💥Join UPSC 2027,2028 Mentorship (July Batch) + XFactor Notes & Microthemes PDF

Talk to Mentor

Skip to content

Civilsdaily

My Courses

About UPSC

UPSC IAS Civil Services Syllabus

New to IAS Preparation? How to start ?

Recommended Books for UPSC Exam (Prelims & Mains)

Must Read (OLD & NEW) NCERTs for IAS Preparation

CivilsDaily’s UPSC material and notes: FREE UPSC Materials for you

UPSC Post list and Salary

IAS officer salary after 7th Pay Commission | IAS Promotion Chart | Vs. IPS, IFS

Study Plans

Study Guide : How to prepare Polity for IAS Prelims

Comprehensive Self Study Plan for Indian History | IAS Prelims & Mains

Comprehensive Self Study Plan for Economics| IAS Prelims & Mains

Comprehensive Self-Study Plan for Physical Geography | IAS Prelims & Mains

Prelims

[FREE]Prelims Daily

Daily Current Affairs Questions for IAS Prelims.

[FREE]Nikaalo Prelims

UPSC IAS Prelims Trend Analysis Year-wise and subject-wise

Attempt Year-wise previous year papers

Mains

Ranker Mains Guidance Program 2024

UPSC Mains Solutions, Sample Answers, Civilsdaily TS Hit Ratio

[FREE]Daily AWE

Our Daily Answer Writing Enhancement (AWE) focuses on the daily answer writing needs of UPSC candidates.

Current Affairs

Paper 1

Paper 2

Paper 3

Paper 4

Economics Stories

Polity Stories

Governance Stories

Important aspects of Governance

Enviro & Biodiversity Economics Stories

International Relations Stories

Science Tech Art Culture

Login

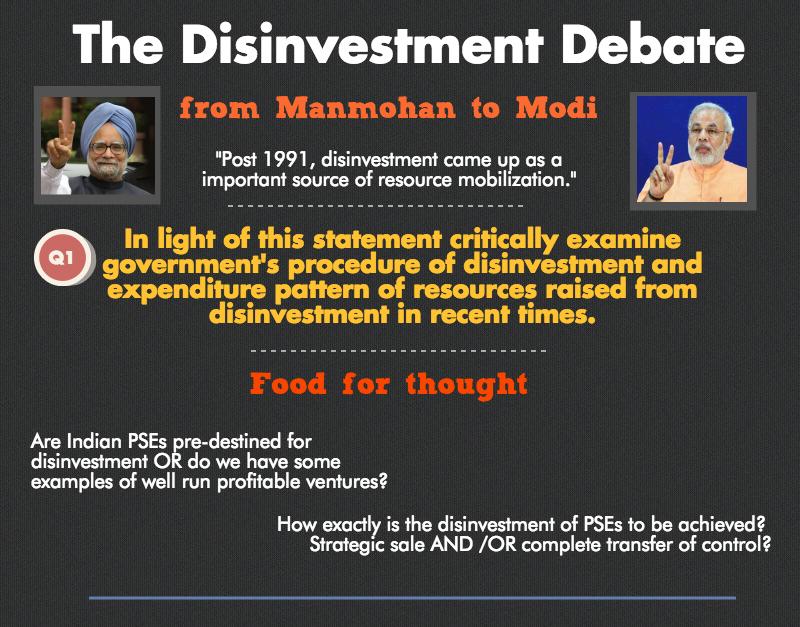

Disinvestment in India

Written by

Rohit Pande

in

←

Goods and Services Tax (GST)

Minimum Support Prices for Agricultural Produce

→

Comments

19 responses to “Disinvestment in India”

Comments

19 responses to “Disinvestment in India”