Why in the News?

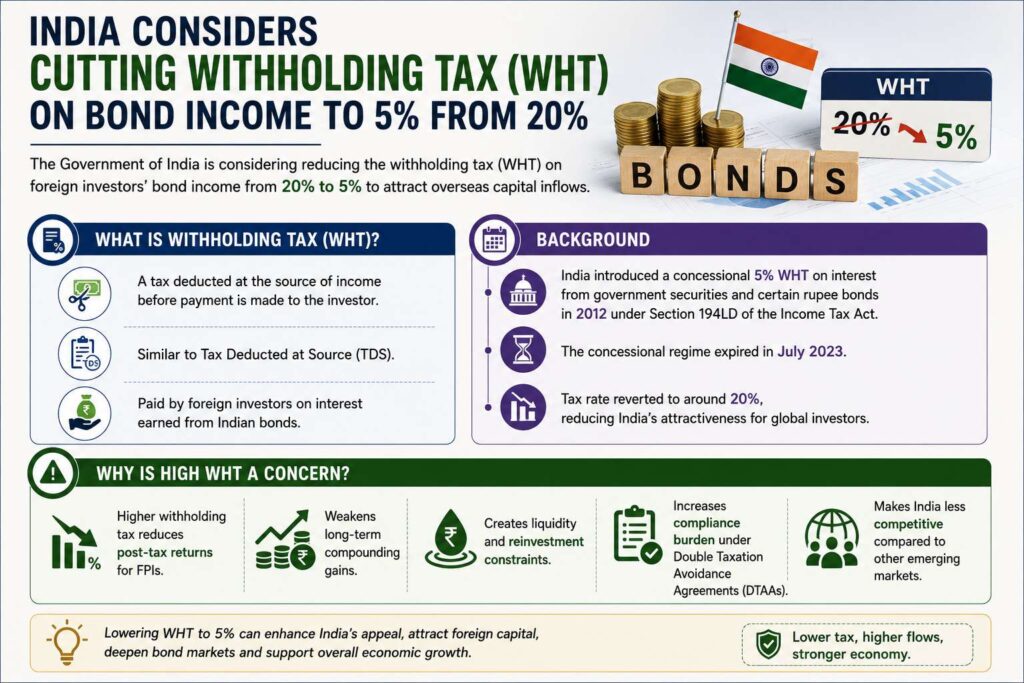

India is reportedly considering reducing the withholding tax on foreign portfolio investors (FPIs) investing in bonds from nearly 20% to the earlier concessional 5% rate. The move comes amid external vulnerabilities, especially rising crude oil prices, pressure on the current account deficit (CAD), and global uncertainty.

How do bonds function as a financial instrument?

- Bond: A bond is a fixed-income financial instrument through which governments or companies borrow money from investors for a fixed period at a predetermined interest rate.

- Issuer-Investor Relationship: The bond issuer receives capital upfront, while the investor receives periodic interest payments (coupon) and repayment of principal at maturity.

- Government Securities (G-Secs): Bonds issued by the government to finance fiscal expenditure and public borrowing requirements.

- Corporate Bonds: Bonds issued by companies to raise funds for business expansion, infrastructure, or debt refinancing.

- Fixed Returns: Bonds generally provide relatively predictable returns compared to equities because they carry fixed interest obligations.

What is meant by bond investment?

- Debt Investment: Bond investment refers to investing money in debt instruments in return for regular interest income and capital repayment at maturity.

- Interest Income: Investors earn periodic returns through coupon payments.

- Capital Appreciation: Bond prices may rise if interest rates decline, allowing investors to sell at higher prices.

- Portfolio Diversification: Institutional investors use bonds to reduce volatility and balance high-risk equity exposure.

- Sovereign Debt Market: In India, foreign investors primarily invest in government securities and rupee-denominated bonds.

How do external sector pressures increase the need for foreign capital inflows?

- Current Account Vulnerability: Rising crude oil prices increase India’s import bill and widen the current account deficit, creating pressure on the external account.

- Forex Reserve Stability: Higher FPI inflows into debt markets strengthen foreign exchange reserves and improve India’s ability to manage external shocks.

- Capital Flow Requirement: Foreign debt inflows provide non-inflationary financing and reduce pressure on domestic borrowing requirements.

- Global Uncertainty: Volatile global financial conditions require India to maintain attractive investment conditions to sustain capital inflows.

How does high withholding tax reduce India’s attractiveness for global bond investors?

