construction. It is a model of contract b/w the government and private contractor. The EPC entails the contractor build the project by designing, installing and procuring necessary labour and land to construct the infrastructure, either directly or by subcontracting. Under this system the entire project is funded by the government rather than the PPP model where there is cost sharing. The project is awarded via bidding. Thus, it shifts all the risk from the private players to the government and is the other extreme of BOT model where all risk was borne by the private player

Key features Of HAM MODEL

- Under this the government will pay 40 per cent of the project cost to the concessionaire during the construction phase in five equal installments of 8 per cent each.

- . Revenue collection would be the responsibility of the National Highways Authority of India (NHAI); developers will be paid in annual instilments over a specified period of time.

- An important feature of the hybrid annuity model is allocation of risks between the partners—the government and the developer/investor. While the private partner continues to bear the construction and maintenance risks as in BOT (toll) projects, it is required only to partly bear the financing risk. The developer is insulated from revenue/traffic risk and inflation risk, which are not within its control.

- In the hybrid annuity model, one need not bring 100 per cent of finance upfront and since 40 per cent is available during the construction period, only 60 per cent is required to be arranged for the long term. This makes it attractive and viable for the private player to invest in Highway projects. It also reduces burden on the Government as unlike EPC, the government has to provide only 40% of the project cost.

Conclusion

- By adopting the Model as the mode of delivery, all major stakeholders in the PPP arrangement – the Authority, lender and the developer, concessionaire would have an increased comfort level resulting in revival of the sector through renewed interest of private developers/investors in highway projects and this will bring relief thereby to citizens / travelers in the area of a respective project.It will facilitate uplifting the socio-economic condition of the entire nation due to increased connectivity across the length and breadth of the country leading to enhanced economic activity.

Swiss Challenge Model

What is Swiss Challenge model?

A ‘Swiss Challenge’ is a way to award a project to a private player on an unsolicited proposal. Such projects may not be in the bouquet of projects planned by the state or a state-owned agency, but are considered given the gaps in physical or social infrastructure that they propose to fill, and the innovation and enterprise that private players bring.

The government may enter into direct negotiations with a private player who submits a proposal and, if they cannot agree on the terms of the project, consider calling for bids from other interested players. In one variant of the Challenge, the government awards bonus points to the project’s ideate; in another, it calls for comparative bids, but gives the first right of refusal to the original player. All this is generally disclosed upfront.

Swiss Challenge model in India

At least half-a-dozen states have used the Swiss Challenge to award projects in sectors including IT, ports, power and health. Gujarat included it in the Gujarat Infrastructure Development Act, 1999, and in 2006, amended the Act to provide for direct negotiation. It was subsequently made part of the Andhra Pradesh Infrastructure Development Enabling Act and Punjab Infrastructure (Development & Regulation) Act. Rajasthan and Madhya Pradesh have included it in their guidelines for infra projects. At the central level, the Draft Public Private Partnership Rules, 2011, allow the Swiss Challenge only in exceptional circumstances — that too in projects that provide facilities to predominantly rural areas or to BPL populations.

What are the advantages?

Globally, there aren’t too many good examples of Swiss Challenge projects. South Africa, Chile, Korea, Indonesia, the Philippines and Taiwan have seriously considered, awarded and implemented unsolicited projects. The obvious advantages are that it cuts red tape and shortens timelines, and promotes enterprise by rewarding the private sector for its ideas. The private sector brings innovation, technology and uniqueness to a project, and an element of competition can be introduced by modifying the Challenge.

And what are the problems?

The biggest concerns are the lack of transparency and competition while dealing with unsolicited proposals. Governments need to have a strong legal and regulatory framework to award projects under the Swiss Challenge method. It can potentially foster crony capitalism, and allow companies space to employ dubious means to bag projects. Given that governments sometimes lack an understanding of risks involved in a project, direct negotiations with private players can be fraught with downsides. In general, competitive bidding is the best method to get the most value on public-private partnership projects. The government might also end up granting significant concessions in the nature of viability gap funding, commercial exploitation of real estate, etc., without necessarily deriving durable and long-term social or economic benefits.

