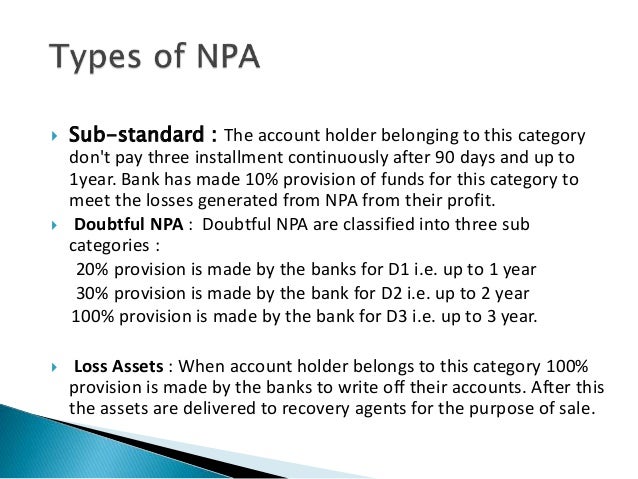

- What is NPA?

- Impact of NPA on economy

- Reasons for the rise in NPA in recent years

- Why most NPA in Public sector?

- Steps taken by RBI and Government in last few years to curb NPA

- How to curb the menace of NPA

source

According to RBI’s recent data, the gross non-performing assets (NPAs) of public sector banks are just under Rs 4 lakh crore, and they collectively account for 90 percent of such rotten apples in the country’s banking portfolio.

In terms of net NPAs, their share is even higher – at 92 percent of the total bad loans reported so far in the banking system. The total NPAs of Indian banks, as a percentage of the total loans, has grown from 2.11 per cent(2008) to 5.08 percent(2016).

In this article we will explain what is NPA, The reason why NPA increased in India and steps taken by Government in recent years to curb the menace of NPA and what else needs to be done.

What is NPA?

- The assets of the banks which don’t perform (that is – don’t bring any return) are called Non Performing Assets (NPA) or bad loans. Bank’s assets are the loans and advances given to customers. If customers don’t pay either interest or part of principal or both, the loan turns into bad loan.

- According to RBI, terms loans on which interest or instalment of principal remain overdue for a period of more than 90 days from the end of a particular quarter is called a Non-performing Asset.

- However, in terms of Agriculture / Farm Loans; the NPA is defined as under: For short duration crop agriculture loans such as paddy, Jowar, Bajra etc. if the loan (installment / interest) is not paid for 2 crop seasons, it would be termed as a NPA. For Long Duration Crops, the above would be 1 Crop season from the due date.

source

Impact of NPA on Economy

The problem of NPAs in the Indian banking system is one of the foremost and the most formidable problems that had impact the entire banking system. Higher NPA leads to following adverse impact on Economy:

- Depositors do not get rightful returns and many times may lose uninsured deposits. Banks may begin charging higher interest rates on some products to compensate Non-performing loan losses

- Bank shareholders are adversely affected

- Bad loans imply redirecting of funds from good projects to bad ones. Hence, the economy suffers due to loss of good projects and failure of bad investments

- When bank do not get loan repayment or interest payments, liquidity problems may ensue.

Reasons for the rise in NPA in recent years

- GDP slowdown: Between early 2000’s and 2008 Indian economy were in the boom phase. During this period Banks especially Public sector banks lent extensively to corporates. However, the profits of most of the corporate dwindled due to slowdown in the global and domestic economy, bans in mining projects, delays in environmental related permits ,Land acquisition hurdles and volatility in prices of raw material. This has adversely affected their ability to pay back loans and is the most important reason behind increase in NPA of public sector banks.

- Relaxed lending Norms: One of the main reasons of rising NPA was the relaxed lending norms especially for corporate honchos when their financial status and credit rating was not analyzed properly. Also, to face competition banks were hugely selling unsecured loans .