- Tax Burden: Withholding tax directly reduces post-tax returns because it is deducted at source before income reaches foreign investors.

- Withholding Tax (WHT): Tax deducted at source on payments such as interest, dividends, royalties, and fees before remittance to recipients. Its purpose is to ensure upfront tax collection and reduce evasion.

- Relative Disadvantage: India’s withholding tax reverted to nearly 20% after July 2023, making India a relatively high-tax jurisdiction for global bond investors.

- Transaction Costs: Higher taxes reduce risk-adjusted returns and increase the effective cost of investing in Indian debt markets.

- Regulatory Frictions: Complex tax claims under Double Taxation Avoidance Agreements (DTAAs) increase compliance costs for FPIs.

- Liquidity Constraints: Tax deductions lock investor capital temporarily until refunds or tax credits are processed.

What was India’s earlier concessional withholding tax regime?

- Policy Shift in 2012: India introduced a concessional 5% withholding tax in 2012 on interest earned by foreign investors from government securities and specified rupee-denominated bonds under Section 194LD of the Income Tax Act.

- Investment Incentive: The concessional regime ensured better post-tax returns and improved India’s attractiveness to global investors.

- Expiry of Regime: The concessional tax structure expired in July 2023, after which taxation reverted to approximately 20%.

- Policy Reconsideration: The government is now evaluating a restoration of lower rates to revive overseas debt inflows.

How do international tax structures shape global capital allocation?

- Comparative Taxation: Global investors allocate capital by comparing post-tax yields across jurisdictions.

- United States: Imposes approximately 30% withholding tax on foreign investors.

- Germany: Imposes nearly 26.4% withholding tax.

- France: Applies nearly 25% withholding tax.

- China: Maintains roughly 10% withholding tax.

- Hong Kong and Singapore: Do not impose withholding tax on foreign bond investors, increasing market competitiveness.

- Tax Competitiveness: Jurisdictions with lower tax burdens attract larger foreign debt participation.

How important are FPIs for India’s bond market?

The RBI defines FPI as any investment made by a non-resident entity in transferable financial assets (such as equity shares, corporate bonds, government securities, or mutual funds) without seeking operational or management control over the underlying company. An FPI can hold a maximum of less than 10% of the total paid-up equity capital of a single listed Indian company.

- Debt Market Participation: FPIs hold a relatively small share of India’s government debt market but their exposure is increasing.

- Global Bond Index Inclusion: India’s inclusion in the JPMorgan Government Bond Index-Emerging Markets (GBI-EM) has increased investor interest in Indian sovereign debt.

- Investment Cap: The Reserve Bank of India (RBI) permits FPI investment up to 6% of outstanding government securities stock.

- Sharp Rise in Investments: FPI investment in dated government securities increased from $30.6 billion (March 2024) to $43.2 billion (March 2025).

What are the possible macroeconomic gains from lowering withholding tax?

- Higher Capital Inflows: Improves overseas participation in Indian debt markets.

- Exchange Rate Stability: Supports rupee stability by improving foreign exchange availability.

- Borrowing Cost Efficiency: Larger investor participation can lower sovereign borrowing costs.

- Bond Market Deepening: Strengthens liquidity and improves depth of India’s debt market.

- Global Financial Integration: Facilitates smoother integration with international capital markets after bond index inclusion.

What concerns may arise from excessive dependence on FPI debt flows?

- Capital Flight Risk: Portfolio investments remain sensitive to global interest rates and geopolitical uncertainty.

- External Vulnerability: Sudden reversals can weaken the rupee and intensify external sector stress.

- Tax Revenue Trade-off: Lower withholding tax may reduce short-term tax collections.

- Market Volatility: Excessive foreign participation may amplify bond yield fluctuations.

Conclusion

Reducing withholding tax on bond investments can strengthen India’s attractiveness as a debt investment destination at a time of external uncertainty and rising financing requirements. However, durable gains require balancing tax competitiveness with macroeconomic stability, prudent capital flow management, and deeper domestic bond market reforms.

PYQ Relevance

[UPSC 2018] How would the recent phenomena of protectionism and currency manipulations in world trade affect macroeconomic stability of India?

Linkage: The PYQ tests understanding of external sector stability, capital flows, exchange rate management, and macroeconomic resilience in a globalised economy. Higher bond inflows can improve forex reserves, rupee stability, and financing of the current account deficit, directly affecting macroeconomic stability.

Context

Context  Types of Inflation

Types of Inflation