Is the Swiss Challenge suited to India?

The jury is still out on the success of public-private partnership (PPP) in infra projects. There have been several controversies around large scale PPP projects. Construction costs jumped significantly in the case of the Mumbai Metro, and then Chief Minister Prithviraj Chavan did some loud thinking on whether the government should take over the company promoted by Anil Ambani after it sought a threefold increase in fares just before commencement last year. There were serious issues related to the international airport and the Airport Metro line in Delhi. The government has now brought PPP projects under the ambit of the CAG, so there is some scrutiny of projects where significant concessions including land at subsidised rates, real estate space, viability gap funding, etc. are granted by the government. But there is still no strong legal framework at the national level, and such projects may be challenged in case of a lack of transparency or poor disclosures. Bureaucrats, who ultimately sign off on such projects, continue to be afraid to take calls that might face an investigation later. In the absence of transparency, and a strong element of competition, such projects may be prone to legal challenges. Smaller projects are better off in this respect.

Government of India Initiatives for Revamping of PPP Models.

Viability Gap Funding.

Viability Gap Funding (VGF) Means a grant one-time or deferred, provided to support infrastructure projects that are economically justified but fall short of financial viability. The lack of financial viability usually arises from long gestation periods and the inability to increase user charges to commercial levels. Infrastructure projects also involve externalities that are not adequately captured in direct financial returns to the project sponsor. Through the provision of a catalytic grant assistance of the capital costs, several projects may become bankable and help mobilise private investment in infrastructure.

Government of India has notified a scheme for Viability Gap Funding to infrastructure projects that are to be undertaken through Public Private Partnerships. It will be a Plan Scheme to be administered by the Ministry of Finance with suitable budgetary provisions to be made in the Annual Plans on a year-to- year basis.

The quantum of VGF provided under this scheme is in the form of a capital grant at the stage of project construction. The amount of VGF will be equivalent to the lowest bid for capital subsidy, but subject to a maximum of 20% of the total project cost. In case the sponsoring Ministry/State Government/ statutory entity propose to provide any assistance over and above the said VGF, it will be restricted to a further 20% of the total project cost.

Support under this scheme is available only for infrastructure projects where private sector sponsors are selected through a process of competitive bidding. The project agreements must also adhere to best practices that would secure value for public money and safeguard user interests. The lead financial institution for the project is responsible for regular monitoring and periodic evaluation of project compliance with agreed milestones and performance levels, particularly for the purpose of grant disbursement. VGF is disbursed only after the private sector company has subscribed and expended the equity contribution required for the project.

India Infrastructure Finance Company Limited.

IIFCL was set up in 2006 to provide long term debt for infrastructure projects. Infrastructure projects are typically long gestation projects and require debt of longer maturity. The provision of long term funds from commercial banks is restricted due to their asset-liability mismatch. IIFCL tries to address the above constraints in long term debt financing of infrastructure.

IIFCL provides financial assistance to commercially viable projects, which includes projects implemented by a public sector company; a private sector company; or a private sector company selected under a Public Private Partnership (PPP) initiative. Priority is given to those PPP projects awarded to private companies, which are selected through competitive bidding process.

Only projects pertaining to following sectors are eligible for financing from IIFCL:

- Road and bridges, railways, seaports, airports, inland waterways and other transportation projects;

- Power;

- Urban transport, water supply, sewage, solid waste management and other physical infrastructure in urban areas;

- Gas pipelines;

- Infrastructure projects in Special Economic Zones;

- International convention centres and other tourism infrastructure projects;

- Cold storage chains;

- Warehouses;

- Fertilizer Manufacturing Industry

IIFCL raises funds from domestic as well as external markets on the strength of government guarantees. The mode of lending is either long term debt; refinance to banks and financial institutions for loans granted by them to infrastructure companies; takes out finance; subordinate debt and any other mode approved by Government from time to time. The total lending by IIFCL is limited to 20% of the Total Project Cost.