- Priority Sector Lending: There is a myth that main reason for rise in NPA in Public sector banks was Priority sector lending as according to the findings of Standing Committee on Finance , NPAs in the corporate sector are far higher than those in the priority or agriculture sector. However, even if PSL is not the main cause but it is still a cause for rising NPA which can be seen from the fact that As per the latest estimates by the SBI, education loans constitute 20% of its NPAs.

- The Lack of Bankruptcy code in India and sluggish legal system makes it difficult for banks to recover these loans from both corporate and noncorporate.

Other factors

- Banks did not conducted adequate contingency planning, especially for mitigating project risk. They did not factor eventualities like failure of gas projects to ensure supply of gas or failure of land acquisition process for highways.

- Restructuring of loan facility was extended to companies that were facing larger problems of over-leverage & inadequate profitability. This problem was more in the Public sector banks.

- Companies with dwindling debt repayment capacity were raising more & more debt from the system.

Why most NPA in Public sector?

- Five sectors Textile, aviation, mining, Infrastructure contributes to most of the NPA, since most of the loan given in these sector are by PSB, they account for most of the NPA.

- Public Sector banks provide around 80% of the credit to industries and it is this part of the credit distribution that forms a great chunk of NPA. Last year, when kingfisher was marred in financial crisis, SBI provided it huge amount of loan which it is not able to recover from it.

- Less Professional management

- Political Pressure and interference forces PSB to lend to not so commercially sounds project.

Steps taken by RBI and Government in last few years to curb NPA

- Government has launched Mission Indradhanush to make the working of public sector bank more transparent and professional in order to curb the menace of NPA in future.

- Government has also proposed to introduce Bankruptcy code which will make it easier for banks to Recover the loans from the debtors.

- RBI introduced number of measures in last few years which include:

- Tightening the Corporate Debt Restructuring (CDR) mechanism,

- Setting up a Joint Lenders’ Forum, prodding banks to disclose the real picture of bad loans, asking them to increase provisioning for stressed assets,

- Introducing a 5:25 scheme where loans are to be amortized over 25 years with refinancing option after every five years, and

- Empowering them to take majority control in defaulting companies under the Strategic Debt Restructuring (SDR) scheme.

How to curb the menace of NPA?

#1. Short Term measures

- Review of NPA’S/Restructured advances- We need to assess the viability case by case. Viable accounts need to be given more finance for turnaround and unviable accounts should either be given to Asset Reconstruction Company or Management/ownership restructuring or permitting banks to take over the units.

- Bankruptcy code should be passed as soon as possible. Bankruptcy code will make it easier for banks to recover loans from unviable enterprises.

- Government should establish ARC with equity contribution from the government and the Reserve Bank of India (RBI). The established ARC should take the tumor (of non-performing assets or NPAs) out” of the banking system. An ARC acquires bad loans from banks and financial institutions, usually at a discount, and works to recover them through a variety of measures, including sale of assets or a turnaround steered by professional management. Relieved of their NPA burden, the banks can focus on their core activity of lending.

#2. Long term Measures

- Improving credit risk management– This includes credit appraisal, credit monitoring, and efficient system of fixing accountability and analyzing trends in group leverage to which the borrowing firm belongs to

- Sources/structure of equity capital– Banks need to see that promoter’s contribution is funded through equity and not debt.

- Banks should conduct necessary sensitivity analysis and contingency planning while appraising the projects and it should built adequate safeguards against such external factors.

- Strengthen credit monitoring– Develop an early warning mechanism and comprehensive MIS(Management information system) can play an important role in it.MIS must enable timely detection of problem accounts, flag early signs of delinquencies and facilitate timely information to management on these aspects.

- Enforce accountability- Till now lower ring officials considered accountable even though loaning decisions are taken at higher level. Thus sanction official should also share the burden of responsibility.

- Restructured accounts should treated as non performing and technical write offs where Banks remove NPA’S from their balance sheets Permanently should be dispensed with.

- Address corporate governance issues in PSB- This includes explicit fit and proper criteria for appointment of top executives and instituting system of an open market wide search for Chairman.

References:

Comments

One response to “NPA Crisis”

Very helpfull