In 2008, a wholly owned subsidiary of IIFCL, IIFCL (UK) Ltd, was established in London with the objective of utilising the foreign exchange reserves of RBI to fund off-shore capital expenditure of Indian companies implementing infrastructure projects in India.

Infrastructure Debt Funds.

The term Debt Fund is generally understood as an investment pool which invests in debt securities of companies. However, an Infrastructure Debt Fund(IDF) registered in India refers to a company or a Trust constituted for the purpose of investing in the debt securities of infrastructure companies or Public Private Partnership Projects. Thus, in contrast to the general understanding of the term, IDF does not refer to a Scheme floated by a mutual fund or such other organizations but to the Company or Trust who is investing in debt securities. An IDF can float various Schemes for financing infrastructure projects.

PurposeIDF is a distinctive attempt to address the issue of sourcing long term debt for infrastructure projects in India. Union Finance Minister in his Budget Speech of 2011-12 had announced setting up of IDFs to accelerate and enhance the flow of long term debt in infrastructure projects. IDFs are meant to

- supplement lending for infrastructure projects

- provide a vehicle for refinancing the existing debt of infrastructure projects presently funded mostly by commercial banks

Structure& Regulation

These Funds can be established by Banks, Financial Institutions and Non- Banking Financial Companies (NBFCs).

IDFs can be set up either as a company or as a trust. A trust based IDF would normally be a Mutual Fund (MF) that would issue units while a company based IDF would normally be a form of NBFC that would issue bonds. Further, a trust based IDF (MF) would be regulated by SEBI; and an IDF set up as a company (NBFC) would be regulated by RBI.

IDF –MF can be sponsored (sponsor is akin to a promoter) by any NBFC which includes an Infrastructure Finance Company(IFC). However, IDF-NBFC can be sponsored only by an IFC.

Investors

The investors in IDFs would primarily be domestic and off-shore institutional investors, especially Insurance and Pension Funds who have long term resources. Banks and Financial Institutions would only be allowed to invest as sponsors / promoters of an IDF subject to certain conditions. The foreign investors eligible to invest in IDFs include FIIs/Sub-accounts, NRIs, HNIs, QFIs and long term foreign investors such as Sovereign Wealth Funds, Multilateral Agencies, Pension Funds, Insurance Funds and Endowment Funds. To attract funds, an exemption from income tax for IDF has been provided and also the withholding tax has been reduced to 5% from 20% on the interest payment on the borrowings of IDFs.

An IDF-MF would raise resources through issue of rupee denominated units of minimum 5-year maturity, which would be listed in a recognized stock exchange and tradable among investors. It would have to invest minimum 90% of its assets in the debt securities of infrastructure companies or SPVs across all infrastructure sectors, project stages and project types. The returns on assets of the IDF will pass through to the investors directly, less the management fee. The credit risks associated with the underlying projects will be borne by the investors and not by the IDF. This structure is focused on investors who can afford to take risk. An existing mutual fund can also launch an IDF Scheme.

An IDF-NBFC would raise resources through issue of either rupee or dollar denominated bonds of minimum 5-year maturity, which would be tradable among investors. It would invest in debt securities of only Public Private Partnership projects which have a buyout guarantee and have completed at least one year of commercial operation.

Buyout guarantee implies compulsory buyout by the Project Authority (which refers to the government agency who is awarding the contract or who is entering into a concession agreement with the private party) in the event of termination of concession agreement.

Refinance (essentially means replacing an older loan issued by a financial institution with a new loan offering better terms) by IDF would be up to 85% of the total debt covered by the concession agreement. Senior lenders would retain the remaining 15% for which they could charge a premium from the infrastructure company. Here, the credit risks associated with the underlying projects will be borne by the IDF. This structure is focused on investors who are risk-averse.

ByHimanshu AroraDoctoral Scholar in Economics & Senior Research Fellow, CDS, Jawaharlal Nehru University